What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

Iran and a number of its allies launched a large-scale drone and missile attack upon Israel on Saturday night in retaliation for a suspected Israeli strike on an Iranian diplomatic complex in Syria. The prospects of a full-blown conflict in the region have increased dramatically over the last week, with at least nine countries involved in Saturday’s conflict, projectiles fired from Iran, Iraq, Syria and Yemen were downed by Israel, the US and France, as well as Jordan. Following Iran’s attack, the U.S. pledged “ironclad” backing for Israel, but President Joe Biden made it clear the US would not participate in any offensive operations against Iran.

- Joe Biden has a tough few months ahead of him before he even contemplates Donald Trump – this could make or break his campaign.

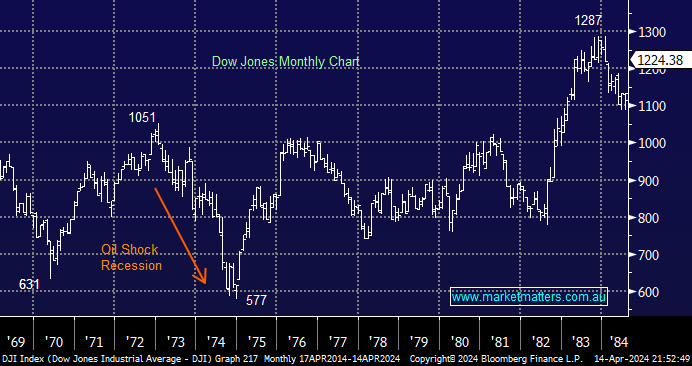

The current events are reminiscent of the 1970s energy crisis, which was caused by America’s support of Israel during the Yom Kippur War against Egypt. Oil-producing Arab countries boycotted the US as punishment for their stance. At the time, the embargos sent oil surging from sub-$US20 to more than $US60 in just a few years. It’s easy to comprehend the dramatic impact on both stocks and countries that were major users and net importers of oil.

- Equities suffered a painful bear market through 1973 and 1974, which became known as the oil shock recession—the S&P500 fell ~40% before recovering strongly.

As we alluded to last week, oil can advance another 10% at this stage. However, let’s hope the situation doesn’t get any worse on both the humanitarian and economic fronts—another full-blown Middle East crisis could easily send stocks down over 10% after their stellar advance over the last six months. At this stage, MM is holding elevated cash levels and looking for buying opportunities, which feels on point.

- Crude oil can re-test $US100 in the coming months as geopolitical tensions continue to escalate in the Middle East.

MM is bullish towards crude oil short-term

Add To Hit List

Successful investing requires a number of moving parts, but one important facet is the recognition that equities are an excellent asset class over the medium to long term – although that’s not always true of individual companies/sectors. Investors who had the resolve and patience to accumulate stocks during the 1973/4 pullback were looking good a few years later and extremely good a decade later. While MM isn’t yet looking for a ~10% pullback, we are always open-minded, and stocks aren’t cheap at the moment; hence, if we do see another oil shock, the retracement could be deeper than we are currently expecting.

- We plan to slowly increase our “risk exposure” into weakness over the coming weeks/months. We’re currently overweight cash, so a pullback is welcome.

MM remains cautiously bullish towards US stocks

Add To Hit List