- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

The ASX recovered some of last week’s weakness to finish higher, as investors looked through ongoing geopolitical uncertainty and rotated back into beaten-down growth names.

While the ceasefire between the US and Iran looked shaky over the weekend, the belief that progress is being made continues to underpin broader positive sentiment. Investors remain cautious around commodity markets, particularly base metals, while Brent crude held around pre-conflict levels.

Today’s leadership was notable, with Technology the best-performing sector, while Healthcare continued its sharp rebound from early June lows. In contrast, Utilities and Real Estate lagged, though the majority of stocks within these sectors traded ex-dividend.

- ASX 200: +59.22 pts / +0.68% / 8,823.40

- AUD/USD: US$0.6896 / flat

- Best sectors: Information Technology +4.04%, Healthcare +2.12%, Communications +1.11%

- Worst sectors: Utilities -2.58%, REITs -0.89%, Industrials -0.80%

- Lithium stocks remained under pressure despite UBS reiterating a constructive long-term view on the sector. The broker reduced price targets across PLS Group (ASX: PLS) +0.79% to $5.08, Liontown Resources (ASX: LTR) flat at $1.66 and IGO (ASX: IGO) +0.14% to $7.32 following weaker spodumene price assumptions, although it continues to forecast robust demand growth through 2026 and beyond.

- Neuren Pharmaceuticals (ASX: NEU) +36.2% to $16.60 surged after partner Acadia received a positive opinion from the European Medicines Agency’s CHMP supporting approval of its DAYBUE product for Rett syndrome. If approved, it would become the first treatment for the condition in Europe, triggering a US$35m milestone payment to Neuren plus future royalties and sales milestones.

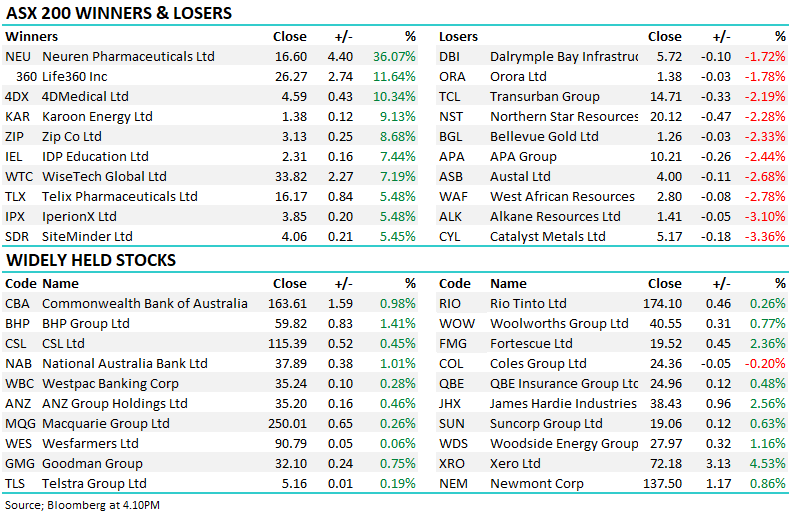

- Life360 (ASX: 360) +11.4% to $26.27, Xero (ASX: XRO) +5.2% to $72.18 and WiseTech Global (ASX: WTC) +5.1% to $33.82 spearheaded a strong rebound across the technology sector following a sharp recovery in US software stocks on Friday night.

- Healthcare continued recent outperformance, with Telix Pharmaceuticals (ASX: TLX) +6.2% to $16.17, Pro Medicus (ASX: PME) +3.4% to $197.45, Ramsay Health Care (ASX: RHC) +2.37% to $44.12 and ResMed (ASX: RMD) +2.00% to $29.52 extending the sector’s recovery — the cohort is now up more than 16% since early June.

- Karoon Energy (ASX: KAR) +8.3% to $1.38 rallied after restarting production at its SPS-92 well, lifting FY26 capex guidance and flagging another on-market share buyback.

- Ramelius Resources (ASX: RMS) +2.3% to $3.07 gained after confirming the $300m sale of its Edna May gold operation to Forrestania Resources. The transaction allows Ramelius to focus on its core growth assets while retaining upside through a $100m equity stake in Forrestania.

- HMC Capital (ASX: HMC) +1.7% rose after securing new institutional private credit mandates with funding capacity of up to $1.35bn, highlighting continued demand for Australian commercial real estate debt.

- CSL (ASX: CSL) +1.2% to $115.39 recovered despite warning it expects to halt new EU patient starts for Tavneos following a recommendation from European regulators to revoke the therapy’s marketing authorisation.

- APA Group (ASX: APA) -2.44% to $10.21 softened after trading without its 30c final dividend – Utilities lagged the broader market as several stocks traded ex-dividend.

- Morgan Stanley maintained a defensive stance on Australian equities, highlighting persistent underweights in the major banks while favouring Macquarie, insurers and selective Energy exposure. The broker also warned changes to property tax concessions could slow Australia’s housing cycle and weigh on bank earnings into FY27.

- Oil (WTI): ~US$69.70/bbl / +0.7%

- Gold: ~US$4,061/oz / -0.6%

- Iron Ore: ~US$98.20/mt / −0.50%

- Asian Markets: China +0.6%, Hong Kong +1.6%, Nikkei −0.2%

- Global Futures: FTSE −0.18%, S&P 500 E-Mini +0.25%, Dow E-Mini +0.07%