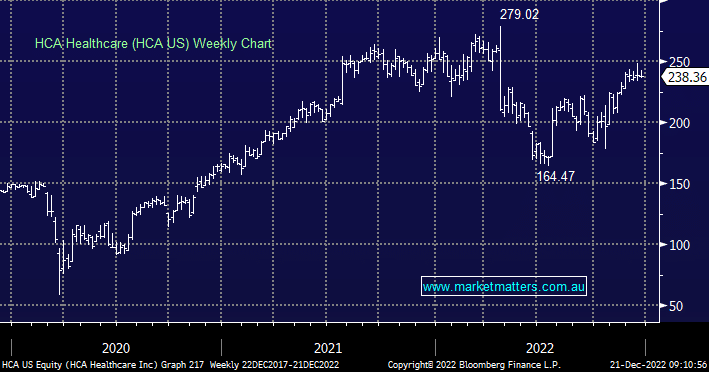

HCA is the largest hospital operator in the US providing around 5% of the country’s hospital services. Generating ~US$60bn a year in revenue and a profit of $US5bn, this is a big player operating ~50,000 beds in ~200 hospitals around the country, along with free-standing surgery centres and urgent care facilities. We originally bought HCA largely on valuation grounds given it has a key market position and was trading on just 10x with a tough year in FY22 well and truly priced in. The share price has now started to factor in a recovery in earnings in FY23, and we now ponder whether or not the rerate has further to run, with MM’s up ~41% in 5 months.

- HCA is now trading on an Est PE of 13x which is not high, but is a premium to the sector and we think the upside is now more limited.

MM is bullish (just) HCA, targeting ~US$250

Add To Hit List