Why is South32 (ASX:S32) down ~7%?

South32 (S32) has flagged another cost blowout at its flagship zinc-lead-silver project in Arizona, pointing to tariffs, inflation, rising input costs and contractor underperformance. The group now expects to spend around US$3.3bn to develop the Taylor deposit, almost double the ~US$1.7bn estimate outlined at approval. Despite the delays and higher costs, S32 struck a more constructive tone on the outlook, extending the mine life by five years to 33 years and pointing to stronger long-term returns, with expected earnings of roughly US$650m.

South32’s update also pointed to a 52% lift in ore reserves and further resource growth at the adjacent Peake deposit, supporting potential future copper production. However, the cost blowout marks another setback for the group, coming just a month after it moved to mothball its Mozal aluminium smelter in Mozambique due to unreliable power access. Despite the recent challenges, S32 shares have rallied ~20% over the past year to ~$4.26, implying a market value of around $19bn.

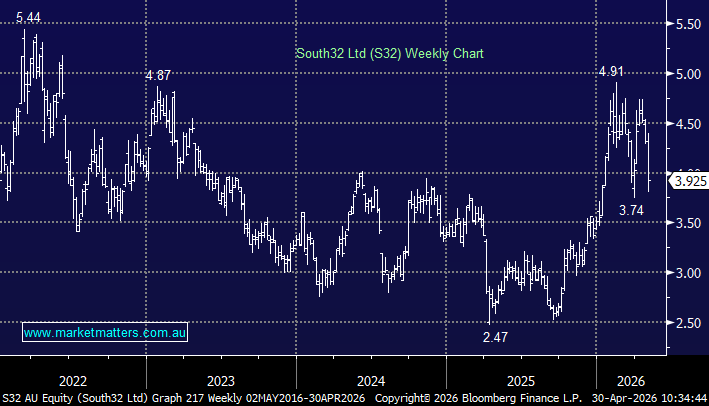

- S32 will start to look interesting to MM ~$3.60.