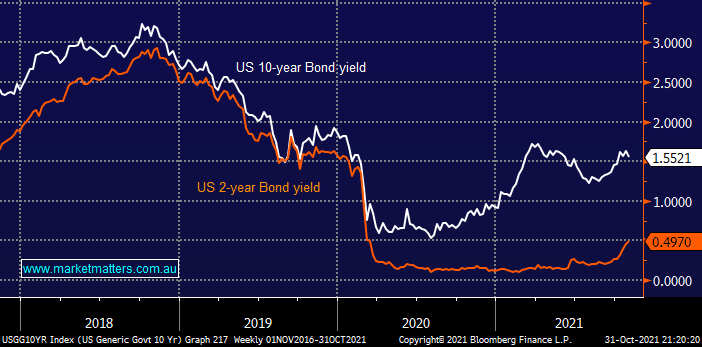

No real change as global bond yields continued to rise from their late August low as inflation spikes, the standout has been the ongoing contraction of the yield spread which can be simply interpreted as follows:

- Short dated bonds like our own 3-years and US 2-years are seeing their yields rally sharply as markets believe rate hikes are inevitable from their current central bank engineered historically low levels.

- Conversely the longer dated yields like the 10-years are showing investors and traders are not convinced the global economy is strong enough to keep growing in the face of such hikes.

We feel after these recent sharp adjustments across the yield curve it’s close to wait and see time towards both central banks and the underlying economies which should offer some short-term respite to equities but we caution that due to supply chain constraints in particular we could see some disconcertingly strong prints of inflation over the coming next 6-months.

MM remains bullish bond yields from current levels into 2022

Add To Hit List