CSC is a Canadian miner that has recently dual-listed on the ASX, and it’s on a higher production tier relative to Sandfire at present. CSC has a strong growth pipeline (Mantoverde, Santo Domingo) with all assets in Americas (USA, Mexico, Chile), where BHP already operates.

Importantly its large enough to move the needle, small enough to buy with a clean portfolio. Its currently trading on the cheaper side whereas SFR is on the more expensive side relative to historical multiples. However the reason for the valuation differential is unlikely to go away, the ASX now has limited pure copper options post BHPs acquisition of OZ Minerals while North America has plenty.

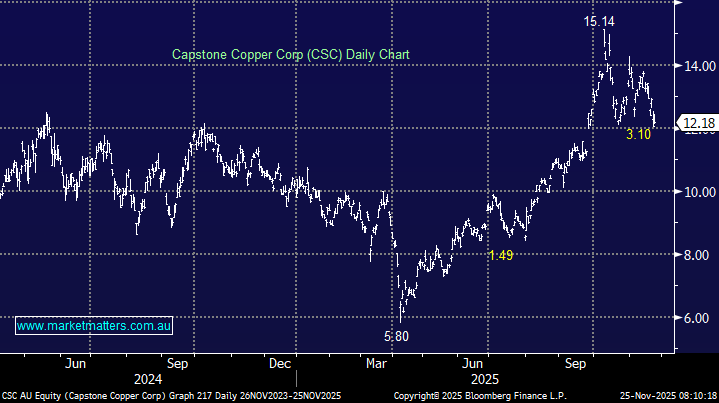

- We like CSC in line with our bullish copper stance plus the potential that it could be on a suitors radar.

MM is bullish towards CSC into 2026

Add To Hit List