The ASX 200 ended the short week up just +0.2%, but the volatility over the 4-days was more than many months! The energy and materials sectors were again the top performers, but Friday’s savage 100-point reversal dented many of the previous high flyers, while the rate-sensitive consumer discretionary and tech sectors fought over the wooden spoon, again.

This week is likely to be a very different market following the confirmed nomination of Kevin Warsh to be the next Federal Reserve Chair, taking over from Jerome Powell. Warsh is seen as more inclined than other finalists to guard against rising price pressures, a stance that would translate into monetary policy that is supportive of the US dollar. That saw the $US push up nearly 1% sending Gold & other commodities sharply lower. Gold experienced a top-to-bottom $US900/oz plunge overnight which will have the miners on the back foot on Monday,

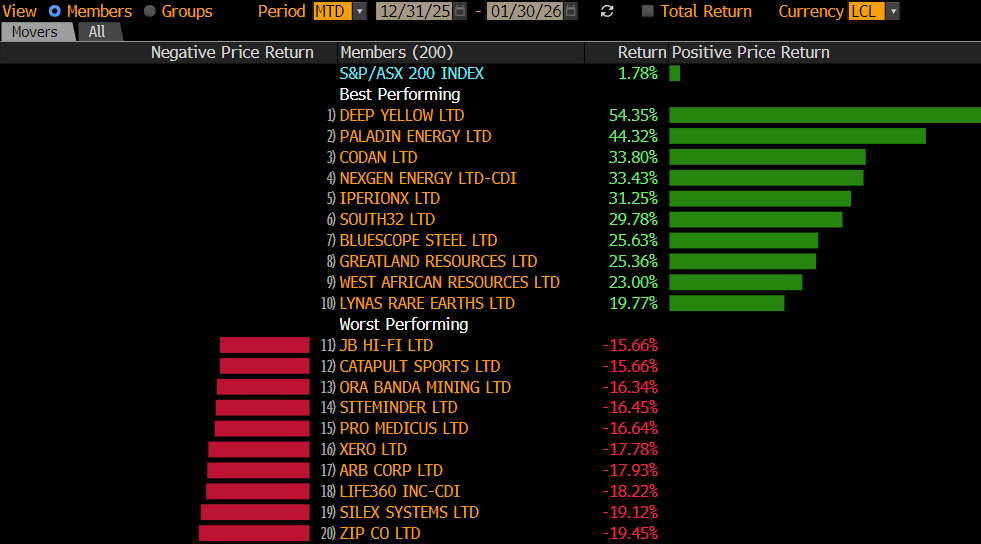

On the stock level, there was pronounced volatility over the 5-days with 12 stocks rallying/declining by over 10%, the same number as last week. The winners’ enclosure was dominated by uranium, gold and diversified miners, while the naughty corner contained primarily lithium and rare earth stocks. A very polarised week by the resources.

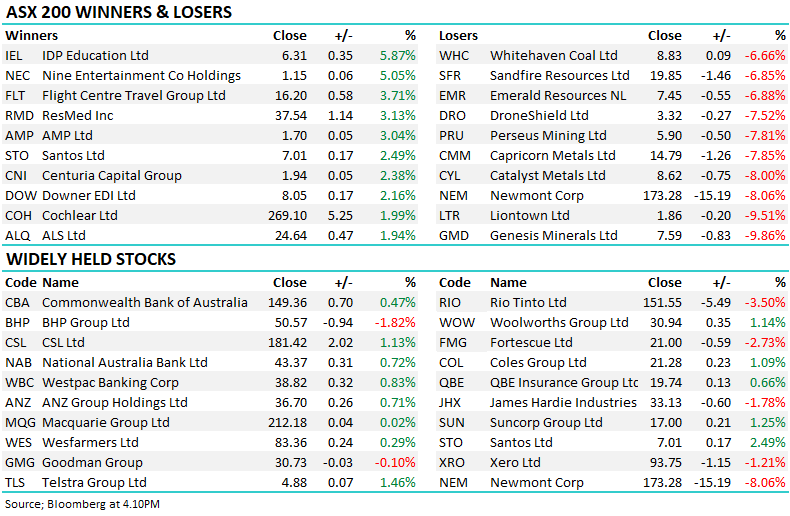

Winners: Deep Yellow (DYL) +23.5%, Northern Star (NST) +10.5%, Santos (STO) +9.9%, Capstone Copper (CSC) +7%, ASX Ltd (ASX) +6.4%, Regis Resources (RRL) +6.3%, Reece (REH) +6.3%, BHP Group (BHP) +5.2%, and South32 (S32) +5%.

Losers: DroneShield (DRO) -29.8%, Iluka (ILU) -21.1%, Liontown (LTR) -14.9%, Pilbara (PLS) -14.9%, Lynas (LYC) -11%, IGO Ltd (IGO) -10.4%, Alcoa Corp (AAI) -10%, Zip Co (ZIP) -8.3%, Aristocrat (ALL) -7.8%, SiteMinder (SDR) -7.3%, and Seek (SEK) -7.1%.

The market-focused news evolved from a hot local CPI on Tuesday to market disappointment with Trump’s nomination for the position of Fed Chair:

- The market opened with a bang on Tuesday, rallying almost 1% as the resources sector took off, led by gold, which posted another all-time high around $US5,100/oz – it was just the beginning.

- Equities fell away on Tuesday after a hotter-than-expected December CPI reading firmed market expectations of a February rate hike from the RBA – a 68% chance according to futures markets by Friday’s close.

- The $A pushed above 70c for the first time in 3 years following the hawkish inflation read and strong commodities market.

- The ASX drifted on Thursday, but the resources again fired as gold traded above $US5,500 and copper popped over +7% in the blink of an eye.

- On Friday, President Trump announced his pick for the Fed’s top job was Kevin Warsh, not the most dovish candidate, sending the $US soaring to its best day since July as hopes of deep rate cuts faded.

- Trump’s announcement on Friday saw the music stop playing for gold and commodities, with the precious metal plunging 16% from its all-time high as global miners corrected their recent strong moves.

Overseas markets were mixed into the weekend following news around the Fed Chair. In Europe, it was another solid session with the German DAX advancing +0.9% and the UK FTSE +0.5%. However, in the US, the news that Warsh was Trump’s pick for the Fed Chair position sent the S&P 500 down -0.4% while the rate-sensitive Russell 2000 fared worse, closing down -1.3%.

- The SPI Futures are calling the ASX200 to open down -0.7% on Monday, with the miners likely to endure a tough start to February. Gold ETFs in Canada were off ~11%, Copper ETFs in the US were down ~10%, Uranium stocks fell ~7% and Lithium names were down ~5%. The AUD fell back to US69.64c, down 1.2% on the session.