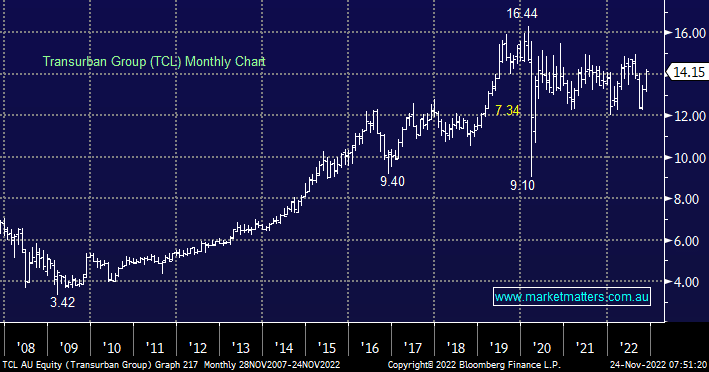

We continue to like TCL for a defensive earnings stream backed by critical and irreplaceable infrastructure with a compound annual growth rate of ~8.5% over the next 5 years which actually benefits from inflation, it may have experienced a relatively quiet few years but we remain firm believers in this toll road operator.

NB, we currently hold TCL in our Active Income Portfolio.

- We can see TCL breaking its January swing high into 2023.

MM remains bullish and long TCL around the $14 area

Add To Hit List