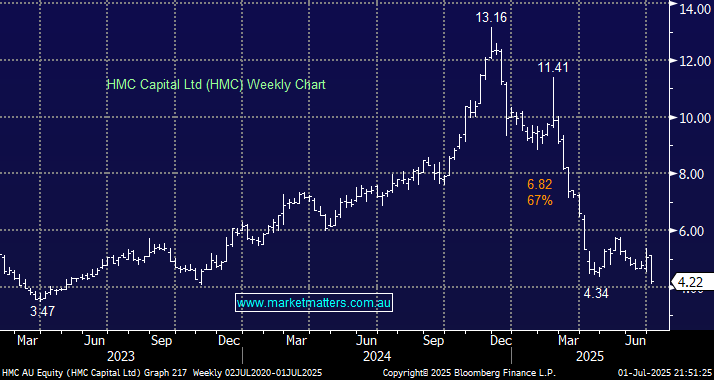

It’s been a tough period for HMC Capital (HMC), the alternative asset manager that grew funds very quickly to $18.5bn, amid ambitions to grow this to $50bn over the next 3-5 years. The pressure compounded yesterday after they announced the delay in settling its $950 million acquisition of Neoen’s renewable energy assets, plus, they also announced the unexpected departure of Angela Karl, Head of Energy Transition.

Firstly, the deal to buy Neoen’s Victorian renewable energy portfolio was inked in December 2024, and formed the cornerstone for HMC Capital’s Energy Transition Platform (Chaired by Julia Gillard), which is aiming to raise $2 billion from institutional investors. The delay is not the main issue here in MM’s view, but it does mildly erode confidence in HMCs ability to execute.

Secondly, and more importantly, the loss of Angela Karl is another incremental negative that implies a greater level of instability or friction in strategic direction. Angela was poached from QIC Global Infrastructure in early 2024, is very experienced in the energy and utilities sectors, and was going to be instrumental in the roll out of HMCs energy transition business. There has also been a change in tack around strategy, with the merging of the the Neoen VIC Portfolio and Stor Energy battery platforms to form one energy platform led by Stor’s CEO Gerard Dover.

- There is a lot of investment banking B/S (excuse our French) used in the HMC announcement yesterday, with ‘strategic partnerships’ being explored, ‘portfolio optimisation’ under consideration, but the reality is, this is a business that relies on growing funds under management (FUM) i.e. raising money, and raising money is all about confidence. Confidence comes from stability and execution that are inline with stated objectives. This has been an area where HMC has clearly struggled in recent times, and this is the area they need to address.

That said, David Di Pilla (CEO) is an exceptional operator with plenty of skin in the game, owning 21% of the company, and we do back him to turn things around. In the short term, we think they need a circuit breaker, such as backing by a larger, well-known global investor.

- HMC also announced yesterday a slight tweak to how they are paid for managing the DigiCo REIT (DGT), a positive sign of their medium—to long-term mindset. We don’t view this as significant in the context of yesterday ~’s 17% fall in the share price.

We hold HMC in the Emerging Companies Portfolio and believe the longer-term thematics for this business remain solid. However, they are grappling with short-term headwinds that have seen the stock move from ~$13 to around $4. Our intention is to increase the weighting in HMC on signs that they have been successful in attracting additional capital.

MM is neutral to mildly bullish HMC ~$4

Add To Hit List