- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

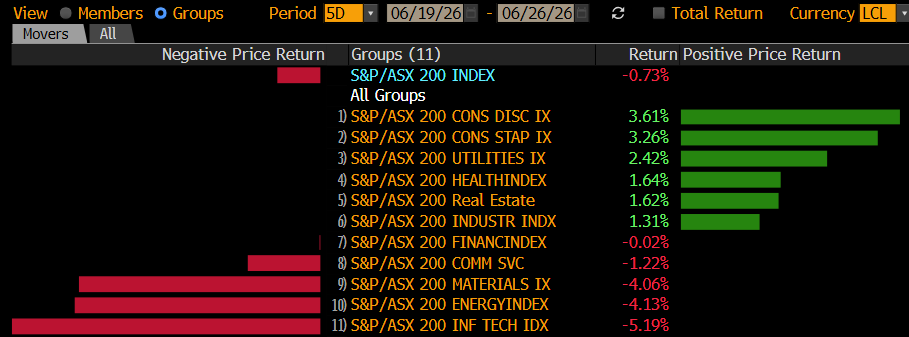

A flat finish capped off a soft week for equities, with the ASX 200 down 0.8% and just two trading sessions remaining before EOFY. Technology (-5%), Materials (-4%) and Energy (-4%) were the week’s biggest drags, while investors rotated into more defensive areas such as Consumer Staples (+3%) and Utilities (+2%). The standout, however, was the beaten-down retail sector, which rallied more than 3.5% for the week. We continue to see further upside here as the market increasingly prices out the prospect of additional interest rate hikes by the RBA.

Today’s trade was choppy, weighed down by weakness across Asian technology stocks. South Korea’s Kospi fell as much as 6.5%, with Samsung and SK Hynix both dropping more than 7% on renewed concerns about memory chip demand. Reports that OpenAI may delay its IPO also hit sentiment, sending SoftBank shares down as much as 13% in Tokyo.

- ASX 200: +15.55 points (+0.18%) to 8,764.20

- AUD/USD: 0.6890 (-0.29%)

- Best sectors: Utilities (+1.01%), Consumer Staples (+0.81%), Materials (+0.81%)

- Worst sectors: Healthcare (-1.30%), IT (-1.17%), Communications (-0.50%)

- Gold miners dominated the winners’ board: Ramelius Resources (ASX: RMS) +3.81% to $3.00, Perseus Mining (ASX: PRU) +3.62% to $5.15, Resolute Mining (ASX: RSG) +3.59% to $1.01, Regis Resources (ASX: RRL) +3.45% to $6.59, Westgold Resources (ASX: WGX) +3.43% to $4.83, Northern Star Resources (ASX: NST) +3.36% to $20.59, Evolution Mining (ASX: EVN) +2.95% to $12.23, Catalyst Metals (ASX: CYL) +2.88% to $5.35 and Vault Minerals (ASX: VAU) +2.71% to $4.55 all firmer, as the sector caught a broad bid; Evolution Mining held in the Active Growth Portfolio.

- Car Group (ASX: CAR) -5.22% to $24.50 — fell sharply, with the online classifieds group caught up in the broader Asian-led tech selloff weighing on the sector.

- NextDC (ASX: NXT) -4.48% to $14.06 — among the session’s biggest laggards as data-centre names came under pressure alongside the broader AI-sentiment unwind.

- HUB24 (ASX: HUB) -4.76% to $69.89 — also among the day’s heaviest fallers.

- Coles Group (ASX: COL) +1.45% to $24.41 — extended its monthly gain as investors rotated into defensives.

- Woolworths Group (ASX: WOW) +0.75% to $40.24 — also higher as consumer staples outperformed.

- CSL (ASX: CSL) -2.36% to $114.87 — a key drag on the Healthcare sector, which was the day’s worst performer.

- BHP Group (ASX: BHP) +0.80% to $58.99 — reshaped its leadership structure ahead of Brandon Craig taking over as CEO, splitting the president Americas role into separate North America and South America positions; held in the Active Growth and Income Portfolios.

- Rio Tinto (ASX: RIO) +2.15% to $173.64 — rose after Bloomberg reported it is in talks with Vitol to set up a freight joint venture.

- HMC Capital (ASX: HMC) +0.7% to $2.94 — received ACCC and FIRB approval for its strategic energy partnership with KKR, clearing the final regulatory hurdle for a deal expected to close shortly; held in the Emerging Companies Portfolio

- ANZ Group (ASX: ANZ) +0.52% to $35.04 and Westpac (ASX: WBC) +0.23% to $35.14 — firmer; held across the Active Growth and Income Portfolios.

- Judo Capital (ASX: JDO) -3.83% to 0.88c— extended this week’s heavy losses (down ~41% over five days) following Thursday’s profit-warning-driven plunge and a wave of broker downgrades (see Broker Moves)

- DigiCo Infrastructure REIT (ASX: DGT) +5.7% to $2.57 — rose after CEO Michael Juniper stepped down effective immediately, having not returned from personal leave;

- 4DMedical (ASX: 4DX) -8.97% to $4.16 — fell sharply despite receiving TGA approval for its CT:VQ lung imaging software, after rocketing ~1700% over the past year.

- Transurban (ASX: TCL) +1.45% to $15.39 — advanced after its 95 Express Lanes JV signed an agreement with Virginia’s DOT on the I-95 Express Lanes upgrade.

- NRW Holdings (ASX: NWH) flat at $7.25 — ended unchanged on the day despite news that subsidiary Golding Contractors secured two new contracts worth a combined $190 million

- Gold flat at $US4022/oz

- US Futures were weaker – Nasdaq Futures -1.2%, Emini’s (S&P) -0.6% and Dow Futures -0.13%