A positive open for stocks before the index tracked lower ahead of the RBA decision on interest rates at 2.30 pm - no change to rates - the market rallied, particularly the financials and property stocks buoyed by some respite to cost of living pressures. About half of the professional forecasters had expected a hike, while interest rate futures were pricing a ~20% probability of a 0.25% move.

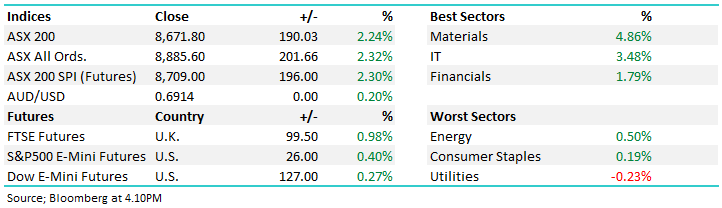

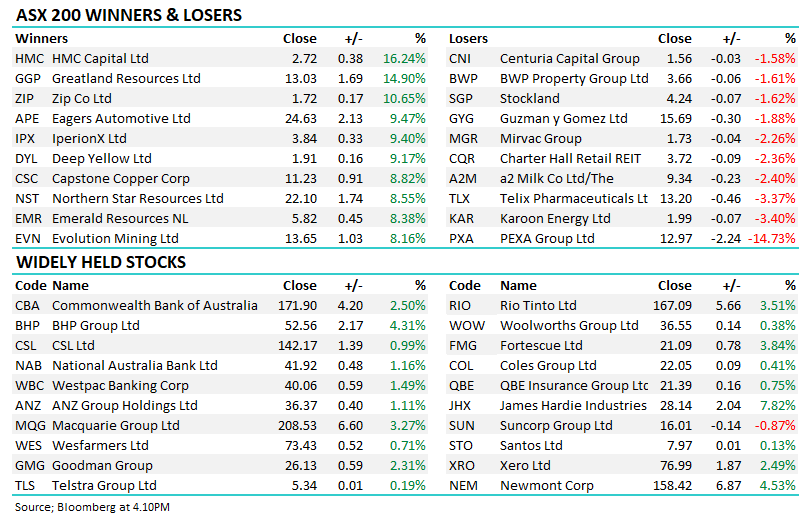

The first session of FY24 was a positive one for local stocks with the market grinding consistently higher throughout the day to close on session highs. There seemed to be an overarching trend today that saw some of the ‘FY23 dogs’ attract buying with the discretionary retailers the most obvious example at a sector level – perhaps confidence is growing around a ‘soft landing’ as inflation cools and central banks look to a least pause on rates.

A quiet session to wrap up FY23, a year where central banks have hiked interest rates at an unprecedented speed taking them to fresh 11-year highs, the US experienced a Banking Crisis, China’s economy was buffeted from aggressive COVID lockdowns and war was waged on Ukraine, to name just a few of the headwinds for equities. The fact the market in price terms has risen more than 10% is just another example of why we, as investors, need to keep an open mind and not let investment decisions be impacted by the barrage of negativity that dominates mainstream press.

While the ASX ended flat today, most of the early gains were surrendered from 11 am onwards as divergence opened up across sectors, Utilities were weak, offset by solid gains by IT stocks that keyed off a good session in the US overnig

Shares opened higher this morning, but the real rally came following the 11.30 am print on inflation which was significantly lower than expected prompting investors to reduce bets on rate hikes - it now seems like the RBA’s aggressive move to tighten policy at an unprecedented rate is showing signs of working, boosting equities today. Most sectors finished more than 1% higher, and only one sector closed lower, but only marginally so.

Some respite from the recent selling today with the market snapping a ~300pt/ 4.1% pullback for the ASX 200 over just 4 trading days, as buying amongst the influential miners and the under-pressure property stocks drove the index higher, 3 days before we rule the books off on FY23. As we wrote this morning, the Australian bourse is up ~8% before dividends, a healthy result if we consider both the economic backdrop and geo-political headwinds in play.

The bearish tone on the market continued today with any intra-day rallies being met with selling, though the ASX200 didn’t seem to want to travel too far south of 7100 at the same time either, finishing with a small jump on the close. No sector was down more than 1% today, though 4 sectors closed -0.5% or worse with Utilities the biggest drop but Financials weighing on the index the most.

