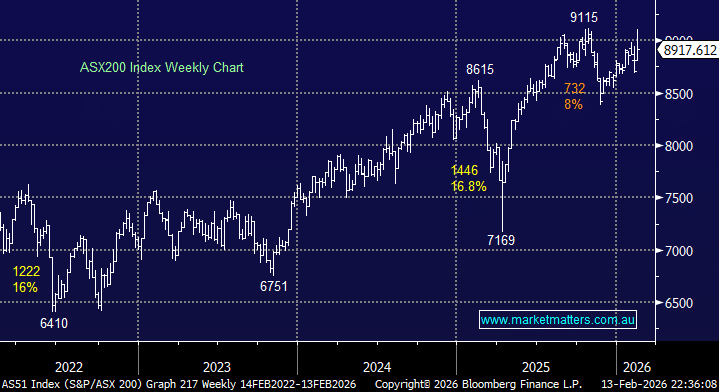

It didn’t feel like it on Friday afternoon as the ASX200 plunged more than 125 points, but the index still managed to finish last week up +2.4% after one of the most violent weeks of reporting season we can remember – 10% swings in either direction were almost pedestrian! The heavyweight banks and resources offset broad market weakness, led by any stocks feared to be at risk of AI disruption, with selling gathering momentum from already panic-like levels. The dominant themes were very binary in nature:

- The disruption by AI across the software sector saw aggressive selling spread from software stocks to the insurance sector, while refocusing on logistics companies.

- The banks surged higher as the “Big Four” delivered strong 1H and quarterly trading updates.

- The resources bounced back into favour as precious metals became less volatile and the heavyweight diversified miners hit new all-time highs.

- Conversely, the retailers and healthcare names came under pressure with “misses” more prevalent across both sectors.

- The defensives were well bid across the “risk off” week, with the utilities particularly strong.

On the stock level, despite the aggressive sell-off by software stocks, the losers enclosure was dominated by companies that disappointed with their earnings updates this week, while the winners were all about the reporting season:

Winners: Ora Banda Mining (OBM) +17%, AGL Energy (AGL) +16%, James Hardie (JHX) +13%, Aussie Broadband (ABB) +12%, Lynas Rare Earths (LYC) +12%, Commonwealth Bank (CBA) +11%, and ANZ Group (ANZ) +10%.

Losers: Temple & Webster (TPW) -32%, Pro Medicus (PME) -25%, Nick Scali (NCK) -22%, Cochlear (COH) -20%, CSL Ltd (CSL) -17%, AMP Ltd (AMP) -15%, Austal (ASB) -15%, SiteMinder (SDR) -15%, Steadfast (SDF) -12.9%, and AUB Group (AUB) -12.3%.

The market-focused news was all about reporting season last week, with little middle ground for those that faced the music:

- The market started the week with an aggressive relief rally, propelling the index up 165 points, led by strong buying across the resources.

- Tuesday saw the “AI disruption” trade switch its attention from tech to insurance, with the brokers in particular following their US peers lower.

- The ASX200 fell a few points short of posting new all-time highs on Wednesday following an impressive result from CBA, which saw it surge the most since the COVID recovery.

- The local index ended the week running scared from AI, not helped by some big earnings misses, taking the index well below its all-time high.

- On Friday night, a relatively tame US inflation print saw the CPI gain by the lowest amount since July, with US 2-year yields falling to their lowest level since 2022.

Overseas markets were mixed on Friday evening after a supportive inflation read saw US Treasuries rally (yields lower). In Europe, the UK FTSE advanced +0.4% while the EURO STOXX 50 retreated by -0.4%. In the US, a choppy session saw the NASDAQ close up +0.2% while the S&P 500 slipped -0.1%.

- The SPI Futures are calling the ASX200 to open up +0.6% with the resources likely to be very supportive, with BHP advancing 60c in US trade.