- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

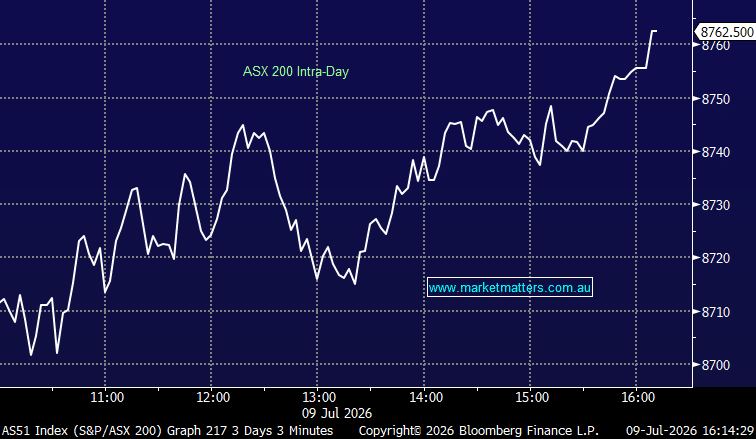

The ASX closed lower on Thursday as a fresh surge in oil prices reignited inflation fears, after Donald Trump said the Iran ceasefire was effectively “over” and the US struck Iran for a second consecutive day. The ASX 200 fell as much as ~50pts intraday before rallying through the afternoon to finish down just 22pts – another solid fight back.

Miners were the heaviest drag as gold extended its slide, while energy stocks led on the back of the Brent spike. Banks were mixed but pared earlier losses into the close. Overall, a pretty solid session given the negative news flow about.

