We own Regal Partners (RPL) in the Emerging Companies Portfolio and remain bullish on the business. However, Regal’s recent experience in biotech highlights the risks of investing in the sector.

Regal was a major backer of Opthea, holding a stake worth ~$220m before things unravelled. In April, Opthea effectively collapsed after late-stage trials for its lead drug OPT-302 failed, with the company warning it may become insolvent – years of funding and development wiped out overnight on a single data point. Last week, a similar dynamic played out with Immutep (IMM).

The company’s lead therapy Efti, targeting lung cancer, failed a key futility analysis despite encouraging prior data. The stock fell ~90% as a result. Regal owned ~14% of the company, worth around $80m pre the news. To be clear, Immutep still has other programs underway and funding in place into next year, but both experiences show that when the primary asset disappoints, it destroys significant value overnight, and it’s the main reason why MM typically avoids the sector.

Other major/well owned Biotech’s have also experienced a tough period of late:

- Telix Pharmaceuticals (TLX) is down ~60% over the past year

- Neuren Pharmaceuticals (NEU) down ~45% from its October highs

Both are high-quality businesses with strong backing, but even here, regulatory delays, trial uncertainty and sentiment shifts have driven significant volatility.

For Regal, this is part of their approach. They are an aggressive manager, targeting high returns (& charging high fees), investing across a range of strategies, including higher-risk, high-reward opportunities like biotech. While both Opthea and now Immutep are clearly a negative outcome, it sits within a diversified alternatives platform and importantly does not change our broader thesis on the stock.

Regal started out as a high-conviction, equities-focused manager, heavily influenced by Phil King’s stock-picking ability, but they’ve evolved into a broader alternatives platform, more akin (on a lot smaller scale) to a Blackstone-style model. Regal has deliberately shifted its model.

Through a combination of organic growth and acquisitions, the business now spans multiple strategies:

- Long/short equities (still core, but no longer dominant)

- Private markets & venture (including biotech exposure like Immutep)

- Real assets & natural resources

- Credit & income strategies

- Special situations / event-driven investing

Just as importantly, Regal has moved from a single lead PM model to a collection of specialist investment teams.

This evolution improves the investment case. The business is no longer reliant on one individual or one strategy to drive returns. Different strategies perform at different times, smoothing revenue across cycles. Alternatives (private markets, credit, real assets) are where flows are heading globally and like global peers, Regal earns fees across a range of strategies, creating scalability as FUM grows.

Regal are attempting to build a mini Blackstone, and we believe the strategy has a lot of merit.

- Build a multi-strategy alternatives platform

- House multiple specialist managers under one umbrella

- Generate a mix of management + performance fees across asset classes

- Reduce reliance on any single market or style

This is a structurally more resilient model than a pure equities hedge fund. The business is now broader, more scalable and less cyclical. Earnings are less reliant on one person or one strategy, and they are successfully building out more exposure to higher-growth areas in alternatives, providing longer-term upside in MM’s view. But it also introduces more moving parts. Private Credit has become a hot topic globally, and exposure here (through the purchase of Merricks in 2024 for ~$235m) significantly expanded private credit exposure – an area that we think will have more ‘issues’ in the coming years relative to the benign environment that has in play for the last 5-10 years – though we still think this is a worthwhile area for investors & the funds operating in this space (just don’t have all your eggs in the private credit basket).

Overall, issues like Opthea and Immutep are disappointing, but they are par for the course when investing at the aggressive end of the spectrum. For MM, we have little interest in taking on the outcomes that are so prevalent across the biotech space, but we do think Regal is growing into a true diversified alternatives manager, at a time when private market investing continues to see good flows.

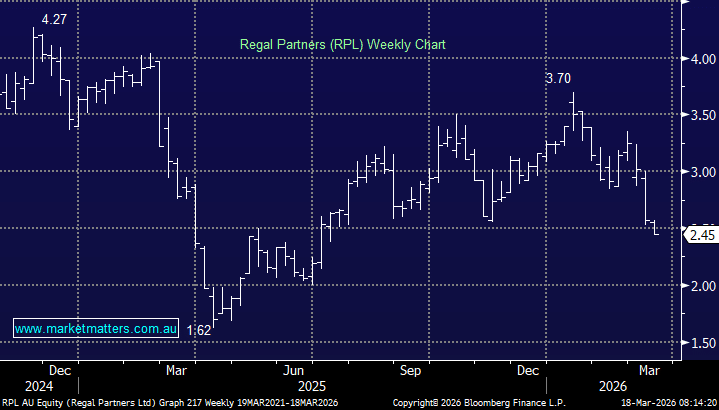

- Recent share price weakness on the back of IMM and Private Credit concerns, we think, is offering up another opportunity in RPL – and we’re likely to increase our weighting as the dust settles.

MM remains long and bullish RPL in the Emerging Companies strategy

Add To Hit List