Tech leads market through 6100 (NWL)

WHAT MATTERED TODAY

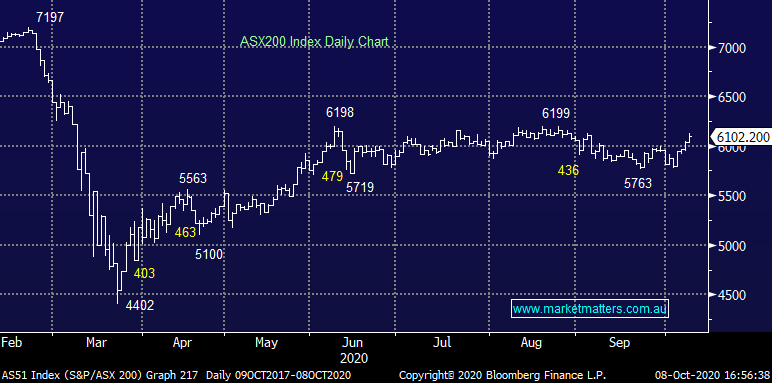

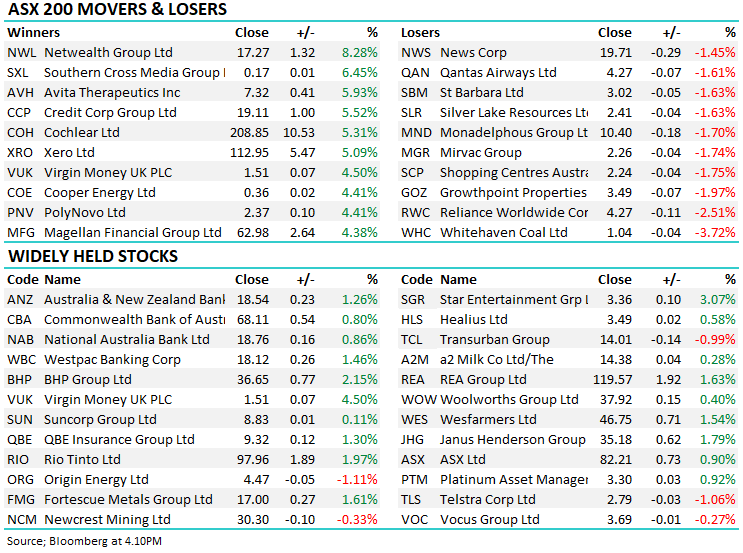

Another strong session for the ASX with the market cracking back up through 6100 with the IT stocks leading the charge, particularly the BNPL space spearheaded by Zip Co (Z1P) which rallied 9% while online accounting business Xero (XRO), also a holding in the MM Growth Portfolio put on more than 5% - our skew towards the sector felt good today, although a few good days does not a summer make ! I cover off some of the aspects catching my eye today in a quick ~5 min recording below.

Wrap up of today’s trade ~5 mins

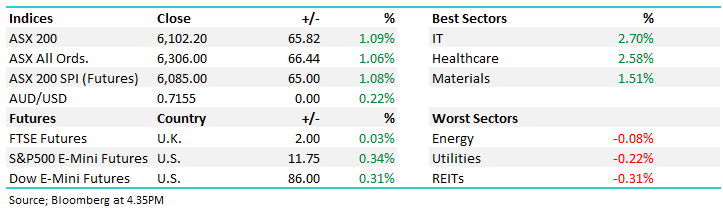

By the close, the ASX 200 was up by 66pts / +1.09%. Dow Futures are trading up 97pts/+0.35%

ASX 200 Chart

ASX 200 Chart

CATHCING MY EYE

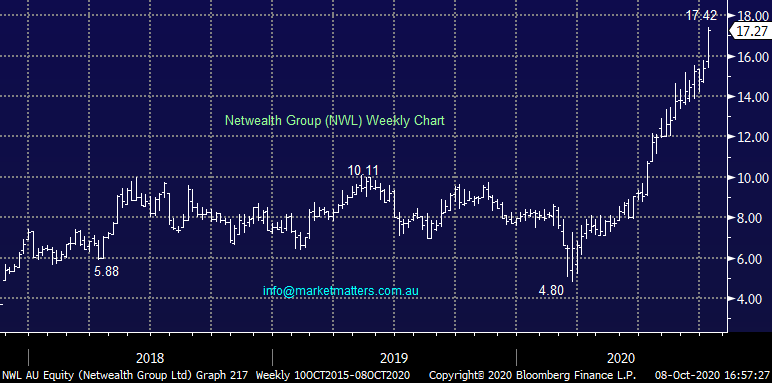

Netwealth (NWL) +8.28%: FUA update today was a positive – there remains no sign that the flow into the independents is slowing down at this point. FUA grew 8% in the September quarter in a flat market with the ANZ wealth transition doing the bulk of the work. FUM was also substantially higher at 11% on the 4th quarter. A large portion of earnings from platforms come from the cash spread – the difference between interest earnt and paid to clients on cash holdings. With the RBA holding rates near zero, this spread has tightened significantly and been a drag on earnings in the space, Netwealth today confirmed that any further rate reductions would be absorbed by the company. Consolidation will continue in the space given the fragmentation in the independent offering – we recently saw Praemium and Powerwrap come together, it won’t be the last deal in the space. We like NWL – technically looks strong, and it’s a conviction way to buy a positive view on the broader market.

Netwealth (NWL) Chart

BROKER MOVES

· ARB Cut to Hold at EL & C Baillieu; PT A$28.20

· Wesfarmers Raised to Outperform at Macquarie; PT A$51 **Resides in MM Income Portfolio**

· Aristocrat Cut to Neutral at Macquarie; PT A$31.50

· Secos Group Rated New Buy at Canaccord; PT 25 Australian cents

· Whitehaven Raised to Lighten at Ord Minnett; PT A$1

· Xero Raised to Outperform at RBC; PT A$120 **Resides in MM growth Portfolio**

· Downer EDI Raised to Overweight at Morgan Stanley; PT A$5.60 **Covered yesterday in the MM Income Note**

· Eagers Automotive Cut to Sell at Morningstar

· Costa Cut to Sell at Morningstar

· Sandfire Raised to Neutral at Goldman; PT A$4.80

· ARB Cut to Underweight at JPMorgan; PT A$24

· Altium Rated New Positive at Evans & Partners Pty Ltd

· Tyro Payments Rated New Neutral at Goldman; PT A$3.20

· Corporate Travel Raised to Outperform at RBC; PT A$19

· Fortescue Reinstated Market Perform at BMO; PT A$16

OUR CALLS

No changes today

Major Movers Today

Have a great night

James & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.