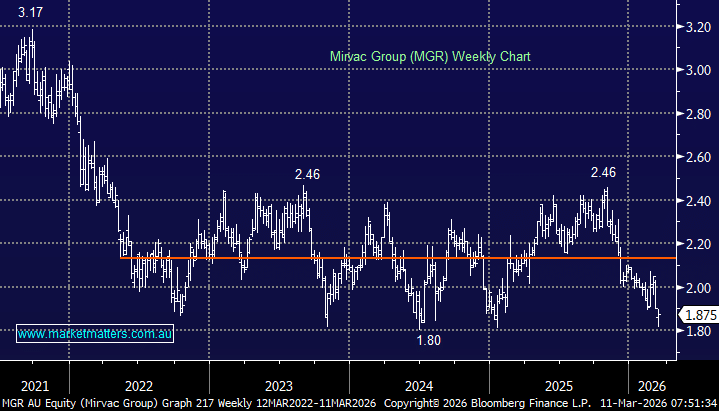

We added Mirvac Group (MGR) to both the Income & Growth portfolios yesterday after recent weakness created what we think is an attractive entry point into one of the higher-quality names in the Australian property sector. The stock has pulled back over the past week or so, not because of any deterioration in the business itself, but largely due to the sharp move higher in bond yields, with the Australian 10-year yield briefly trading above 5%. Rising yields are typically a headwind for listed property, compressing valuation multiples and increasing discount rates applied to long-duration assets.

However, the recent surge in yields looks heavily influenced by the spike in oil prices and renewed inflation concerns stemming from geopolitical tensions in the Middle East. If energy prices stabilise, bond yields could ease again, which would likely provide some support to rate-sensitive sectors such as REITs.

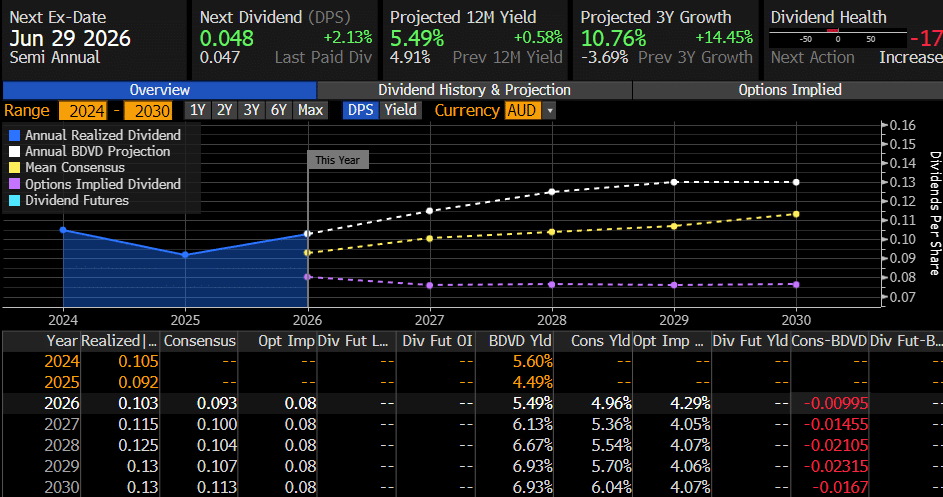

- MGR is expected to yield ~5.5% over the coming 12 months, with the next dividend due in June.

chart

Mirvac (MGR) consensus dividend expectations – source Bloomberg

chart

Mirvac (MGR) consensus dividend expectations – source Bloomberg

Importantly, Mirvac’s underlying business momentum remains strong, highlighted by a solid first-half result that reinforced the group’s earnings outlook.

Operating profit was up 5.1% YoY, earnings per share (EPS) increased 6% and they left FY operating EPS guidance unchanged at 12.8–13.0c, though momentum in residential settlements increased materially (+38%). This was the highlight of the result, with sales improving and development margins recovering. Mirvac also continues to execute well on capital partnering initiatives, recycling capital into new projects while maintaining a strong balance sheet and around $1.1bn in liquidity. That provides good visibility for earnings growth through FY28 and beyond.

From a portfolio perspective, Mirvac also offers a ~5.5% yield, which becomes increasingly attractive as the sector approaches the June ex-dividend period. If bond yields stabilise and investors rotate back toward income-generating assets, property names like MGR should see improved demand.

- Overall, MGR has solid operating momentum, a strong development pipeline and an attractive yield, and we think the risk/reward looks favourable buying the current weakness, particularly ahead of the sector’s key dividend period.

MM is now long & bullish MGR

Add To Hit List