Hi Angela,

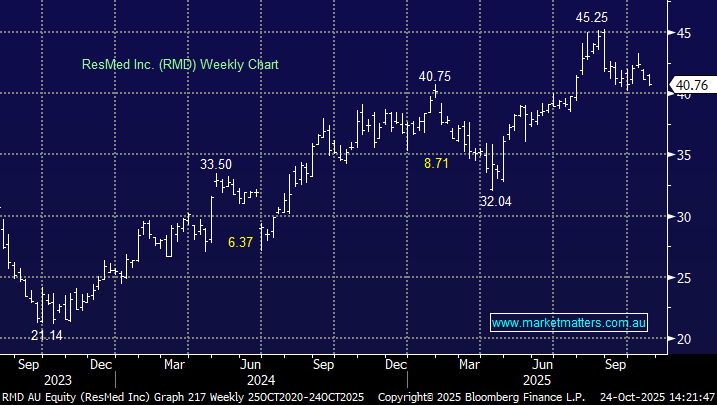

A few growth stocks have struggled in the last month, we’ve covered a few in this report although they’ve primarily been in the tech, as opposed to healthcare space. RMD is still up more than +10% year-to-date making it one of the sectors top performers, one where the majority of names have actually retreated through 2025. We see nothing sinister in the selling with some profit taking ahead of its result while competition is set to increase:

- Philips is re-entering the CPAP market after a significant recall in 2021 due to health risks associated with the foam used in their devices. The recall led to a $1.1 billion settlement in 2024 and a temporary halt in production and sales – great news for RMD at the time.

NB CPAP stands for Continuous Positive Airway Pressure. It is a medical device used primarily to treat obstructive sleep apnea (OSA), a condition where a person’s airway collapses or becomes blocked during sleep, causing breathing pauses.

ResMed faces a big test next week with analysts expecting strong sales growth and a tough year-over-year comparison in fiscal 1Q.

For the quarter, consensus is:

- Revenue $US1.33bn

- NPAT: $US368.8m

- EPS US0.25c

FY26 guidance will be more important than the earnings themselves.

For FY26, the market is looking for growth in revenue of 9% with earnings expected to be 12.8% higher by year end, at $US1.587b. Forecasts moving forward will be key with competition set to increase – its “game on” as RMD’s CEO said recently.

- We believe RMD is solid value ~$40, trading on 23x, around 1 standard deviation below it’s 5-year average, and they do have a history of beating at earnings time. The average earnings ‘surprise’ since 2015 is 8.1%, leading to an average positive share price reaction of +4.8% over that time frame, though in the last few years, the share price reactions have been more hit and miss even as earnings have beaten at 8 of their last 10 quarterlies.