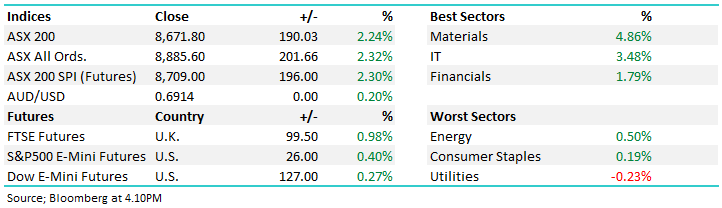

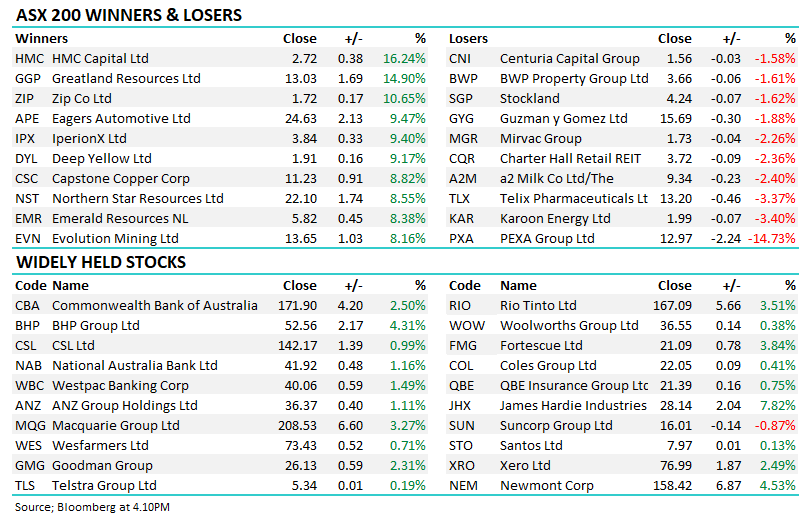

A strong start to the week with the ASX holding onto the majority of the gains that were flagged by futures markets this morning. The recently depressed Consumer Discretionary & Materials sectors bounced back while Technology gave back some recent outperformance.

The ASX had a good crack at closing higher on the week today after a very volatile 5 sessions, only just falling short of the milestone in the end. Materials were helped by stronger commodity prices and a softer USD, both reversing moves from earlier in the week with a relief rally for global growth leverage following the US Debt ceiling vote.

A pretty quiet day on the news flow front with the market drifting higher to recover some of yesterday’s freefall. The early session sugar hit came from the US lower house passing the debt ceiling relief bill but aside from that there was little to move markets for the first session of the new month. Tech continued its rally while Healthcare was the star performer of the sectors.

Overseas markets underperformed overnight which weighed on the open here locally. Resources were particularly on the back foot with strength in the USD putting pressure on materials while coal also fell to 2-year lows to hold energy stocks back. The rest of the market followed suit, particularly following a higher-than-expected CPI print at 11.30 am, up 6.8% in April vs the 6.4% expected. A very weak close resigned the ASX200 to its worst day since March.

It was a pretty muted session from the index point of view today with very little to drive markets following the US observing Memorial Day today. Real Estate gave back much of yesterday’s outperformance, followed by weakness in coal stocks weighing on the Energy sector. Banks were also marginally lower today, partly offset by strength in Telcos.

The local market was on the front foot early, jumping almost exactly +100pts/+1.4% on the open today following a tentative deal on the US debt ceiling. The ASX followed a positive move from the US on Friday night with US Futures adding to gains during trade this morning, however, the rally was sold into with the S&P500 Futures currently trading ~0.5% from the session highs. Tech in particular finished well of intraday highs after some profit-taking kicked in.

A quiet end to a busy week for markets with competing factors creating some big divergence across sectors. For the week, the ASX 200 fell by -1.68% while the Small Cap Index was off by -2.86% - smalls still can’t take a trick! These moves however underplay the variance across sectors with IT up +4.7% contrasted by the Materials sector which fell 3.45%.

