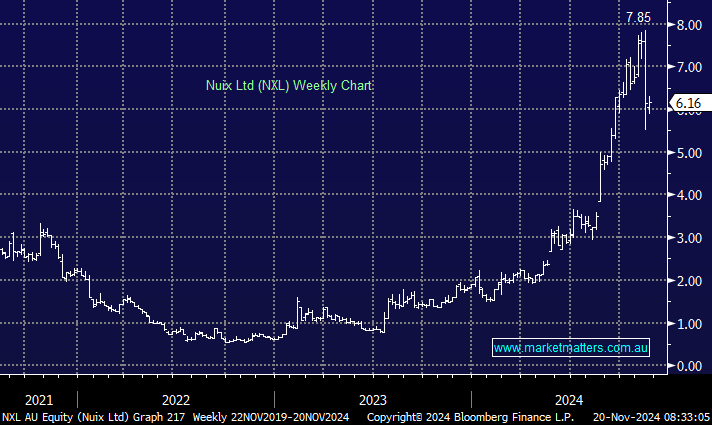

NXL is a company with a storied (relatively short) history on the ASX, listing in December of 2020 at an IPO price of $5.31, having raised $400m through Macquarie, and was one of the hottest IPOs of the year. Shares were above $12 by January 2021, but things started to unravel. Financial performance struggled, the CEO resigned, their accounting practices were questioned, and the regulators investigated disclosures provided during the IPO process. It was a classic cluster of issues that sent shares down to ~50c. More recently, things have turned, and they are once again living up to their potential, reaching a market capitalisation over $2bn.

Nuix is a software company that processes and deciphers complex data very quickly. It’s used in a lot of areas, including legal, compliance, cybersecurity, and Government agencies globally. For example, many government entities rely on Nuix’s solutions to manage large-scale data governance projects, ensuring compliance with privacy laws and regulatory requirements, such as the handling of public records, sensitive personal data, analysing digital evidence and communications in investigations ranging from organised crime to terrorism i.e. they operate in a growing area, and have a great set of solutions that are highly regarded.

The shares recovered strongly from 50c to hit a recent high of nearly $8, before last week’s trading update provided at their AGM, which knocked the stock back to ~$6. While they reiterated their FY25 outlook for all key targets, it seems the market reacted negatively to a comment made that “sales are not linear over the course of the year, and our current expectations are that growth will be weighted towards the second half of the fiscal year”. In other words, we need to trust they’ll come home with a wet sail in the 2H of FY25. While they have not traditionally had a 1H/2H skew in their business, they are dependent on the timing of renewals and closing new business, which can be lumpy and highlights that a greater proportion of renewals are scheduled for the 2H and the timing of new business closing might be also.

- In our view, this does not highlight a change in demand or execution success. As such, we view the commentary as being on track and in line with prior communications, with a 20% pullback in the shares providing an opportunity.

MM is now interested in NXL ~$6 following recent weakness

Add To Hit List