A steady flow of corporate news across the ticker today to keep things interesting while the RBA minutes released at 11.30 am prompted a sharp sell-off before a grinding recovery ensued – the index closing only marginally lower.

A tentative start to the trading week from an index perspective, although there were a few landmines at the stock level, signs of what could be ahead as we approach FY23 results season perhaps.

A weaker USD and a drop in local bond yields helped push the ASX to a 3-week high, crossing back above 7300 for the first time this financial year. Aussie 2-year bond yields fell back below 4% today for the first time in more than a month, supporting the risk-on attitude. Similar to the US market, tech was a standout today and led the sector performance for the week.

Inflation, at least in the US, is quickly coming under control leading to a strong rally on the local market today. The broad-based rally saw more than 90% of the ASX200 close higher today, led by a strong rally in Real Estate on a day when all sectors closed up. China trade data also printed today with both imports and exports falling more than expected with a lower trade surplus adding to the view that China will ramp up its stimulus efforts.

Resilience was shown on the ASX again today, continuing the relief rally that kicked off yesterday. Commodity-linked stocks were once again the main focus with follow-through buying on the back of China’s support of their property sector. Energy was the key standout though thanks to signs that Russian production had started to slow and comments from the Saudis supporting the OPEC+ actions to stabilize oil markets. In a shift away from recent history, tech was the laggard on the local market today. All eyes will be on the US Inflation data due out at 10.30 pm tonight.

Strong resilience was shown on the local market starting on the front foot today but highlighted by consistent intra-day buying, grinding higher throughout the session to put on more than 100 points. Just 7% of the index closed lower with all sectors adding more than 0.5%. Just like the US market overnight, the small-cap index (S&P Small Ords) outperformed with a 2.14% jump today.

The ASX saw the best of it early on Monday morning, initially rallying ~0.6%, looking to recover some of last week’s losses. Banks, miners and energy sectors supported the index before traders faded the strength throughout the rest of the session. The ASX200 settled at its lowest close since late March with the only shining light being the Tech sector.

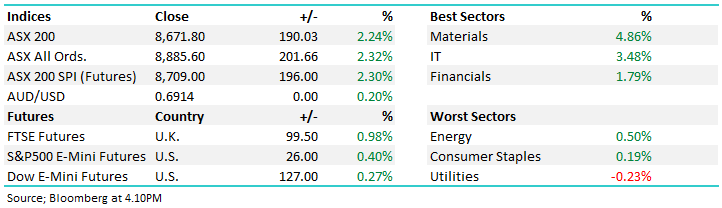

The local market fell to levels not seen in 3 months today on the back of a swift turn higher in bond yields The local 10-year yield was up 15bps/~3.5% early on in the session, settling at 4.255% driving a shift away from risky assets. There was little appetite to add exposure on a Friday either, resigning the market to a ~200pt drop over the last 3 sessions. All sectors closed lower while the ASX200 closed down 2.24% for the week.

A tough day for the Aussie market with broad-based selling knocking shares sharply low – the higher beta parts of the market felt the brunt of the risk-off attitude while the IT stocks were the only ones to finish up on the day - WiseTech (WT) +0.98% only knows one way!

A weaker session for the ASX, and with no lead from the US we were left to key off marginally softer European markets while Asian stocks also tracked lower during our time zone. Banks lost some of yesterday’s gains while property stocks also fell.

A tentative start to the trading week from an index perspective, although there were a few landmines at the stock level, signs of what could be ahead as we approach FY23 results season perhaps.

A weaker USD and a drop in local bond yields helped push the ASX to a 3-week high, crossing back above 7300 for the first time this financial year. Aussie 2-year bond yields fell back below 4% today for the first time in more than a month, supporting the risk-on attitude. Similar to the US market, tech was a standout today and led the sector performance for the week.

Inflation, at least in the US, is quickly coming under control leading to a strong rally on the local market today. The broad-based rally saw more than 90% of the ASX200 close higher today, led by a strong rally in Real Estate on a day when all sectors closed up. China trade data also printed today with both imports and exports falling more than expected with a lower trade surplus adding to the view that China will ramp up its stimulus efforts.

Resilience was shown on the ASX again today, continuing the relief rally that kicked off yesterday. Commodity-linked stocks were once again the main focus with follow-through buying on the back of China’s support of their property sector. Energy was the key standout though thanks to signs that Russian production had started to slow and comments from the Saudis supporting the OPEC+ actions to stabilize oil markets. In a shift away from recent history, tech was the laggard on the local market today. All eyes will be on the US Inflation data due out at 10.30 pm tonight.

Strong resilience was shown on the local market starting on the front foot today but highlighted by consistent intra-day buying, grinding higher throughout the session to put on more than 100 points. Just 7% of the index closed lower with all sectors adding more than 0.5%. Just like the US market overnight, the small-cap index (S&P Small Ords) outperformed with a 2.14% jump today.

The ASX saw the best of it early on Monday morning, initially rallying ~0.6%, looking to recover some of last week’s losses. Banks, miners and energy sectors supported the index before traders faded the strength throughout the rest of the session. The ASX200 settled at its lowest close since late March with the only shining light being the Tech sector.

The local market fell to levels not seen in 3 months today on the back of a swift turn higher in bond yields The local 10-year yield was up 15bps/~3.5% early on in the session, settling at 4.255% driving a shift away from risky assets. There was little appetite to add exposure on a Friday either, resigning the market to a ~200pt drop over the last 3 sessions. All sectors closed lower while the ASX200 closed down 2.24% for the week.

A tough day for the Aussie market with broad-based selling knocking shares sharply low – the higher beta parts of the market felt the brunt of the risk-off attitude while the IT stocks were the only ones to finish up on the day - WiseTech (WT) +0.98% only knows one way!

A weaker session for the ASX, and with no lead from the US we were left to key off marginally softer European markets while Asian stocks also tracked lower during our time zone. Banks lost some of yesterday’s gains while property stocks also fell.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.