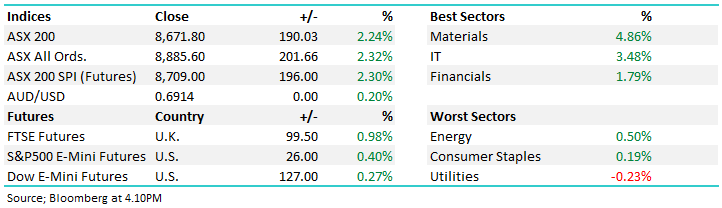

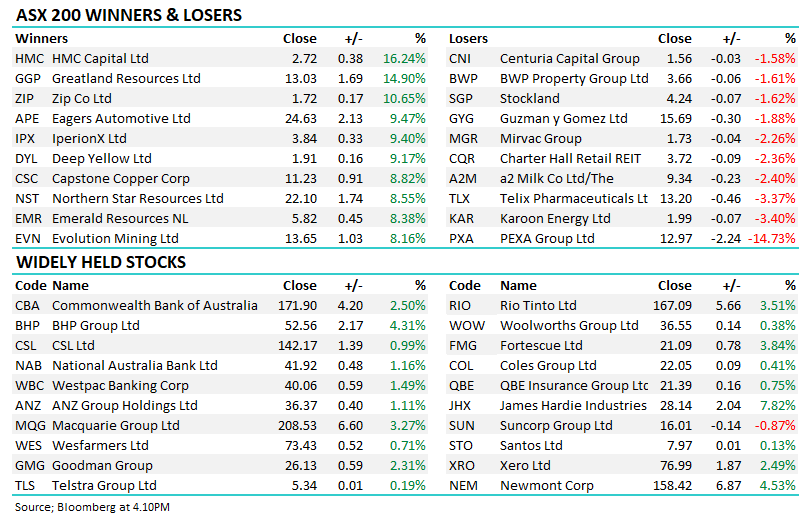

A bullish start to the trading week with the risk-on sectors doing best following a stellar session on Wall Street all the way back on Friday night. Lots of analysis out this morning as brokers re-cut their numbers following a flow of trading updates last week (a result of MQG conference), with a lot of news flow stemming from some of the more interesting sectors – namely Lithium & Rare-Earths – more on these sectors in the AM report.

A positive session to end a tough week for the market with some confidence stemming from solid results out of ANZ & Macquarie (MQG) despite the latter ending lower on the day. For the week, the ASX 200 lost 1.22% with the financials the biggest headwind, while it was pleasing to see a bounce back in the property sector despite the increase in rates – a sign that the market believes rates have hit their peak!

The market opened sharply lower this morning before a spirited ~50pt fightback that saw 75% of the main board actually finish up on the day. Banks dominated following a weaker than expected 1H23 result from NAB which threw the cat amongst the pigeons, weakness in the big 4 taking 44pts off the ASX200 ahead of ANZ & Macquarie (MQG) reporting tomorrow, while Westpac (WBC) is out on Monday.

A tough day at the office with the ASX now down ~150pts/2% since Philip Lowe et al surprised the majority (Chris Joye will say we’re all idiots!) and raised rates by 25bps, a move which is likely to be reflected in the US tonight as their Central Bank steps up to the plate. However, it wasn’t all one-way traffic today with a spirited fight back (+40pts) from mid-afternoon lows, as the ‘buy the dip’ mentality emerged. Gold stocks a stand out while some select industrials also went against the grain, encouragingly 20% of the main board actually closed higher.

A fairly subdued morning before RBA Governor Dr Philip Lowe stepped up to the plate and surprisingly raised interest rates when the vast majority thought they would remain on hold. That sent the AUD sharply higher, bond (prices) & equities sharply lower which materially pushed up yields.

A positive start to the week and month for the ASX, though the local index finished a long way from early session highs today as investors position themselves ahead of the RBA rate decision due out tomorrow morning. Tech was the main laggard which was particularly disappointing given the strength seen in the Nasdaq in recent sessions. The Materials sector was also lacklustre, struggling for direction with most Asian markets closed for Golden Week.