A tough day for stocks with the heavy-weight sectors of Financials & Materials causing most of the pain. Despite the index finishing down ~1%, only 65% of stocks actually closed lower with the technology sector enjoying a phenomenal update from global chipmaker Nvidia (NVDA US) after the US close this morning – a stock we discussed this week here. That pushed Nasdaq Futures up +1.5% underpinning a 2.4% move higher from the Aussie tech sector.

The ASX opened lower to start the day and there was little in the way of buying support for the rest of the session as the index rolled off another ~25pts intra-day. Materials were the main drag on performance with iron ore continuing its slide while Tech was also soft as it gave back some of the recent outperformance with growth concerns weighing on sentiment. Energy went against the grain ahead of the next OPEC meeting, one of only three sectors to trade noticeably higher today.

Some optimism seen early with positive talk around the US debt ceiling negotiations but that seemed to evaporate, with the ASX following Asian markets down the gurgler by the close. Financials & property were solid, but anything linked to the consumer was soft.

The ASX had a good crack at closing higher on the week today after a very volatile 5 sessions, only just falling short of the milestone in the end. Materials were helped by stronger commodity prices and a softer USD, both reversing moves from earlier in the week with a relief rally for global growth leverage following the US Debt ceiling vote.

A pretty quiet day on the news flow front with the market drifting higher to recover some of yesterday’s freefall. The early session sugar hit came from the US lower house passing the debt ceiling relief bill but aside from that there was little to move markets for the first session of the new month. Tech continued its rally while Healthcare was the star performer of the sectors.

Overseas markets underperformed overnight which weighed on the open here locally. Resources were particularly on the back foot with strength in the USD putting pressure on materials while coal also fell to 2-year lows to hold energy stocks back. The rest of the market followed suit, particularly following a higher-than-expected CPI print at 11.30 am, up 6.8% in April vs the 6.4% expected. A very weak close resigned the ASX200 to its worst day since March.

It was a pretty muted session from the index point of view today with very little to drive markets following the US observing Memorial Day today. Real Estate gave back much of yesterday’s outperformance, followed by weakness in coal stocks weighing on the Energy sector. Banks were also marginally lower today, partly offset by strength in Telcos.

The local market was on the front foot early, jumping almost exactly +100pts/+1.4% on the open today following a tentative deal on the US debt ceiling. The ASX followed a positive move from the US on Friday night with US Futures adding to gains during trade this morning, however, the rally was sold into with the S&P500 Futures currently trading ~0.5% from the session highs. Tech in particular finished well of intraday highs after some profit-taking kicked in.

A quiet end to a busy week for markets with competing factors creating some big divergence across sectors. For the week, the ASX 200 fell by -1.68% while the Small Cap Index was off by -2.86% - smalls still can’t take a trick! These moves however underplay the variance across sectors with IT up +4.7% contrasted by the Materials sector which fell 3.45%.

A tough day for stocks with the heavy-weight sectors of Financials & Materials causing most of the pain. Despite the index finishing down ~1%, only 65% of stocks actually closed lower with the technology sector enjoying a phenomenal update from global chipmaker Nvidia (NVDA US) after the US close this morning – a stock we discussed this week here. That pushed Nasdaq Futures up +1.5% underpinning a 2.4% move higher from the Aussie tech sector.

The ASX opened lower to start the day and there was little in the way of buying support for the rest of the session as the index rolled off another ~25pts intra-day. Materials were the main drag on performance with iron ore continuing its slide while Tech was also soft as it gave back some of the recent outperformance with growth concerns weighing on sentiment. Energy went against the grain ahead of the next OPEC meeting, one of only three sectors to trade noticeably higher today.

Some optimism seen early with positive talk around the US debt ceiling negotiations but that seemed to evaporate, with the ASX following Asian markets down the gurgler by the close. Financials & property were solid, but anything linked to the consumer was soft.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.