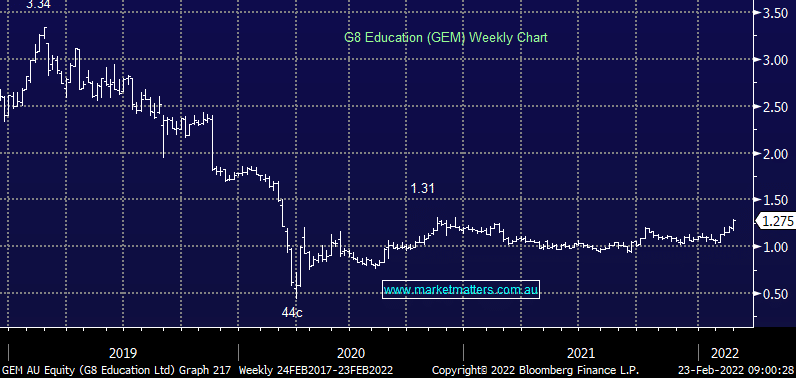

Childcare has been a very challenging business over the last 2 years and being one of the largest operators in the space, G8 has certainly felt the brunt of these challenges Yesterday, they reported FY21 results that were around 5% better than expectations and in MM’s view, show signs the turnaround is gaining traction. They also announced a share buy-back , reinstated the dividend and announced a 6% fee increase to help boost margins. Their balance sheet is in decent shape post a COVID induced recapitalisation, and there is a high probability that dividends of at least 6cps are sustainable and will grow from FY23 and beyond as occupancy levels rise, putting it on a yield of at least 4.7% fully franked.

MM is now bullish GEM, looking to add it to the Income Portfolio

Add To Hit List