A softer start to the week with banks weighing on the broader index while strength in the IT sector overseas continued to support our local tech stocks, Xero (XRO) a standout again while WiseTech (WTC) continued its march higher.

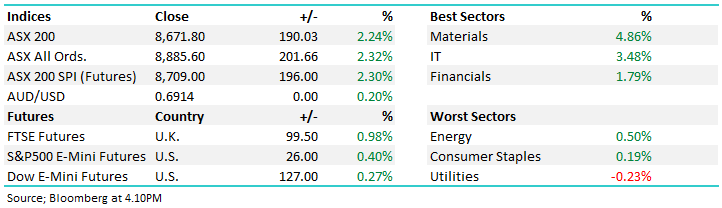

The easing of rhetoric around the US Debt Ceiling seems to have lifted markets again today with a broad rally for local shares carrying the index higher into the weekend. 70% of the local bourse closed higher with the Tech sector seeing the best of it for the second day in a row. Financials were the main support for the index while Utilities and Materials were the only sector to close lower. The index added 22pts/+0.31% this week for its second consecutive weekly gain.

A solid session for the ASX today, particularly in some areas as good results from Xero (XRO) and a ‘less bad; update from Nufarm (NUF) curated some broader optimism. Tech led the gains today, the local market enjoyed a risk-on shift thanks to improved rhetoric around the US debt ceiling discussions.

Another weaker session for local stocks today however ‘buyers of the dip’ saw the local market recover over half of its early losses as it tracked a bounce by US futures, influential names such as BHP and Com Bank (CBA) closed well off their respective lows with the banks in particular catching our attention with ANZ closing positive on the day, while the IT sector followed US counterparts higher.

A soft day for stocks with a barrage of economic data that implied the RBA may still raise rates again – which was enough to upset the apple cart. It was interesting to see the more defensive sectors feel most of the selling with 75% of the top 200 finishing under water, while the materials and energy stocks which are more heavily linked to Chinese growth were outperformers…

A solid (~30pt) fightback from early weakness (again) today pushing the ASX 200 into the black by the close. Some corporate activity plus some buying in the recently weak materials & energy stocks supported by an ongoing recovery amongst the REITs offset the drag from the financials with ANZ & MQG trading ex-dividend.

With so much negative rhetoric doing the rounds, the market has remained incredibly resilient and today was no different. Commodities were hit overnight on growing recessionary fears, however by the close, early weakness was bought into and the ASX200 finished higher on the day with 65% of stocks closing in the green despite BHP taking ~8 index points from the broader market.

Solid earnings and a bump of corporate activity was not enough to push the market higher today, weakness amongst the mining stocks (ex-Lithium) to blame while Westpac (WBC) trading ex-dividend didn’t help. That said, another example of intra-day weakness being bought, more stocks than not actually trading higher while the index experiences a slow, shallow & begrudging pullback.

Another day of intra-session buying on the ASX which battled back from early session lows to close marginally down. The headline index move was largely a result of ex-dividends from NAB and BOQ, NAB’s dividend alone is worth ~10pts to the index. There was a pretty muted reaction to last night’s Federal Budget with no clear winners from a sector point of view, though Healthcare was probably the main beneficiary from the markets perspective.

A reasonable session after a weaker open this afternoon saw the broader market grind higher throughout the day. Some interesting company news out, with CBA providing a solid quarterly to round out bank reporting while Worley (WOR) held a strategy day where they outlaid the huge opportunity in front of them with the energy transition, and importantly, focussed on how they would grow margins.

The easing of rhetoric around the US Debt Ceiling seems to have lifted markets again today with a broad rally for local shares carrying the index higher into the weekend. 70% of the local bourse closed higher with the Tech sector seeing the best of it for the second day in a row. Financials were the main support for the index while Utilities and Materials were the only sector to close lower. The index added 22pts/+0.31% this week for its second consecutive weekly gain.

A solid session for the ASX today, particularly in some areas as good results from Xero (XRO) and a ‘less bad; update from Nufarm (NUF) curated some broader optimism. Tech led the gains today, the local market enjoyed a risk-on shift thanks to improved rhetoric around the US debt ceiling discussions.

Another weaker session for local stocks today however ‘buyers of the dip’ saw the local market recover over half of its early losses as it tracked a bounce by US futures, influential names such as BHP and Com Bank (CBA) closed well off their respective lows with the banks in particular catching our attention with ANZ closing positive on the day, while the IT sector followed US counterparts higher.

A soft day for stocks with a barrage of economic data that implied the RBA may still raise rates again – which was enough to upset the apple cart. It was interesting to see the more defensive sectors feel most of the selling with 75% of the top 200 finishing under water, while the materials and energy stocks which are more heavily linked to Chinese growth were outperformers…

A solid (~30pt) fightback from early weakness (again) today pushing the ASX 200 into the black by the close. Some corporate activity plus some buying in the recently weak materials & energy stocks supported by an ongoing recovery amongst the REITs offset the drag from the financials with ANZ & MQG trading ex-dividend.

With so much negative rhetoric doing the rounds, the market has remained incredibly resilient and today was no different. Commodities were hit overnight on growing recessionary fears, however by the close, early weakness was bought into and the ASX200 finished higher on the day with 65% of stocks closing in the green despite BHP taking ~8 index points from the broader market.

Solid earnings and a bump of corporate activity was not enough to push the market higher today, weakness amongst the mining stocks (ex-Lithium) to blame while Westpac (WBC) trading ex-dividend didn’t help. That said, another example of intra-day weakness being bought, more stocks than not actually trading higher while the index experiences a slow, shallow & begrudging pullback.

Another day of intra-session buying on the ASX which battled back from early session lows to close marginally down. The headline index move was largely a result of ex-dividends from NAB and BOQ, NAB’s dividend alone is worth ~10pts to the index. There was a pretty muted reaction to last night’s Federal Budget with no clear winners from a sector point of view, though Healthcare was probably the main beneficiary from the markets perspective.

A reasonable session after a weaker open this afternoon saw the broader market grind higher throughout the day. Some interesting company news out, with CBA providing a solid quarterly to round out bank reporting while Worley (WOR) held a strategy day where they outlaid the huge opportunity in front of them with the energy transition, and importantly, focussed on how they would grow margins.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.