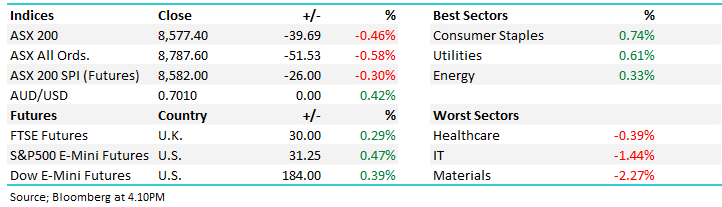

The ASX200 ended last week up +2.3%, with the first three days of October already recouping all of September's decline. The healthcare sector made a welcome return to the winners' enclosure, ably supported by the influential miners and banks, while the energy sector was the only meaningful drag on the index. Only a flat week by the heavyweight iron ore miners reined in performance, although their sector peers worked hard to address their slumber, with 18 members of the materials sector closing out the week up more than +5%.

The ASX200 snapped a 3 week losing streak up +0.2% although the broad market was soft with 8 of the main 11 sectors closing lower. However, a stellar +5.9% advance by the influential materials sector was enough to see the local bourse close higher, even as global indices experienced a rare dip for 2025. This recent sector rotation into the miners will be challenged early next week following a dip by BHP in the US on Friday night.

The ASX200 ended last week down 1% with only the rate-sensitive tech, consumer discretionary and utilities sectors taking some solace from the Fed's 0.25% rate cut. The energy sector stood out in the losers enclosure, dropping 4% after Abu Dhabi National Oil Co’s investment arm, XRG, walked away from its $36.4bn bid for Santos (STO). The market traded in another tight 150-point/1.7% range as the Fed rate cut failed to deliver any meaningful lead.

The ASX200 ended last week largely flat, holding September's current pullback to 1.2%. It may have been a quiet week on the index level, but it wasn’t on the sector level, with solid gains by the rate-sensitive tech, real estate, and utilities sectors while the energy sector fell 4.5% as OPEC+ maintained its elevated supply. It was disappointing to see the local index drift while US indices punched higher, although a number of majors trading ex-dividend did weigh locally. The heavyweight miners slipped slightly after mining giants Anglo American / Teck Resources agreed to merge, forming a ~$53 billion copper powerhouse.

The ASX200 was whacked 160-points on Wednesday after hotter-than-expected GDP figures tempered rate cut expectations, but by Friday’s close, the market had recovered over 80% of the fall. Nerves increased throughout the week into Friday night's pivotal US Job Report, but after the release, markets remained uncertain as Fed rate cuts looked a given following the weak numbers, but concerns started to percolate around the health of the US economy.

The ASX200 slipped 0.1% lower on Friday, but it still finished the week up +0.1%. As we’ve said a few times lately, it's feeling a touch tired above 9000. It was another week to remember from a reporting perspective, which dominated much of the movement on the sector level, although the materials sector continued to enjoy a strong recovery, topping the leader board for the week and month.

The ASX200 fell away on Friday to close down 0.6%, with the heavyweight miners and banks largely reversing early gains to close lower. The index still managed to end the week up +0.3%, but it failed to hold above the psychological 9000 level, with healthcare, and especially CSL, weighing heavily. The week, as expected, was dominated by the reporting season, with “misses” treated a touch more severely than beats were embraced. However, that’s no major surprise with the index posting all-time highs as often as it rains in Sydney!

A strong end to the week saw the ASX200 advance 1.5%, breaking to new all-time highs above 8,900. It was only a little over four months ago that the ASX was trading below 7,200, clouded by an aggressive tariff regime implemented by the president of the world’s largest economy. While the tariff situation remains a work in progress, with a deal yet to be signed between China and the US, it has quickly faded from headlines. Deals with other countries suggest the same will happen between the two superpowers, and our view at the time—that huge tariffs simply didn’t work as policy and therefore had to be a strategy—appears to be playing out.

The ASX200 slipped lower on Friday but still managed to snap a two-week losing streak. The index finished up +1.7% over the five days, driven by strong gains by miners and rate-sensitive names. On the sector level, only healthcare retreated courtesy of renewed tariff jitters while the Materials sector surged over 5% higher, led by gold, rare earth and lithium stocks. A more than 30c gain by BHP in the US on Friday nights suggests there's more in this move. The extent of the gains in miners saw a number of the best performers outperform IRESS (IRE), and it received a takeover bid!

