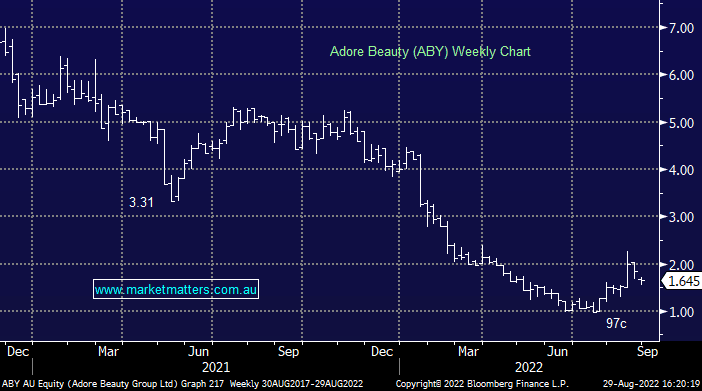

ABY -10.60%: the beauty products e-commerce business reported disappointing numbers and a softer outlook, weighing on the stock today. Revenue was a small miss to expectations despite being up +65% for the year, coming in at $199.7m. EBITDA at $5.3m was marginally below the consensus estimate as well, though EBTIDA margins were in line. FY23 expectations will have to be revised lower with the company saying sales are running at -28% on the same period last year in the first 7 weeks. While this number will normalize given it is cycling the boost from COVID lockdowns, the company doesn’t expect to see double-digit growth until the second half. Disappointingly, margins are expected to drop below the 2-4% in FY23, though they provided medium-term guidance of 8-10%for FY27, which highlights the benefit of increasing scale and growing the private label offerings.

MM is neutral ABY – today’s result was weaker than we hoped

Add To Hit List