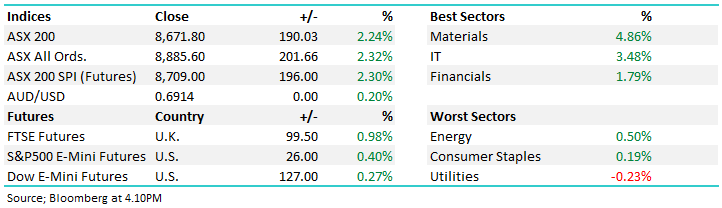

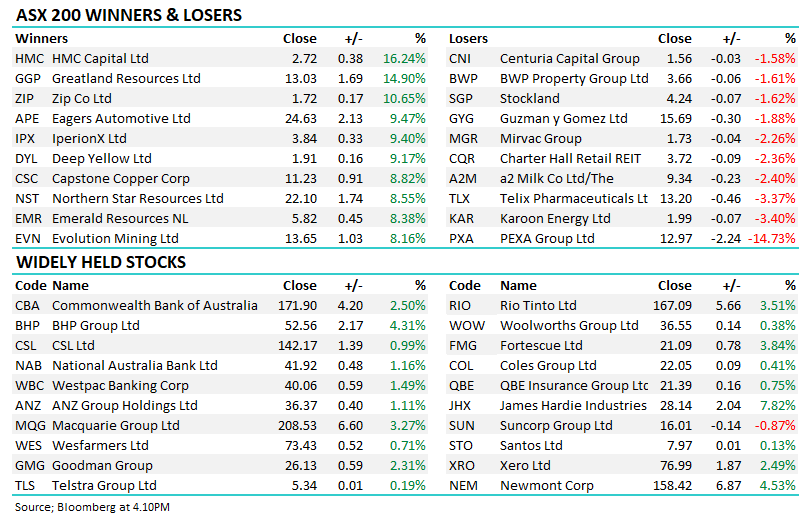

A surprisingly positive session for the ASX today, courtesy of the RBA minutes that showed a July 0.25% rate hike in perhaps, not a fait accompli, with the RBA still more data dependent than the market had given it credit for. Bond yields fell after the 11.30 am release, and so too did the Australian dollar and that put a bid tone under the market which built on its impressive 6-day advance now totalling ~220pts/3%, chalking up a 7-week high in the process

A rebound in the Banks and Healthcare stocks underpinned a solid start to the week with the ASX treading its own path today ahead of a public holiday (no trade) in the US tonight. Resources have been on fire so far this month, with the Material Index +7% in June to date, however, we wouldn’t be surprised to see some performance reversion in the short term, particularly if the $US finds some support – that was certainly the case today.

The ASX finished the shortened week on the front foot today with healthcare being the only sector to fall on Friday’s session. The index strength came on the back of gains in energy and materials as commodities caught a bid largely thanks to growing confidence in stimulus in China. Coal stocks were a notable winner in the session, continuing the rally seen this month with Newcastle Coal futures trading more than 3.5% higher today.

The ASX ticked up to the highest level in more than a week on the back of strength in both mining and financials stocks early on. The advance was halted by stronger-than-expected employment data with the Australian economy adding 76k jobs in May and the unemployment rate falling to 3.6% - the strong data lifting expectations of another, if not two more hikes by the RBA in the next few months. The index gave back all the early gains to trade marginally lower around midday, though buyers returned into the afternoon to help eke out a small gain. Healthcare was again the laggard while Tech continues to show strength.

Commodity stocks were the place to be today enjoying the more bullish rhetoric coming from China, the sector underpinning a solid move higher at the index level and more than offsetting a softer-than-expected update from heavyweight CSL.

A positive session to kick off the shortened week which will be dominated by key US economic data. CPI Inflation tonight in the US is expected to be benign, up just 0.1% MoM and 4.1% YoY, down from 4.9%. This should mean the Federal Reserve holds rates at 5-5.25% on Thursday, although the market has largely priced in another 0.25% increase in July.

