Yesterday’s rate rise in Australia has provided an immediate tailwind for floating-rate hybrids, with cash distributions stepping higher as the bank bill swap rate resets. For income-focused investors, that’s the good news. The less comfortable reality is that hybrid margins remain tight by historical standards, meaning total returns are being driven more by higher base rates than by generous risk compensation.

In 2025, APRA confirmed it will phase out bank Additional Tier 1 (AT1) hybrids, replacing them with a mix of Tier 2 subordinated debt and Common Equity Tier 1. The regulator’s stated aim is to simplify bank capital structures in a crisis and reduce reliance on retail investors. We disagreed with the decision – bank hybrids have historically proven resilient through multiple stress periods, delivering income that more than compensated investors for the incremental risk versus term deposits; however, the reality is now that bank hybrids will continue to be phased out with the final issue being called in 2032.

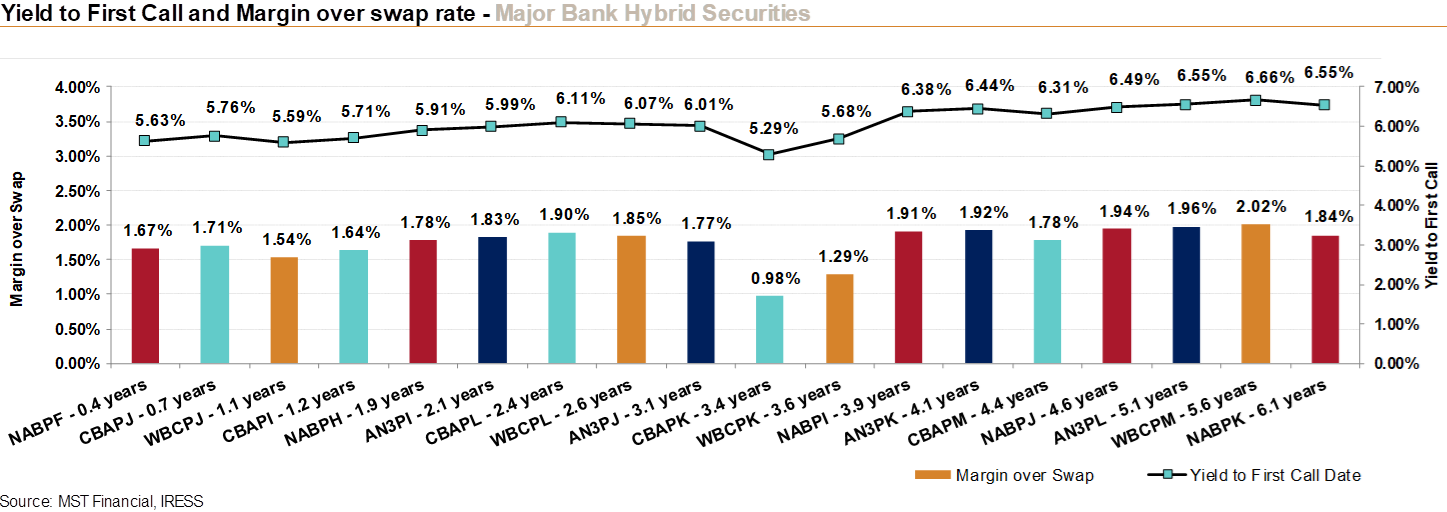

- Bank Hybrids are still trading and can be bought on the market, with major bank hybrids currently offering yields to first call broadly in the 5.6–6.6% range, with margins over swap mostly clustered around ~1.5–2.0%

While these margins are modest relative to long-term averages, they have ticked more attractive versus late-2025 levels as swap rates have risen and prices have stabilised. In short, investors are being paid an adequate return for holding hybrids, and we still believe there is reasonable value in the space – hence several positions still held in the Market Matters Income Portfolio.

The ruling affects roughly $36bn of bank hybrids issued by ANZ, CBA, NAB, Westpac, Macquarie Bank, Bendigo & Adelaide Bank, Bank of Queensland and Judo. However, newer Macquarie hybrids issued at the Macquarie Group level (rather than Macquarie Bank) are not impacted, nor are non-bank hybrids (~$8bn outstanding) from AMP, Challenger, IAG, Latitude, Macquarie Group and Suncorp.

Within the Income Portfolio, we previously held CBAPG, which was called in April 2025, and we still have AN3PI ( due for call in 2028) and WBCPK / NABPI (2029). We don’t expect material pricing disruption beyond potentially reduced liquidity over this time frame. Investors should still receive face value plus accrued distributions at first call.

Alternatives are now coming to market, and we have written about several of them in recent months, namely the Dominion Income Trust (DN1) which is held in the portfolio, while we also like the MA Credit Income Trust (MA1), Dominion Income Notes 1 (DMNHA), the Stonepeak Credit Income Securities (SPPHA), in addition to listed income securities such as the Perpetual Credit Income Trust (PCI) and others. There is also a new listing set for later this month (early next) from Kapstream, a large domestic and US fixed-income and private credit manager that we will write about when further details are released.

- As with anything in financial markets, when a void is left, fund managers will fill that void with alternative offers, and while these securities are different to Hybrids, they are suitable for our income strategy and will be used as a replacement for outgoing Hybrid securities.

For investors able to tap the wholesale market, Tier 2 bank bonds are also attractive, with Westpac coming to market today issuing a new 10 year, with a final legal maturity of 15 years (these are generally called at their first call date), likely to pay a fixed yield above 6%. We also see value in these types of securities, though they are not traded on the ASX.