The third consecutive session of pain for the local market, however, today’s move was felt across the region with Asian markets feeling the pinch. The index was down by more than 100pts late in the day before ticking up slightly on the close, though it wasn’t enough to stop the week from finishing at a new low for the last fortnight. Energy was a clear detractor to performance despite some weaker supply numbers out of the US tonight, instead, energy traders were focused on a slowing global economy while a surprise 50bps hike from the Bank of England overnight didn’t help with confidence.

A dose of reality today with some broad-based selling right across the market, as aggressive selling knocked the ASX back from seven-week highs, the recently hot IT sector in the cross-hairs however over 90% of the market finished in the red. Asian markets were down as well, but not by as much while US Futures remained resilient, only trading marginally lower.

The market snapped its seven-day winning streak today with ~60% of the market closing lower, led by weakness in the Energy stocks which succumb to Crude Oil’s decline overnight, while the consumer discretionary sector was hit by a downgrade from UBS. The afternoon session saw the most action as the market slid sharply lower into the close chalking up a bearish close.

The first session of FY24 was a positive one for local stocks with the market grinding consistently higher throughout the day to close on session highs. There seemed to be an overarching trend today that saw some of the ‘FY23 dogs’ attract buying with the discretionary retailers the most obvious example at a sector level – perhaps confidence is growing around a ‘soft landing’ as inflation cools and central banks look to a least pause on rates.

A quiet session to wrap up FY23, a year where central banks have hiked interest rates at an unprecedented speed taking them to fresh 11-year highs, the US experienced a Banking Crisis, China’s economy was buffeted from aggressive COVID lockdowns and war was waged on Ukraine, to name just a few of the headwinds for equities. The fact the market in price terms has risen more than 10% is just another example of why we, as investors, need to keep an open mind and not let investment decisions be impacted by the barrage of negativity that dominates mainstream press.

While the ASX ended flat today, most of the early gains were surrendered from 11 am onwards as divergence opened up across sectors, Utilities were weak, offset by solid gains by IT stocks that keyed off a good session in the US overnig

Shares opened higher this morning, but the real rally came following the 11.30 am print on inflation which was significantly lower than expected prompting investors to reduce bets on rate hikes - it now seems like the RBA’s aggressive move to tighten policy at an unprecedented rate is showing signs of working, boosting equities today. Most sectors finished more than 1% higher, and only one sector closed lower, but only marginally so.

Some respite from the recent selling today with the market snapping a ~300pt/ 4.1% pullback for the ASX 200 over just 4 trading days, as buying amongst the influential miners and the under-pressure property stocks drove the index higher, 3 days before we rule the books off on FY23. As we wrote this morning, the Australian bourse is up ~8% before dividends, a healthy result if we consider both the economic backdrop and geo-political headwinds in play.

The bearish tone on the market continued today with any intra-day rallies being met with selling, though the ASX200 didn’t seem to want to travel too far south of 7100 at the same time either, finishing with a small jump on the close. No sector was down more than 1% today, though 4 sectors closed -0.5% or worse with Utilities the biggest drop but Financials weighing on the index the most.

The third consecutive session of pain for the local market, however, today’s move was felt across the region with Asian markets feeling the pinch. The index was down by more than 100pts late in the day before ticking up slightly on the close, though it wasn’t enough to stop the week from finishing at a new low for the last fortnight. Energy was a clear detractor to performance despite some weaker supply numbers out of the US tonight, instead, energy traders were focused on a slowing global economy while a surprise 50bps hike from the Bank of England overnight didn’t help with confidence.

A dose of reality today with some broad-based selling right across the market, as aggressive selling knocked the ASX back from seven-week highs, the recently hot IT sector in the cross-hairs however over 90% of the market finished in the red. Asian markets were down as well, but not by as much while US Futures remained resilient, only trading marginally lower.

The market snapped its seven-day winning streak today with ~60% of the market closing lower, led by weakness in the Energy stocks which succumb to Crude Oil’s decline overnight, while the consumer discretionary sector was hit by a downgrade from UBS. The afternoon session saw the most action as the market slid sharply lower into the close chalking up a bearish close.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.