Hi Carl,

Persistent discounts to NAV in ASX LITs can drive corporate action, including wind-ups or delistings, but typically it requires a catalyst. The key trigger is sustained underperformance alongside a wide discount (e.g. >10–15%) over time, which frustrates shareholders. This is often followed by activist or large holder pressure to realise value. Other contributing factors include high fees, declining FUM, or strategy changes that fail to close the discount.

In practice, outcomes are usually determined via shareholder votes (e.g. continuation votes) or board-led strategic reviews. If investors conclude the listed structure is destroying value, they may support a wind-up and return capital at or near NAV. While some LITs attempt interim measures such as buybacks, tender offers or fee reductions, failure to narrow the discount increases the likelihood of a full exit.

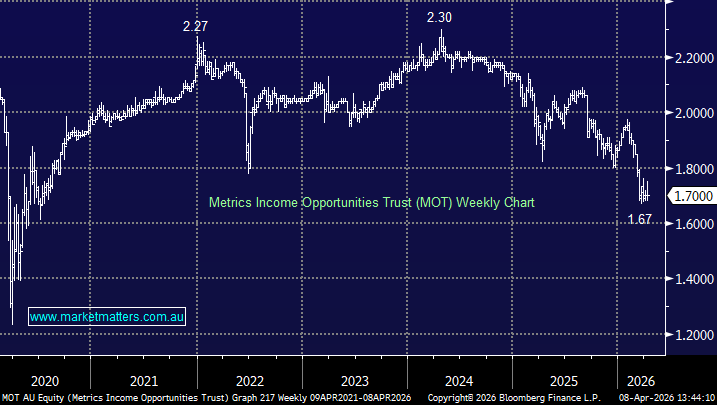

We mentioned the MCP Income Opportunities Trust (ASX:MOT), which is trading over 20% below NTA, in April. But this LIT benefits from reasonable scale and manager backing, which reduces the probability of near-term action relative to smaller, less supported peers.