- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

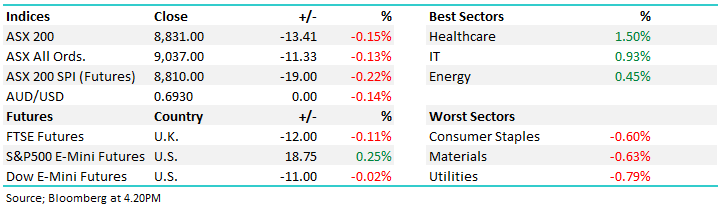

The ASX 200 eased today in what was a relatively subdued start to the week, with the market spending most of the session oscillating around the flatline before sellers gradually gained the upper hand into the afternoon. There was little in the way of macro catalysts, leaving investors to rotate away from the heavyweight Banks and Miners that drove Friday’s rally and back toward Healthcare, Technology and Energy.

Materials accounted for most of the index’s weakness despite a strong day for the gold miners as iron ore remained under pressure. Financials were also under pressure as investors reduced exposure to the major banks after a bounce over the past week. Energy also outperformed even as oil prices softened, while Technology found support as investors rotated back into quality growth names.

- ASX 200: -13.41 pts / -0.15% / 8,831.00

- AUD/USD: US$0.6930 / -0.14%

- Best sectors: Healthcare +1.50%, IT +0.93%, Energy +0.45%

- Worst sectors: Utilities -0.79%, Materials -0.63%, Consumer Staples -0.60%

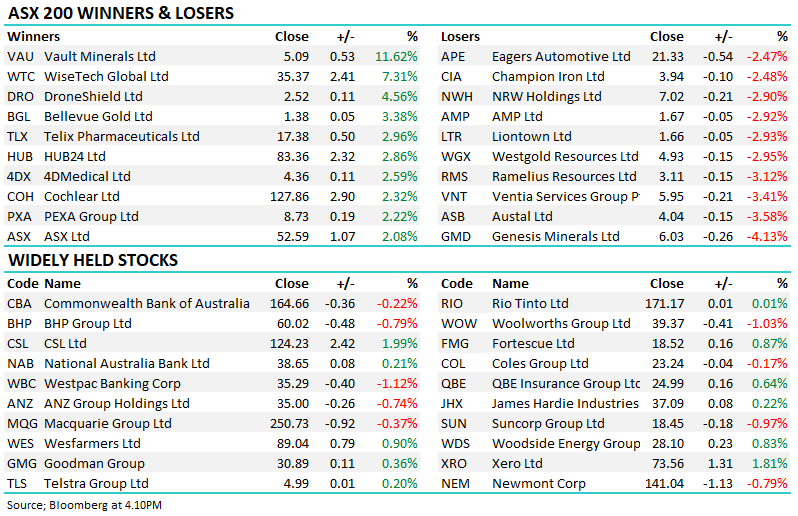

- Genesis Minerals (ASX: GMD) -4.13% to $6.03 slipped after launching a $5.6bn scrip-and-cash bid for Vault Minerals (ASX: VAU) +11.62% to $5.09, trumping Regis Resources’ existing proposal. The market questioned the valuation paid by Genesis, while Vault shareholders welcomed the improved offer.

- Santos (ASX: STO) +1.41% to $7.20 enjoyed its strongest session in two months after Morgan Stanley upgraded the stock to Overweight, citing an improving risk/reward profile despite softer oil prices. Woodside (ASX: WDS) +0.83% to $28.10 also firmed alongside the broader Energy sector.

- Healthcare was the standout sector, led by CSL (ASX: CSL) +1.99% to $124.23, which notched its best close since late April. The stock has now rallied more than 30% from its June lows despite no fresh company-specific news.

- Boss Energy (ASX: BOE) +6.27% to $1.35 rallied after Macquarie upgraded the uranium producer to Outperform and lifted its price target by 35%. The broker pointed to improving confidence around Honeymoon’s wellfield design, a stronger resource outlook and an accelerated feasibility study due in late August.

- Commonwealth Bank (ASX: CBA) -0.22% to $164.66 eased after updating its economic forecasts, warning the housing downturn rather than the Middle East conflict is now expected to be the primary drag on Australian growth into year-end. The bank continues to expect the RBA to remain on hold through 2026 before beginning to cut rates in 2027.

- Fortescue (ASX: FMG) +0.87% to $18.52 finished higher despite confirming it had been served with a Federal Court class action relating to historical allegations of sexual harassment and discrimination at its Australian operations. The company said the proceedings remain at an early stage and damages are yet to be specified.

- Dexus (ASX: DXS) +0.55% to $5.49 edged higher after reporting draft property valuations showed its portfolio declined just 0.2% over the June half, with industrial asset strength largely offsetting continued weakness across office property.

- Helia (ASX: HLI) -2.11% to $5.58 finished weaker despite securing a new four-year exclusive lenders mortgage insurance agreement with ING Australia, extending a relationship that accounted for around 20% of FY26 gross written premium.

- Worley (ASX: WOR) +0.19% to $10.80 gained after being selected as one of 11 contractors on a five-year project management consultancy agreement with Saudi Aramco.

- Greatland Resources (ASX: GGP) +0.17% to $11.79 was little changed after reporting FY26 gold production of 328,986oz and copper output of 14,594t, with gold production finishing around 6% above guidance.

- Oil (WTI): ~US$69.20/bbl / +0.7%

- Gold: ~US$4,150/oz / -0.5%

- Iron Ore: ~US$97.90/mt / +0.2%

- Asian Markets: China flat, Hong Kong +0.9%, Nikkei −0.5%

- Global Futures: FTSE −0.18%, S&P 500 E-Mini +0.25%, Dow E-Mini +0.07%