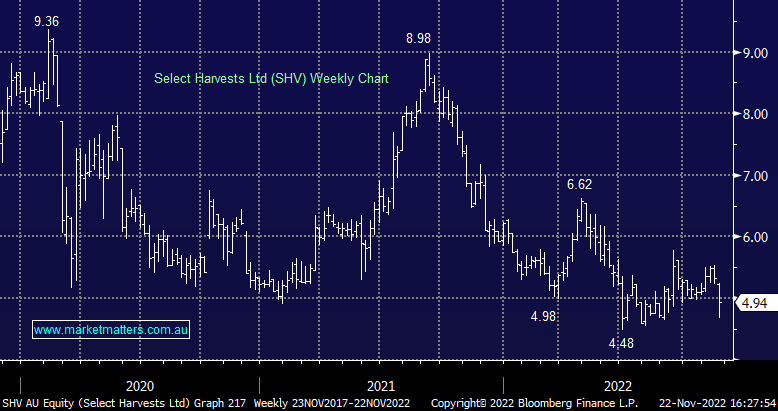

SHV -4.63%: the FY result was out today for the almond grower, with shares weaker on a slightly disappointing report. EBITDA was in line at $37.9m, however, the revenue of $200m and NPAT of $4.8m were slight misses to consensus. They produced 29kmt, right in the middle of guidance, while the selling price of $6.80/kg was slightly above expectations. The almond market remains oversupplied with prices at cyclical lows, however, there are signs the outlook is starting to improve as the drought in California weighs on crops, though this is taking longer than we expected to play out. Costs are also expected to be higher in FY23 given high fertilizer prices, though this is partially offset by lower water prices. The company said recent heavy rainfall across Australia is expected to have a minimal impact on the current crop.

MM is getting frustrated with our holding in SHV in the EC portfolio – so many moving parts!

Add To Hit List