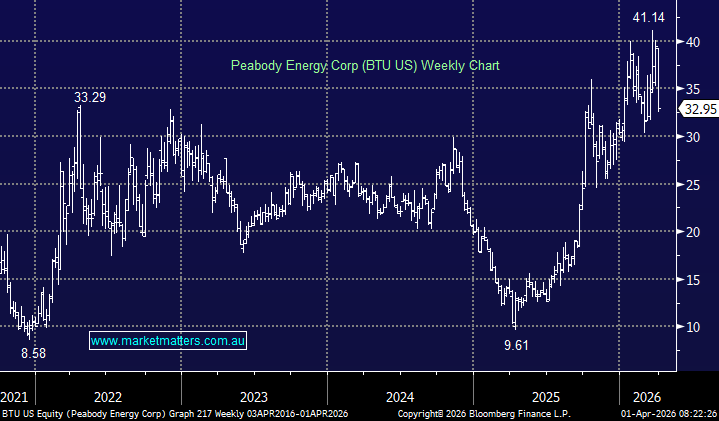

BTU was hit hard over the past two session, falling around 15% after warning that Q1 sales volumes from its Centurion mine in QLD will be materially below prior expectations. The company now expects roughly 250kt of shipments versus earlier guidance of around 700kt, blaming more difficult-than-expected commissioning challenges.

Importantly, management left FY26 metallurgical coal volume guidance unchanged at 10.3–11.3Mt, suggesting this a timing and ramp-up issue rather than a structural problem. That said, the market is clearly worried that Centurion, a key plank of the medium-term growth story, may take longer to deliver than hoped.

Analysts were mixed in their assessments, but not outright negative. Jefferies kept a Buy rating, arguing that stronger seaborne thermal coal prices should help offset some of the near-term earnings impact, although they conceded the stock is likely to remain under a cloud until Centurion is ramping smoothly. BMO estimated the disruption could trim Q1 EBITDA by US$25–30m and suggested the top end of full-year guidance may now be harder to achieve.

- Overall, this was a disappointing update, no doubt, and without the recent Coal price tailwind, the stock would have fared worse. We trimmed BTU last week, bringing it back to a 4% holding – we should have done more!

MM has turned more neutral on BTU ~$US33

Add To Hit List