A solid end to a choppy week for the ASX that was dominated by another 25bps rate hike by the RBA. Sector rotation remains a constant with the first cracks appearing in the recent tech rally while the resource stocks found their feet and edged higher, inline with our recent commentary that tech was vulnerable and we should continue our patient transition towards commodity stocks.

A choppy and ultimately negative day for the ASX where buying in Energy & Materials was more than offset by a sharp pullback in Tech, although weakness was obvious right across the sectors negatively influenced by higher interest rates.

The local bourse was on the front foot initially, rallying ~0.5% early in the session before caution returned, seemingly the market has lost its mojo after the RBAs hike, failing to hold on to gains. The end result from the index perspective was a small fall as the ASX200 closed on the intraday lows, but there was significant volatility on the sector front.

The local market was on the back foot for most of the session today thanks to softer US markets overnight before yet another hike by the RBA resigned shares to a drop of more than 1%. The latest hike takes Australian interest rates to an 11-year high while Governor Lowe’s commentary seems to suggest he’s not done yet. Discretionary stocks took a hit as a result with a downgrade in the sector not helping the already negative market view of the space being squeezed by tighter household budgets.

A rebound in the Banks and Healthcare stocks underpinned a solid start to the week with the ASX treading its own path today ahead of a public holiday (no trade) in the US tonight. Resources have been on fire so far this month, with the Material Index +7% in June to date, however, we wouldn’t be surprised to see some performance reversion in the short term, particularly if the $US finds some support – that was certainly the case today.

The ASX finished the shortened week on the front foot today with healthcare being the only sector to fall on Friday’s session. The index strength came on the back of gains in energy and materials as commodities caught a bid largely thanks to growing confidence in stimulus in China. Coal stocks were a notable winner in the session, continuing the rally seen this month with Newcastle Coal futures trading more than 3.5% higher today.

The ASX ticked up to the highest level in more than a week on the back of strength in both mining and financials stocks early on. The advance was halted by stronger-than-expected employment data with the Australian economy adding 76k jobs in May and the unemployment rate falling to 3.6% - the strong data lifting expectations of another, if not two more hikes by the RBA in the next few months. The index gave back all the early gains to trade marginally lower around midday, though buyers returned into the afternoon to help eke out a small gain. Healthcare was again the laggard while Tech continues to show strength.

Commodity stocks were the place to be today enjoying the more bullish rhetoric coming from China, the sector underpinning a solid move higher at the index level and more than offsetting a softer-than-expected update from heavyweight CSL.

A positive session to kick off the shortened week which will be dominated by key US economic data. CPI Inflation tonight in the US is expected to be benign, up just 0.1% MoM and 4.1% YoY, down from 4.9%. This should mean the Federal Reserve holds rates at 5-5.25% on Thursday, although the market has largely priced in another 0.25% increase in July.

A solid end to a choppy week for the ASX that was dominated by another 25bps rate hike by the RBA. Sector rotation remains a constant with the first cracks appearing in the recent tech rally while the resource stocks found their feet and edged higher, inline with our recent commentary that tech was vulnerable and we should continue our patient transition towards commodity stocks.

A choppy and ultimately negative day for the ASX where buying in Energy & Materials was more than offset by a sharp pullback in Tech, although weakness was obvious right across the sectors negatively influenced by higher interest rates.

The local bourse was on the front foot initially, rallying ~0.5% early in the session before caution returned, seemingly the market has lost its mojo after the RBAs hike, failing to hold on to gains. The end result from the index perspective was a small fall as the ASX200 closed on the intraday lows, but there was significant volatility on the sector front.

The local market was on the back foot for most of the session today thanks to softer US markets overnight before yet another hike by the RBA resigned shares to a drop of more than 1%. The latest hike takes Australian interest rates to an 11-year high while Governor Lowe’s commentary seems to suggest he’s not done yet. Discretionary stocks took a hit as a result with a downgrade in the sector not helping the already negative market view of the space being squeezed by tighter household budgets.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.