Weak earnings + Trump Tweets put the kibosh on the market (FMG, BLD, IFL, GEM, JHC)

WHAT MATTERED TODAY

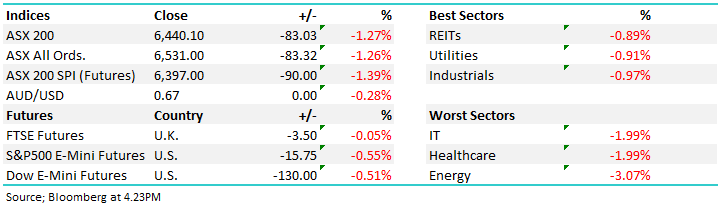

Volatility was back in town today thanks to Mr Trumps barrage of tweets over the weekend and subsequent escalation of the China – US trade tussle. US Futures opened sharply lower this morning building on Friday’s losses and that put pressure on stocks from the get go. Amplifying the negativity was company reporting that was generally weak, particularly when it came to outlook commentary for FY20. The table below provides some fairly sombre reading with the average decline of those companies that released results today of over 9%.

While it was clearly a negative session, the market did open on its lows and improved throughout the day closing near the session highs, with a lot of activity through the SPI Futures market in the last 15 mins of trade, around 7000 SPI Futures contracts traded pushing the market up +30pts is quick succession, about ~$1bn worth of exposure…BIG. That trade was around 4pm while news broke on Bloomberg around 4.55pm saying **TRUMP SAYS CHINA CALLED, WANTS TO RESTART TRADE TALKS** with no further detail. Reminds me of the Elmo ap that I still have on the my phone from when the kids were younger….US Futures have just turned positive.

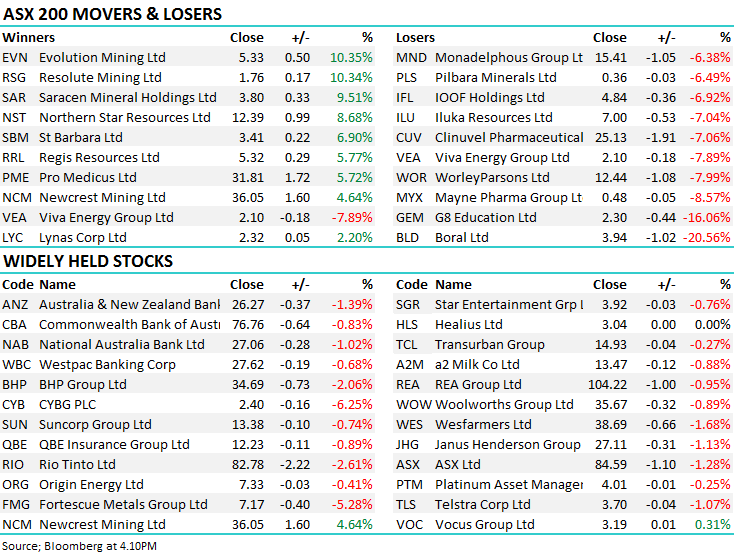

At a sector level today, it was all red with energy hardest hit down by more than 3% while the defence REITS help up well – Gold bounced from recent weakness with the likes of Evolution (EVN) +10% & Northernstar (NST) +8.68%. Asian markets were understandably lower while US Futures were down but recovered around 1% from their lows during our time zone.

Overall, the ASX 200 lost -83pts today or -1.27% to 6440. Dow Futures are now trading down -130pts /-0.51%.

