Hi Michael,

The sell-off was short lived. The announcement referred to CBA putting their total Lenders Mortgage Insurance (LMI) business up for tender. At the moment, HLI has most of it, but not all (QBE has some). When that happens at the end of 2025, they might lose the contract entirely, or they might win the full deal, and if that were to happen, clearly that is a positive. In a situation like this, it highlights 1. the risk of having over 50% of your business with one client & 2. There is not a huge ‘moat’ around the business. That said, the focus should be on what HLI looks like if they lose the contract all together i.e. look after the downside and the upside will take care of itself!

The impact of any loss would be felt mostly in 2027 given the nature of the business. Providing LMI requires capital, so when less LMI is written, HLI would require less capital, some of which would come back to shareholders via capital management, offsetting the loss of earnings as their book goes partially into run off. Capital management would involve more aggressive buy-backs and other initiatives.

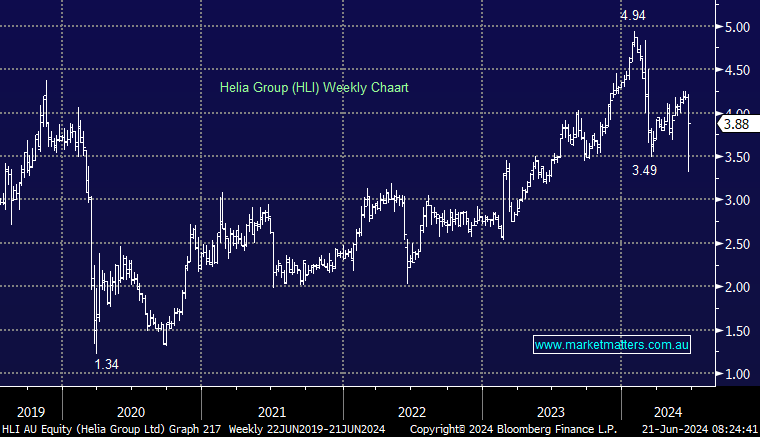

Macquarie values HLI’s current policies + future profits from them at $5.32, and then applies a discount to get their 12 months target price of $3.90, which they kept unchanged this week. In essence. If they lose the contract, it will be mostly offset by capital management, and if they win all the CBA business, it will be net positive. It was a knee jerk reaction from the market when this was announced, and we should have been quicker taking this opportunity given the stock resides on the Hitlist of our Income Portfolio. We think the stocks is a hold ~$3.80, but a buy into headline driven weakness.