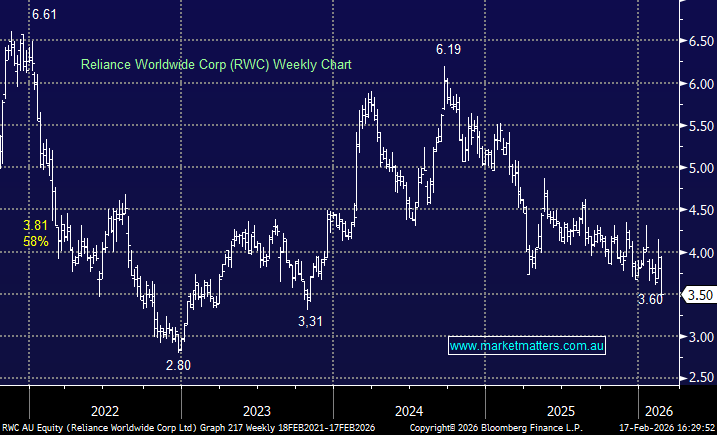

Reliance Worldwide (RWC) -9.09%: delivered a weaker-than-expected first-half result, with softness extending beyond the US into Australia and EMEA, surprising the market. Tariff impacts and lower volumes weighed on margins, and guidance suggests a tougher earnings backdrop through FY26.

- Sales of $645.4mn, -4.6% YoY (vs $677.7mn est.)

- Adjusted net profit $52.2mn, -31% YoY (vs $61.7mn est.)

- Interim dividend 2.0c (vs 2.5c YoY)

- FY26 tariff impact expected $25–30mn

Management expects 2H trading conditions to remain broadly consistent, with mitigation actions reducing tariff impacts and modest margin improvement into the second half, though full-year margins will still be lower than FY25.

This was a disappointing print with multiple regions showing softness, and while cash conversion remains strong, the earnings reset and tariff drag are likely to cap near-term upside.

MM remains neutral toward RWC

Add To Hit List