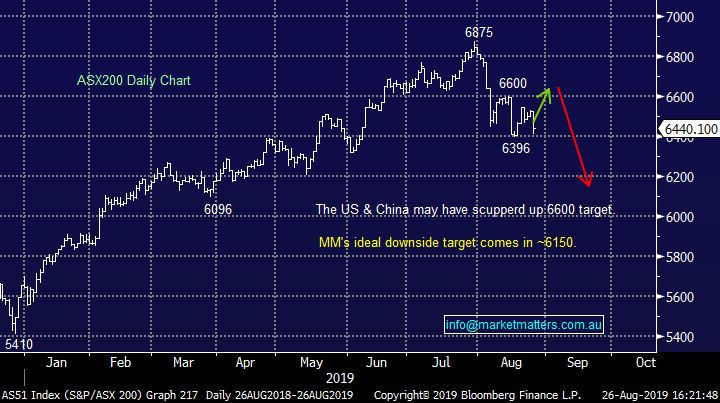

ASX 200 Chart

ASX 200 Chart

CATCHING OUR EYE;

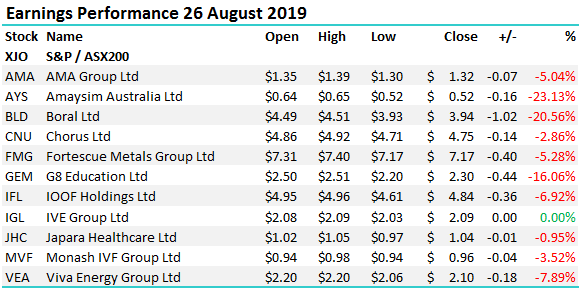

Stocks today: The table below looks at the share price performance of those companies that reported today. Not a pretty picture today unfortunately.

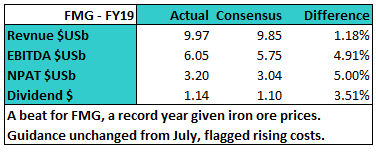

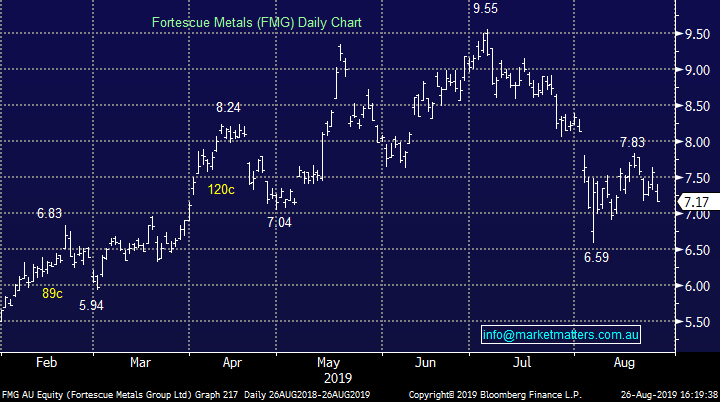

Fortescue Metals (FMG) –5.28%%; managed a record profit of $US3.2b thanks to the iron ore price tailwind seen in the second half of the year, topping up its total dividend to $AU1.14 – to put this in context, FMG was trading below $1.50 for a period in 2016. Their outlook remained unchanged, with Fortescue maintaining 170-175mt in shipment expectations, and costs to be in the range of $US13.25-13.75/wmt. This is a reasonable jump in costs vs the FY19 average of $US13.11/wmt and reflects the general rising costs theme in the resource space seen by many of Fortescues peers.

We remain keen buyers of weakness across the iron ore names.

