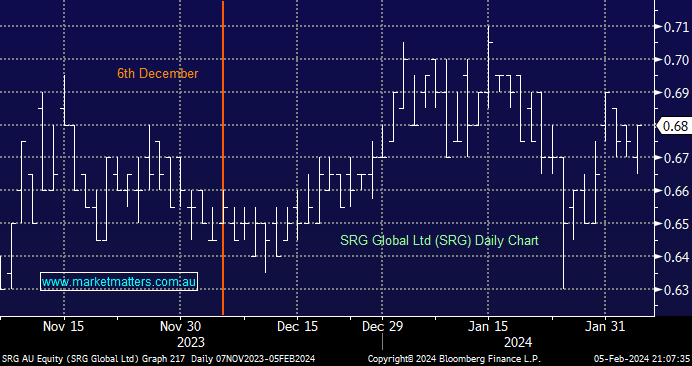

Construction services company SRG is a high-quality business that looks set to win ~$1bn in contracts this financial year, with cash conversion likely to rise through FY24, helped by its stable of top-quality clients, including the Government, BHP (BHP) and South32 (S32). It’s still cheap, below 70c, making it an excellent opportunity at the smaller end of the market. Plus, a forecasted yield above 6% is a nice bonus.

- We remain bullish on SRG, initially looking for a move to ~85c; we hold SRG in our Emerging Companies Portfolio.

MM is long and bullish on SRG

Add To Hit List