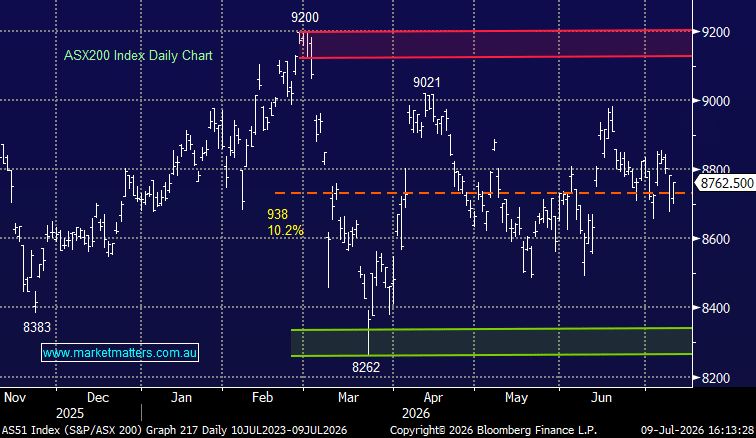

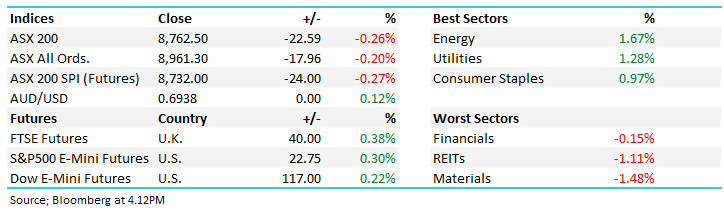

- ASX 200: -22.59 pts / -0.26% to 8,762.50

- AUD/USD: 0.6938, +0.12%

- Best sectors: Energy +1.67%, Utilities +1.28%, Consumer Staples +0.97%

- Worst sectors: Materials -1.48%, REITs -1.11%, Financials -0.15%

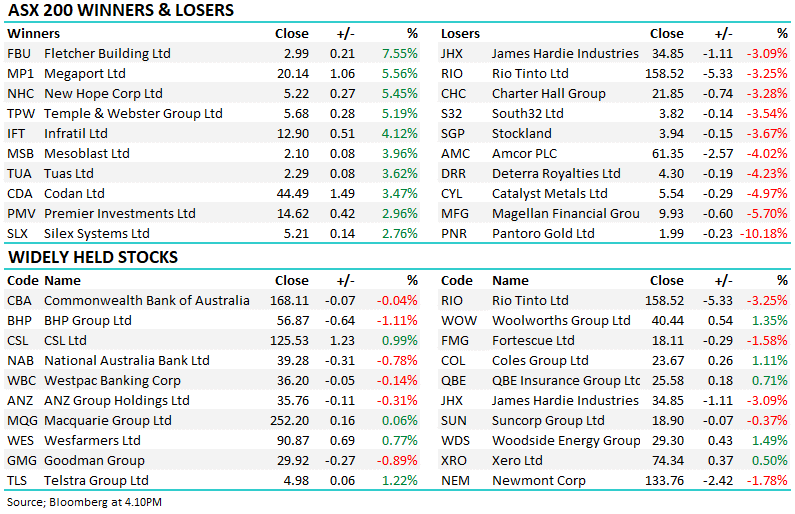

- FDC Consolidated (ASX: FDC) +12.33% to $3.37 — Rocketed as much as 17% above its $3 IPO price after raising $400m in the ASX’s largest float of 2026; the construction, fit-out and infrastructure group counts NextDC and Digital Realty data centre work in its pipeline.

- Fletcher Building (ASX: FBU) +7.55% to $2.99 — Upgraded FY26 EBIT guidance by ~6.4% to NZ$400m–$403m on stronger-than-expected property sales and improved manufacturing and distribution volumes.

- Pantoro Gold (ASX: PNR) -10.18% to $1.99 — whacked as much as 22% intraday after FY26 production of 77,408oz missed February’s 86,000–92,000oz guidance; blamed labour shortages and contractor underperformance. FY27 guidance of 90,000-105,000oz at AISC of $2,800-$3,400/oz. Ended the year debt-free with $223.4m cash and bullion.

- Rio Tinto (ASX: RIO) -3.25% to $158.52 — Cut to Underweight from Equal-weight by Morgan Stanley (PT $149.00 from $171.50) on weaker aluminium dynamics and renewed merger-speculation risk after August 5.

- BHP (ASX: BHP) -1.11% to $56.87 — Fell with the broader miner sell-off despite Morgan Stanley reiterating it as its preferred major, citing copper’s >50% earnings contribution and electrification/AI infrastructure demand (Overweight, PT $67.50). We agree with MS on this.

- Deterra Royalties (ASX: DRR) -4.23% to $4.30 — Cut to Underweight by Morgan Stanley alongside the broader miner reshuffle.

- Catalyst Metals (ASX: CYL) -4.97% to $5.54 — Secured gold price protection via forward contracts on 30,000oz at a fixed $6,075/oz to manage volatility while retaining upside exposure.

- Newmont (ASX: NEM) -1.78% to $133.76 — Tracked the broader gold/materials weakness as spot gold held near $US4,080/oz.

- Northern Star (ASX: NST) -0.89% to $20.13 appointed former Perseus Mining CEO Jeff Quartermaine as an independent non-executive director.

- Woodside Energy (ASX: WDS) +1.49% to $29.30 — Led the energy sector higher as Brent extended its rally on Strait of Hormuz supply risk.

- Santos (ASX: STO) +2.00% — Built on Wednesday’s rally (its best day since March 2) as oil prices continued to climb.

- Steadfast (ASX: SDF) +0.78% — Takeover talks continue with an Amwins Group/Dragoneer Investment-led consortium, which reaffirmed its $7.7bn proposal.

- WiseTech Global (ASX: WTC) -0.06% — Citi cut FY26–FY28 net profit forecasts by 2–17% and lowered FY27 CargoWise revenue growth to 12%, citing the DSV migration and delayed AI features; PT cut to $52.00 from $66.00 (Buy maintained).

- Commonwealth Bank (ASX: CBA) -0.04% to $168.11, National Australia Bank (ASX: NAB) -0.78% to $39.28, Westpac (ASX: WBC) -0.14% to $36.20, ANZ (ASX: ANZ) -0.31% to $35.76 — Banks broadly softer but recovered through the session alongside the wider index rebound.

- Oil: Brent rose 1% to $US78.83/bbl, adding to Wednesday’s 5%+ jump, after the US struck Iran for a second day and revoked Tehran’s global oil-sale waiver. Focus has shifted from inventories to shipping/insurance risk through the Strait of Hormuz.

- Gold: Spot little changed near $US4,080/oz after three straight days of declines; down more than a fifth since the Iran conflict began in late February.

- Global gold ETFs still recorded $US8bn of H1 inflows despite June outflows of $US8.9bn, led by Asian and European demand; North American funds saw their weakest H1 since 2013.

- Asian markets: China +1%, Hong Kong -0.8% and Japan +1.8%

- Global futures: FTSE +0.38%, S&P 500 E-mini +0.30%, Dow E-mini +0.22%.