Hi Darren,

Good timing, we discussed SDR in detail earlier in the week Here.

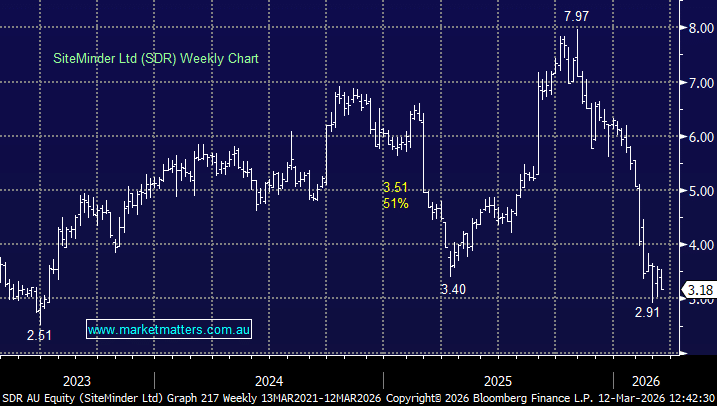

SiteMinder’s share price weakness appears driven more by sentiment toward small-cap SaaS stocks than by deterioration in fundamentals. The stock is trading around $3.51, well below our $5.80 entry point, but after repeatedly stress-testing the thesis we believe the core investment case remains intact.

SiteMinder provides mission-critical cloud software for hotels, connecting properties to major booking platforms like Booking.com, Expedia and Airbnb. The platform allows hotels to manage inventory, pricing and distribution across hundreds of channels from a single interface. This infrastructure is highly sticky and embedded in hotel operations, and the industry is still early in its digital transformation, with many properties globally yet to adopt modern systems.

While the market has been disappointed by slower near-term margin expansion—largely due to continued investment in product development and global expansion—the strategic position of the business hasn’t changed. SiteMinder connects ~50,000 hotels worldwide to hundreds of booking channels, creating network effects that strengthen as the platform scales. More hotels attract more distribution partners, which in turn increases value for hotels, forming a self-reinforcing competitive moat that would be difficult to replicate.

Meanwhile, global travel demand remains resilient, and hotel operators continue investing in technology to optimise pricing and occupancy. SiteMinder sits directly within this spending trend. As the business scales, SaaS operating leverage should emerge, with incremental revenue increasingly flowing to profit.

At current levels, the market appears to be pricing the business as if the investment phase will never end, which we think is overly pessimistic. Given its global footprint, structural growth tailwinds and strong platform economics, we remain comfortable holding SDR and are looking to add to the position.

- We are looking to add to our SDR position, ideally below $3 but we believe value is now presenting itself following the steep sell-off/valuation contraction.