- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

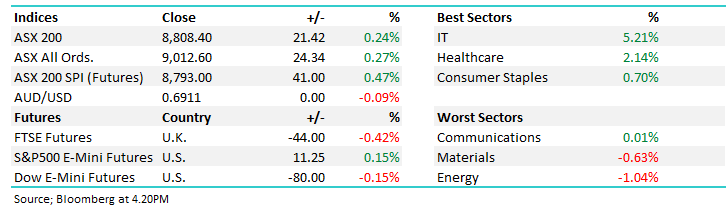

The local market broke a four-day losing streak today, with the ASX 200 grinding higher as investors weighed a mixed May inflation print. Headline CPI cooled to 4% — softer than the 4.3% expected, largely on falling fuel prices — but the RBA’s preferred trimmed mean measure accelerated to 3.6%, above forecasts, keeping underlying inflation pressures alive. The Aussie dollar slumped to an 11-week low before paring losses, as markets turn to Thursday’s jobs report and an evening speech from RBA deputy governor Andrew Hauser for the next steer on policy.

- ASX 200: 8,808.40 / +21.42pts / +0.24%

- AUD/USD: 0.6911 / −0.09%

- Best sectors: IT +5.21%, Healthcare +2.14%, Consumer Staples +0.70%

- Worst sectors: Communications +0.01%, Materials −0.63%, Energy −1.04%

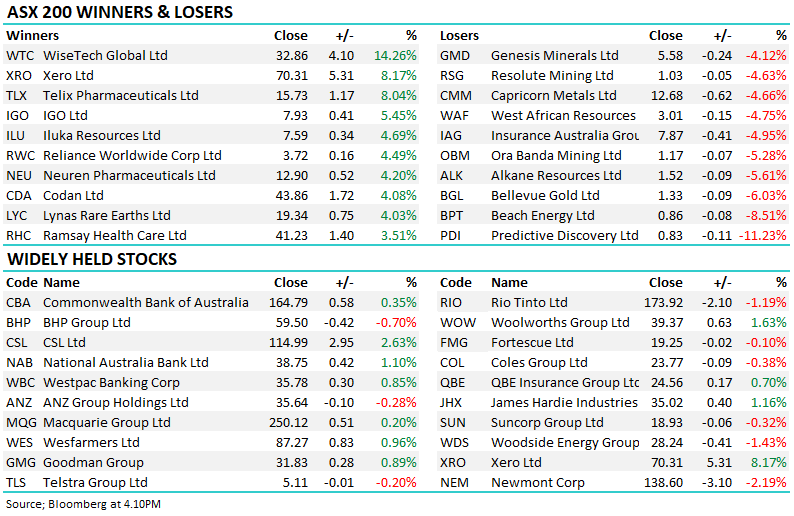

- Xero (ASX: XRO) +8.17% to $70.31 rose as Citi said the company’s UK price increases signal confidence in its market position, while UBS flagged strong app download data as a positive signal.

- WiseTech Global (ASX: WTC) +14.26% to $32.86 bounced as dip-buyers stepped in after a two-session slide of more than 20% tied to reports about founder Richard White.

- Healthcare was solid today, with CSL (ASX: CSL) +2.63% to $114.99 extending its one-month gain to almost 20%, while Pro Medicus (ASX: PME), ResMed (ASX: RMD) and Ramsay Health Care (ASX: RHC) each rose around 3.5%.

- A mixed bag around Energy & Resources – Woodside Energy (ASX: WDS) −1.43% to $28.24, Beach Energy (ASX: BPT) −8.51% to $0.86 and BHP (ASX: BHP) −0.70% to $59.50 all fell as copper held a loss, while Ora Banda Mining (ASX: OBM) −5.28% to $1.16 and Newmont (ASX: NEM) −2.19% to $138.60 also declined.

- Baby Bunting (ASX: BBN) −10.6% to $1.47 downgraded its 2H profit forecast to $11m–$12m, ~12% below consensus at the midpoint.

- KMD Brands (ASX: KMD) −4.6% to $0.062 flagged a 1-for-25 share consolidation, cutting shares on issue from ~1.8bn to ~72m.

- Tasmea (ASX: TEA) +6.9% to $9.65 acquired energy services provider JPS Group for up to $75m and reaffirmed FY26 earnings guidance.

- Atlas Arteria (ASX: ALX) −0.10% to $5.10 traded flat as IFM Investors extended its hostile takeover offer by 14 days after lifting its stake above 50%; an independent expert said the $5.10/share offer undervalues the toll-road operator.

- Iluka Resources (ASX: ILU) +4.69% to $7.59 rebounded from yesterday’s announcement that it had secured its first binding rare earths offtake agreement.

- Collins Foods (ASX: CKF) +1.8% to $8.35 rose despite Citi trimming FY27 EPS forecasts by 8% on cost pressures but kept the stock at Buy, cutting its price target to $10.30 (closing price not available).

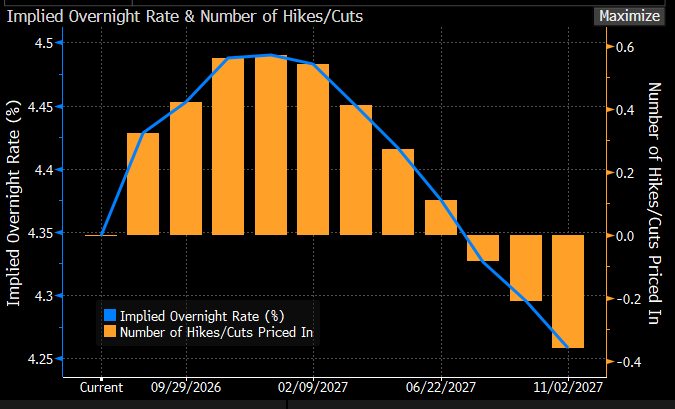

- UBS held its call for a 25bp August RBA hike to 4.60%, calling the case “a closer call” but citing sticky trimmed mean inflation; Betashares’ David Bassanese took the opposite view, arguing the RBA is likely done hiking this year — a view shared by ANZ and NAB.

- Oil (WTI): ~US$72.50/bbl / -0.9%

- Gold: ~US$4,087/oz / -0.6%

- Iron Ore: ~US$98.80/mt / +0.8%

- Asian Markets: China +0.2%, Hong Kong +0.5%, Nikkei -0.5%

- Global Futures: FTSE −0.42%, S&P 500 E-Mini +0.15%, Dow E-Mini −0.15%