The ASX200 slipped 0.1% last week after a tough Friday session, but it still ended up 2.3% for July. Earnings season is upon us, and it's already started to exert its force on the market - It's not often you see an ASX200 stock halve in the blink of an eye! We have begun the seasonally weak August-September period for the ASX, and on cue, the index has started to feel a touch soft, although 2-days doesn't make a summer.

The ASX200 snapped a 3 week losing streak up +0.2% although the broad market was soft with 8 of the main 11 sectors closing lower. However, a stellar +5.9% advance by the influential materials sector was enough to see the local bourse close higher, even as global indices experienced a rare dip for 2025. This recent sector rotation into the miners will be challenged early next week following a dip by BHP in the US on Friday night.

The ASX200 ended last week down 1% with only the rate-sensitive tech, consumer discretionary and utilities sectors taking some solace from the Fed's 0.25% rate cut. The energy sector stood out in the losers enclosure, dropping 4% after Abu Dhabi National Oil Co’s investment arm, XRG, walked away from its $36.4bn bid for Santos (STO). The market traded in another tight 150-point/1.7% range as the Fed rate cut failed to deliver any meaningful lead.

The ASX200 ended last week largely flat, holding September's current pullback to 1.2%. It may have been a quiet week on the index level, but it wasn’t on the sector level, with solid gains by the rate-sensitive tech, real estate, and utilities sectors while the energy sector fell 4.5% as OPEC+ maintained its elevated supply. It was disappointing to see the local index drift while US indices punched higher, although a number of majors trading ex-dividend did weigh locally. The heavyweight miners slipped slightly after mining giants Anglo American / Teck Resources agreed to merge, forming a ~$53 billion copper powerhouse.

The ASX200 was whacked 160-points on Wednesday after hotter-than-expected GDP figures tempered rate cut expectations, but by Friday’s close, the market had recovered over 80% of the fall. Nerves increased throughout the week into Friday night's pivotal US Job Report, but after the release, markets remained uncertain as Fed rate cuts looked a given following the weak numbers, but concerns started to percolate around the health of the US economy.

The ASX200 slipped 0.1% lower on Friday, but it still finished the week up +0.1%. As we’ve said a few times lately, it's feeling a touch tired above 9000. It was another week to remember from a reporting perspective, which dominated much of the movement on the sector level, although the materials sector continued to enjoy a strong recovery, topping the leader board for the week and month.

The ASX200 fell away on Friday to close down 0.6%, with the heavyweight miners and banks largely reversing early gains to close lower. The index still managed to end the week up +0.3%, but it failed to hold above the psychological 9000 level, with healthcare, and especially CSL, weighing heavily. The week, as expected, was dominated by the reporting season, with “misses” treated a touch more severely than beats were embraced. However, that’s no major surprise with the index posting all-time highs as often as it rains in Sydney!

A strong end to the week saw the ASX200 advance 1.5%, breaking to new all-time highs above 8,900. It was only a little over four months ago that the ASX was trading below 7,200, clouded by an aggressive tariff regime implemented by the president of the world’s largest economy. While the tariff situation remains a work in progress, with a deal yet to be signed between China and the US, it has quickly faded from headlines. Deals with other countries suggest the same will happen between the two superpowers, and our view at the time—that huge tariffs simply didn’t work as policy and therefore had to be a strategy—appears to be playing out.

The ASX200 slipped lower on Friday but still managed to snap a two-week losing streak. The index finished up +1.7% over the five days, driven by strong gains by miners and rate-sensitive names. On the sector level, only healthcare retreated courtesy of renewed tariff jitters while the Materials sector surged over 5% higher, led by gold, rare earth and lithium stocks. A more than 30c gain by BHP in the US on Friday nights suggests there's more in this move. The extent of the gains in miners saw a number of the best performers outperform IRESS (IRE), and it received a takeover bid!

The ASX200 slipped 0.1% last week after a tough Friday session, but it still ended up 2.3% for July. Earnings season is upon us, and it's already started to exert its force on the market - It's not often you see an ASX200 stock halve in the blink of an eye! We have begun the seasonally weak August-September period for the ASX, and on cue, the index has started to feel a touch soft, although 2-days doesn't make a summer.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.