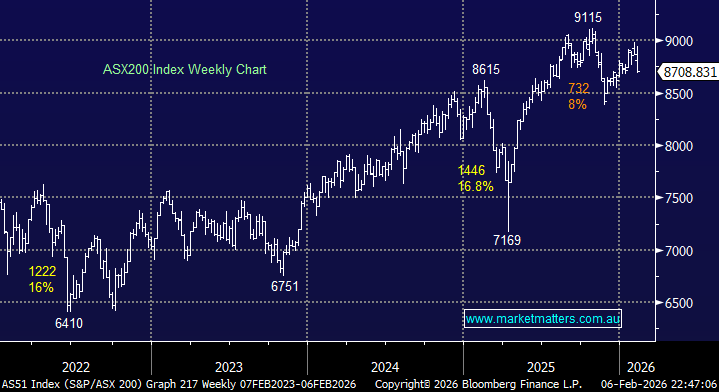

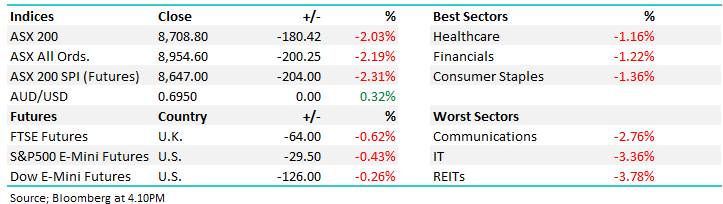

The ASX 200 ended a volatile week down -1.8%, but it felt far worse on Friday when the index tumbled more than 2% – at least it should recover half of those losses on Monday morning. We received a rate hike last week, but it hardly registered with investors, focusing on three major themes:

- The disruption by AI across the software sector, with negative sentiment spreading to tech in general.

- Profit-taking in the commodity markets with silver falling over 16% in just a matter of hours.

- Risk off in general with Bitcoin plunging to its lowest level since late 2024.

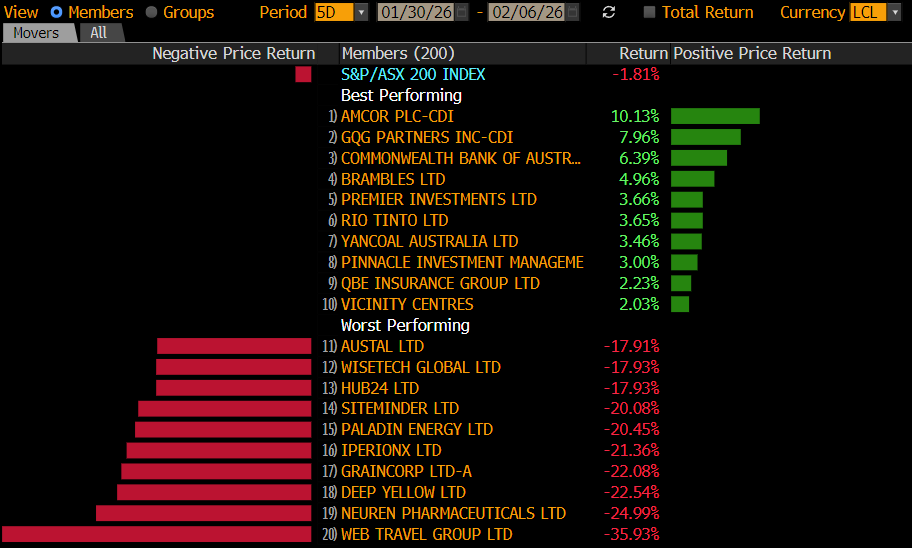

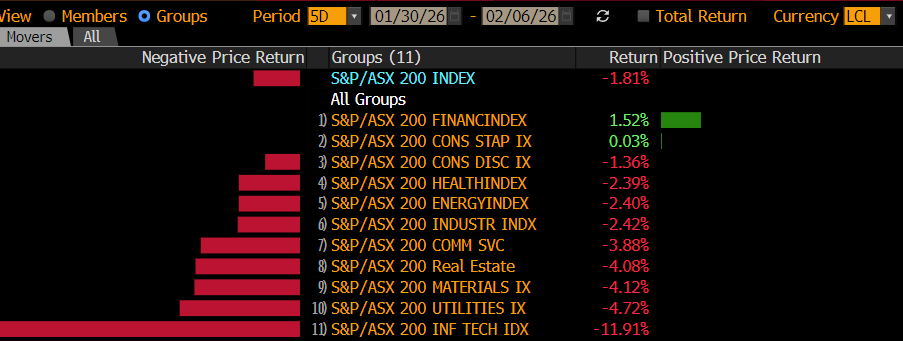

On the stock level, the winners enclosure, while sparse, held a distinctive safety feel, conversely the losers were all about “risk off” surrounding AI disruption. Software stocks were smacked, as were uranium names, on the risks that the forecasted power demand for the AI boom is being overstated.

Winners: Amcor PLC (AMC) +10.1%, GQG Partners (GQG) +8%, Commonwealth Bank (CBA) 6.4%, Brambles (BXB) +5%, RIO Tinto (RIO) +3.7%, Premier Investments (PMV) +3.7%, Pinnacle (PNI) +3%, QBE Insurance (QBE) +2%, and Woolworths (WOW) +1.7%.

Losers: Web Travel (WEB) -35.9%, Deep Yellow (DYL) -22.5%, Paladin (PDN) -20.5%, SiteMinder (SDR) -20%, HUB24 Ltd (HUB) -17.9%, WiseTech Global (WTC) -17.9%, Pro Medicus (PME) -14.4%, Technology One (TNE) -13.2%, and Newmont Corp (NEM) -10.7%.

The news evolved from Trump’s nomination for the Fed Chair to AI in the blink of an eye, with little impact from the RBA’s rate hike:

- The market endured its worst fall of the year on Monday, soon to be eclipsed, down 1% as investors reacted to reports that Donald Trump was going to nominate Kevin Warsh as the next US Federal Reserve chair.

- Precious metals started the week softly, down ¬7%, on the prospect that Warsh wouldn’t be as accommodating with rate cuts as was previously hoped.

- Tuesday saw the first RBA rate-hike since 2023, with the 0.25% tightening to 3.85% having little impact on equities, which managed to close firmly on the day.

- AI-driven disruption gathered momentum on Wednesday with several high-profile ASX names tumbling by over 10%; fortunately for the index, the resources and financials enjoyed a strong session.

- Thursday saw the unprecedented volatility in precious metals, with silver catching the eye as the precious metal plunged over 16% in a matter of hours.

- Friday was primarily back to AI disruption, although the selling was aggressive and broad, and by 4 pm, we all needed a weekend’s rest.

Overseas markets rebounded strongly on Friday, with big tech grabbing the headlines, heavyweight NVIDIA +7.8% and Broadcom +7% both catching the eye. However, the software stocks at the epicentre of disruption fears enjoyed a more muted recovery, e.g., Intuit +2%. In Europe, the EURO STOXX 50 closed +1.2%, leading the UK FTSE, which ended the session up +0.6%.

In the US, the Dow surged +1200 points with the big banks leading the line, while the NASDAQ closed up +2.2% with a 5.6% fall by Amazon weighing on the recovery following its announcement to spend a whopping $US200bn on AI this year – Google also fell 2.5% after announcing similar capex intentions the prior night.

- The SPI Futures are calling the ASX200 to open up +1.2% on Monday morning, with the resources and tech stocks set to open strongly.