Why is Evolution Mining (ASX: EVN) down3% when the Gold Sectors rallying?

Evolution Mining’s (EVN) Q4 FY26 update was a mixed result, with record cash generation overshadowed by rising cost expectations for FY27:

- Production softer than expected: Q4 gold production of 179,655oz was down 1.1% YoY, with Mungari production falling 11% QoQ.

- FY27 cost headwind: Inflation is expected to lift all-in sustaining costs (AISC) by 4–5% (A$150–160/oz) in FY27.

- Higher investment: Sustaining capex is expected to increase by $50–60m, while mine development spend is forecast to rise $130–160m.

- Mt Rawdon closure: No material change to group production capacity beyond the planned closure of Mt Rawdon.

- Balance sheet remains a strength: Record FY operating cash flow of $1.39bn and a $1.35bn net cash position were largely overlooked by the market.

The FY27 outlook broadly matched its expectations, suggesting the share price weakness reflects investor caution ahead of formal FY27 guidance, due with the FY26 result in August. Plus, EVN enjoyed almost 7% bounce of its lows on Wednesday making it vulnerable to some short-term selling.

Bottom line: The market is focused on margin pressure rather than operational performance. While EVN remains fully leveraged to higher gold prices through its unhedged portfolio, investors are increasingly concerned that cost inflation could erode the benefit of a strong gold price environment.

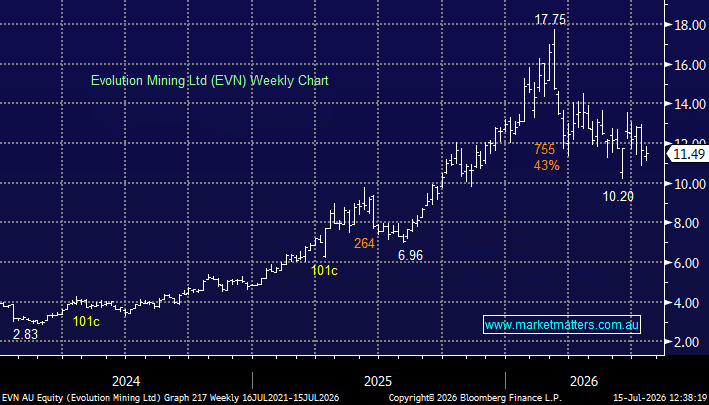

- We remain bullish towards EVN believing it represent good value below $11.50.