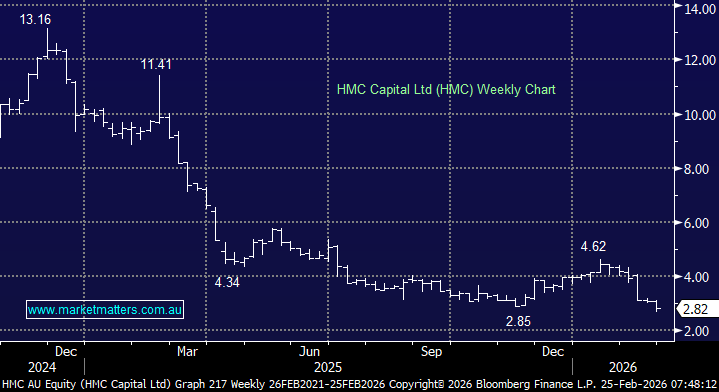

HMC has gone from one of the market’s most celebrated alternative asset managers to one of its most heavily discounted. The share price is down ~70% over the past year (-76% from late-2024 highs), as investors lost faith in the group’s ability to deliver on its ambitious targets; $50bn assets under management (AUM) and 20% return on equity (ROE) targeted within 3-5 years – first announced at its AGM in November 2024. That implied a compound annual growth rate of ~23 % over five years (or ~42 % over three) from then-current levels. (The 20% ROE target had been discussed earlier).

HMC sits today with ~$16bn AUM , which is not insignificant, but it is a long way from the $50bn target by FY30 (5 years from when the target was put out there). Between FY20-24 they enjoyed a compound annual growth rate (CAGR) of ~70%, and were on track to be Australia’s very own, mini-Blackstone.

Since those heady days where Founder, Managing Director and Group CEO David Di-Pilla could do no wrong , AUM growth has slowed to single digits over the past year, with sentiment dented by a major tenant entering receivership (Healthscope), weak performance across satellite exposures (DGT, HDN & HCW) and several false starts in the Energy Transition strategy – a dedicated platform to facilitate investment across the energy value chain, including wind, solar, battery energy storage, bio-fuels and other decarbonisation technologies – chaired by Julia Gillard

Having peaked at $13.16 in November of 2024, the unwind has been brutal, and now HMC trades on 9.4x FY26 consensus earnings, a long way from the 32x it was trading at its peak.

It’s not all bad news; of the 5 core divisions that make up HMC Capital, Real-Estate & Private Credit are continuing to perform steadily, and make up over $12bn of AUM. Private Equity is small ~$500m, while Digital Infrastructure (~$5.5bn) and Energy Transition (~$1.5bn) are struggling to grow. If we price HMC purely on the areas where they have a demonstrable ability to grow AUM at still solid rates, and we slice their $50bn target in half ($25bn by 2030), we can still get a valuation north of $7 at half the multiple that Blackstone currently trades on.

The last time we covered HMC (Oct 2025), we added to our position ~$3.25, reinforcing our 4% target weight. The stock rallied to ~$4.60, but has since rolled over. Results out yesterday sounded positive but did little in the way of supporting the stock.

From here, we need to see positive developments in these key areas:

- HMC Urban Retail Fund (HURF): Targeting ~$1.0–1.5bn, focused on larger regional and sub-regional retail assets. The close has shifted into FY26. A successful raise would directly challenge the market’s “ex-growth” narrative.

- Private Credit momentum: AUM has been grown to $2.2bn (Oct-25) from $1.9bn at June, supported by wholesale and family office inflows into the Core Fund. Continued growth here provides a visible earnings lever.

- Healthscope resolution: Alternative operators have been secured with no change to face rents. A clean outcome during FY26 would remove a persistent overhang on sentiment.

These are all very achievable, and if they can execute, the shares should get rerated higher.

MM is sticking with HMC, seeing deep value sub $3

Add To Hit List