Fortescue Metals (FMG) Chart

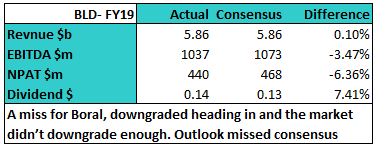

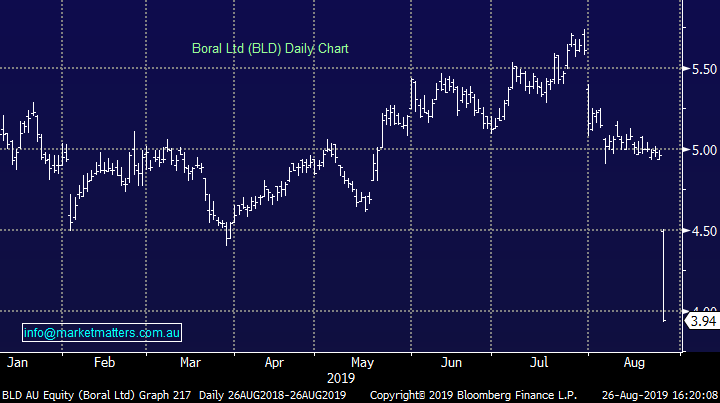

Boral (BLD) –20.56%: The stock took a bath today after they missed FY19 expectations and were more downbeat about the outlook for FY20. Back at the start of June, BLD held an investor day which split analyst opinion, Morgan Stanley who was bullish the stock said the most important aspect of the day was ‘no news is good news’ in terms of downgrades and they became more positive on the building material company. Credit Suisse was on the other side of the ledger downgrading BLD at the time, as it turns out, not aggressively enough – although they were right. BLD are facing a barrage of challenges, similar to Adelaide Brighton (ABC) and the expectations for a decline in earnings of 5-15% in FY20 versus markets expectations for a 1% decline was the nail in coffin today. A difficult period ahead for BLD.

Boral (BLD) Chart

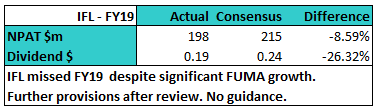

IOOF (IFL) -6.92% Reported FY19 earnings numbers this morning and the stock was down as a result. They missed on the profit line and they cut their dividend saying “In one of the most challenging years for our company and for the industry, we have focused on the imperatives of stabilising the business, with a view to delivering better outcomes for our clients and our shareholders”

While the result was a miss, the underlying performance of the business was reasonable. Total funds under administration and advice (FUMA) increased while their adviser net promoter score was up +17% versus the industry average which was down. While it’s going to be a long road for IFL and the acquisition of the ANZ Wealth Business was completed at the wrong time, the decision today to cut the dividend, conserve cash, protect the balance sheet and bed down for a challenging operating environment we think is the right one.

IOOF (IFL) Chart

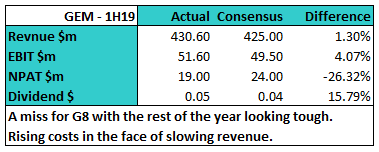

G8 Education (GEM) –16.06%; a tough start to the year for G8 which saw earnings squeezed by higher costs and an oversupply of childcare spaces dragged on occupancy and thus earnings. The company remains cautious heading into the year-end despite seeing signs of moderating supply growth and some benefit from the Government’s childcare subsidy. Full year EBIT guidance for $140m-$145m was well below the market’s expected $172m and the stock was smashed as a result.

G8 Education (GEM) Chart

Japara Healthcare (JHC) -0.95%; the aged care provider outperformed the market today but couldn’t finish higher despite an in line result. The space has come under pressure with the Royal Commission into providers coupled with wage inflation rising faster than CPI squeezing profits. Revenue was up strongly for Japara, however this all came from two developments coming online as well as a few acquisitions. Occupancy rates fell marginally, and FY20 isn’t expected to see too much in the way of a recovery. We own competitor Estia (EHE) in the Income portfolio which was upgraded by both Macquarie and UBS last week after they reported.

Broker moves;

- Ardent Leisure Upgraded to Buy at Baillieu Ltd; PT A$1.55

- Costa Downgraded to Hold at Morgans Financial; PT A$3.48

- Steel & Tube Upgraded to Neutral at Forsyth Barr; PT NZ$1

- Comvita Upgraded to Outperform at Jarden Securities; PT NZ$3.61

- Skellerup Cut to Underperform at Jarden Securities; PT NZ$2.05

- Orocobre Downgraded to Neutral at Macquarie; PT A$2.50

- Hansen Tech Downgraded to Sector Perform at RBC; PT A$4.15

- Skellerup Downgraded to Hold at Deutsche Bank; PT Set to NZ$2.45

- Rhipe Upgraded to Buy at Blue Ocean; PT A$3.60

- ERM Power Downgraded to Hold at Morgans Financial; PT A$2.47

OUR CALLS

No trades today.

Major Movers Today

Have a great night

James, Harry & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence