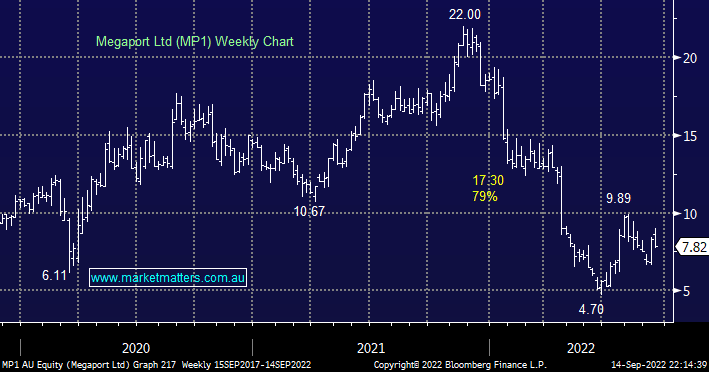

MP1 is a $1.2bn software-based elastic connectivity provider that could fit into either of our Flagship Growth or Emerging Companies Portfolios although its high volatility is likely to dictate a relatively small position in the former.

- We like management’s current focus on profitability and commitment to achieving free cash flow breakeven by the end of FY23.

- Last month the company announced a 40% lift in revenue for FY22 to $110mn which while in line with expectations was a definite step in the correct direction.

While we can easily see MP1 trading back into the $11-12 area this year, we’re not considering a retest of the $20 region.

MM likes MP1 under $8 as an aggressive play

Add To Hit List