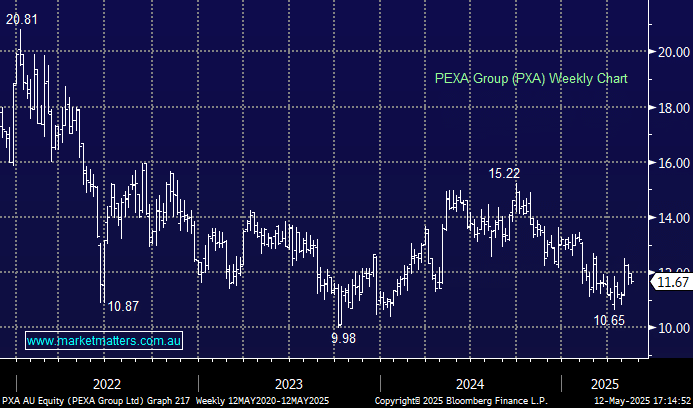

PXA -1.19%: Posted mixed 3rd quarter results showing continued market dominance and growth in Australia but slightly weaker figures in the UK.

- 871,000 transactions processed in Australia, +4% y/y, 90% market share

- UK remortgage volumes declined -4% y/y, 24.5% market share

- Digital solutions subscription revenue +11% y/y

- Consulting revenue +78% y/y

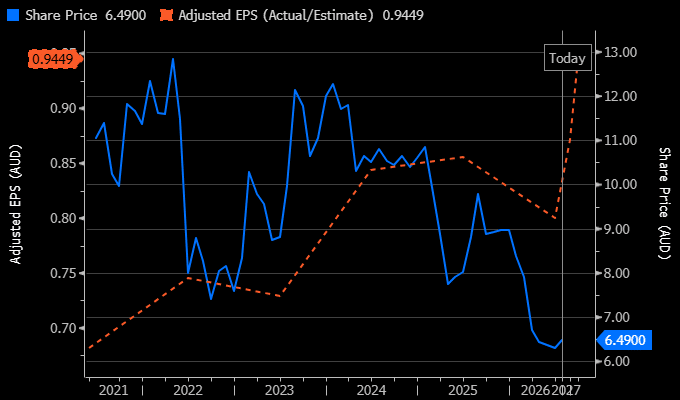

FY25 earnings were reaffirmed, with revenue growth at +13-19% and group EBITDA margins of ~34%. While market share did decrease in the UK over the quarter, market penetration remains relatively low, with the recent approval to become an authorised payment institution will allow the business to expand and deepen market relationships. Management did release a statement around ongoing uncertainty in the macro environment and potential for guidance revision, though this isn’t necessarily cause for alarm as it appeared be new CEO Russell Cohen playing it cautiously while he undertakes a business review, due in the August result.

MM remains long and bullish PXA

Add To Hit List