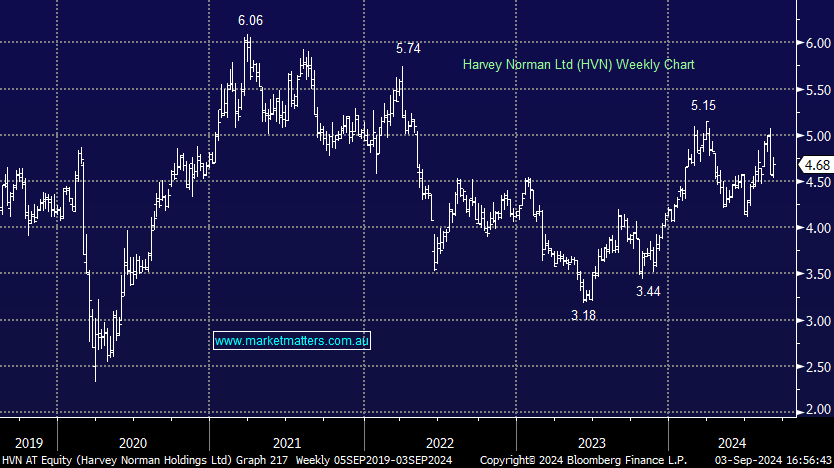

HVN +1.74%: Has been a big underperformer relative to some of the other discretionary retailers YTD, up 12% versus JB Hi-Fi (JBH) up 54%. A better share price performance from JBH is justified given their better financial performance, however, HVN now trade on a ~30% discount from a relative PE perspective vs JBH, a ~40% discount to the ASX Industrials (ex-Financials) and an EV/EBIT multiple (ex property) for FY25e of ~9x, or in other words, it screens value. We are in a market that is gravitating towards the strength, with earnings certainty & safety being highly regarded, however, that will change at some point, trees don’t grow to the sky, and being open to the laggards is important for what may come next.

- Our view last month on HVN was anchored to JBH, suggesting we still prefer JBH, however given the relative moves since, HVN is starting to look interesting again.

MM sees value in HVN ~$4.70

Add To Hit List