Hi Simon,

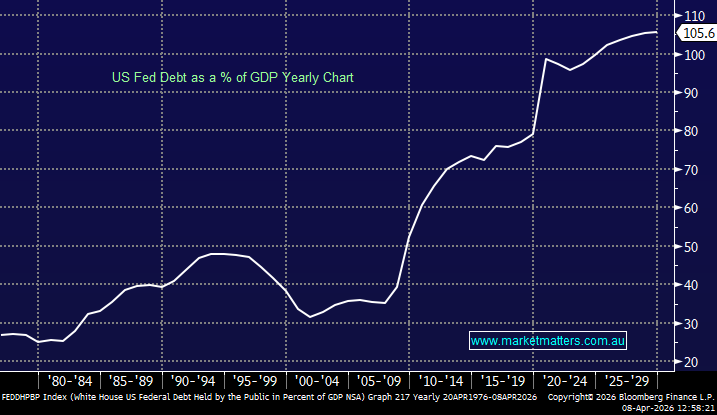

In our view, US debt is a long-term structural issue rather than an imminent crisis, and it is important to separate “war-driven” spending from the broader fiscal trajectory. While defence outlays contribute at the margin, the key drivers of US debt are persistent primary deficits, entitlement spending and rising interest costs. The most relevant measure to assess sustainability is debt held by the public as a % of GDP (currently ~100%), rather than gross debt (~$39T), which includes intra-government holdings. Also, markets are increasingly focus on interest-to-revenue ratios, as these capture the real fiscal burden.

- We believe the $US is “wobbling” as the worlds reserve currency contributing to the strong rise in gold in recent times.

The reason the US has been able to sustain elevated debt levels, as you touched on, is a combination of strong nominal GDP growth, reserve currency status and deep capital markets. As long as growth (nominal GDP) is comparable to or exceeds the effective interest rate on debt, the system remains manageable. However, the inflection point occurs when interest costs compound faster than growth, forcing higher borrowing just to service existing obligations. At that stage, fiscal flexibility deteriorates and investor confidence becomes more sensitive to policy credibility rather than absolute debt levels.

- For decades markets have largely ignored rising US debt, and though the chicken is likely to come home to roost one day, that may not be for several years, i.e. we wouldn’t worry about it yet, it’s unlikely to be a “Black Swan” event, more of slow-moving juggernaut that finally scares markets.