A solid end to a positive month for the ASX with 60% of the market finishing higher, although there were some fireworks happening under the hood with Megaport (MP1) up ~40% on better guidance. For the month, the ASX 200 put on +1.83% and it was the sectors that benefit from lower interest rates that saw the best of it, namely Property & IT while the Material’s were the only group to end April in the red.

The ASX fell again today, now down 5 consecutive sessions with Banks & Healthcare stocks contributing most of the pain at the index level. Concern stemming from the US financial system is headlining the media, however, in MM’s view, it has simply been a case of a tired market approaching a seasonally weak period and it made sense to take some cream off the top after a solid run for stocks.

A choppy session for the ASX today with a lot of company news met with key economic data. A weaker open, although better results from key US companies aftermarket saw US Futures rally which provided some support to local stocks, before the recovery really got underway post the inflation data at 11.30 am where the RBA’s preferred measure of prices came in a touch below expectations, and this reduces the chance of another hike in May.

A quiet session as you’d expect with all the smart people taking Monday off to lock in a 4-day break ahead of ANZAC day tomorrow….The ASX opened lower and remained in a holding pattern, although there were a few moves on the stock level that caught our eye.

A positive session to end a tough week for the market with some confidence stemming from solid results out of ANZ & Macquarie (MQG) despite the latter ending lower on the day. For the week, the ASX 200 lost 1.22% with the financials the biggest headwind, while it was pleasing to see a bounce back in the property sector despite the increase in rates – a sign that the market believes rates have hit their peak!

The market opened sharply lower this morning before a spirited ~50pt fightback that saw 75% of the main board actually finish up on the day. Banks dominated following a weaker than expected 1H23 result from NAB which threw the cat amongst the pigeons, weakness in the big 4 taking 44pts off the ASX200 ahead of ANZ & Macquarie (MQG) reporting tomorrow, while Westpac (WBC) is out on Monday.

A tough day at the office with the ASX now down ~150pts/2% since Philip Lowe et al surprised the majority (Chris Joye will say we’re all idiots!) and raised rates by 25bps, a move which is likely to be reflected in the US tonight as their Central Bank steps up to the plate. However, it wasn’t all one-way traffic today with a spirited fight back (+40pts) from mid-afternoon lows, as the ‘buy the dip’ mentality emerged. Gold stocks a stand out while some select industrials also went against the grain, encouragingly 20% of the main board actually closed higher.

A fairly subdued morning before RBA Governor Dr Philip Lowe stepped up to the plate and surprisingly raised interest rates when the vast majority thought they would remain on hold. That sent the AUD sharply higher, bond (prices) & equities sharply lower which materially pushed up yields.

A positive start to the week and month for the ASX, though the local index finished a long way from early session highs today as investors position themselves ahead of the RBA rate decision due out tomorrow morning. Tech was the main laggard which was particularly disappointing given the strength seen in the Nasdaq in recent sessions. The Materials sector was also lacklustre, struggling for direction with most Asian markets closed for Golden Week.

A solid end to a positive month for the ASX with 60% of the market finishing higher, although there were some fireworks happening under the hood with Megaport (MP1) up ~40% on better guidance. For the month, the ASX 200 put on +1.83% and it was the sectors that benefit from lower interest rates that saw the best of it, namely Property & IT while the Material’s were the only group to end April in the red.

The ASX fell again today, now down 5 consecutive sessions with Banks & Healthcare stocks contributing most of the pain at the index level. Concern stemming from the US financial system is headlining the media, however, in MM’s view, it has simply been a case of a tired market approaching a seasonally weak period and it made sense to take some cream off the top after a solid run for stocks.

A choppy session for the ASX today with a lot of company news met with key economic data. A weaker open, although better results from key US companies aftermarket saw US Futures rally which provided some support to local stocks, before the recovery really got underway post the inflation data at 11.30 am where the RBA’s preferred measure of prices came in a touch below expectations, and this reduces the chance of another hike in May.

A quiet session as you’d expect with all the smart people taking Monday off to lock in a 4-day break ahead of ANZAC day tomorrow….The ASX opened lower and remained in a holding pattern, although there were a few moves on the stock level that caught our eye.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.