- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

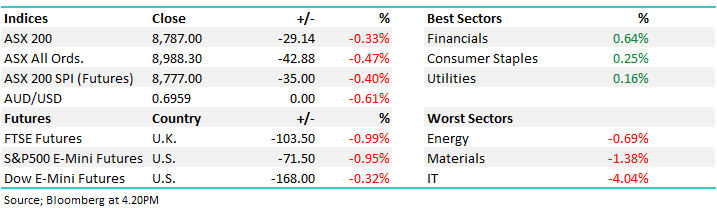

The ASX 200 finished lower today, with choppy trade through, in positive territory briefly before selling in technology, resources and small caps outweighed strength in the major banks and defensive sectors. Resilience in the Big Four provided some cushion, but market breadth was notably weak with around two-thirds of stocks finishing in the red. Investors continued to digest developments around US-Iran peace negotiations, while positioning ahead of tomorrow’s Australian inflation data and ongoing scrutiny of the AI trade.

- ASX 200: 8,787.00 / -29.14pts / -0.33%

- AUD/USD: 0.6959 / -0.61%

- Best sectors: Financials +0.64%, Consumer Staples +0.25%, Utilities +0.16%

- Worst sectors: Energy -0.69%, Materials -1.38%, IT -4.04%

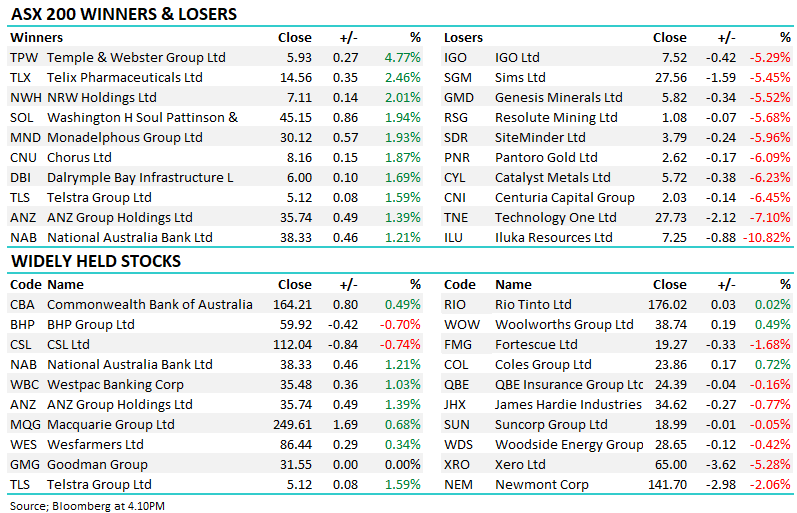

- WiseTech Global (ASX: WTC) -4.39% to $28.76 slid again after confirming Executive Chairman Richard White was “not aware” of any AFP investigation being reported in the media.

- Iluka Resources (ASX: ILU) -10.82% to $7.25 tumbled after announcing its first binding rare earths offtake agreement and securing access to the final tranche of the Federal Government’s $1.65 billion non-recourse loan for the Eneabba refinery, with the market more focused on project execution risk and the path to production.

- Centuria Capital Group (ASX: CNI) -6.57% to $2.03 traded lower as investors digested a ~$300 million capital raising, with concerns around earnings per share dilution outweighing the ambitious AI infrastructure growth strategy.

- Reliance Worldwide (ASX: RWC) -3.00% to $3.56 declined after announcing plans to close its brass casting, forging and machining operations in Melbourne as part of a broader manufacturing rationalisation program, with approximately 85 jobs expected to be impacted.

- ANZ Group Holdings (ASX: ANZ) +1.39% to $35.74, National Australia Bank (ASX: NAB) +1.21% to $38.33, Commonwealth Bank of Australia (ASX: CBA) +0.49% to $164.21 and Westpac Banking Corp (ASX: WBC) +1.03% to $35.48 helped support the broader market, with Financials comfortably the strongest major sector through the session.

- SGH Ltd (ASX: SGH) -1.03% to $44.11 traded lower even as Macquarie reiterated its Outperform recommendation and lifted its target price following the company’s proposed $500 million share buyback.

- Metcash (ASX: MTS) -2.88% to $3.03 extended recent weakness despite delivering a result largely in line with expectations, with investors focused on FY27 earnings headwinds including higher depreciation, interest costs and ongoing tobacco excise pressures.

- Viva Energy (ASX: VEA) -2.35% to $2.08 fell on broader Energy sector weakness, though the group restarted its residual catalytic cracking unit at its Geelong refinery; production has returned to more than 90 per cent of normal capacity, though the alkylation unit is expected to remain offline through 2027.

- TechnologyOne (ASX: TNE) -7.10% to $27.73 and Xero (ASX: XRO) -5.28% to $65.00 led losses in the technology sector as investors rotated away from growth and AI-linked exposures following weakness in US peers.

- Uranium stocks remained under pressure, with Paladin Energy (ASX: PDN) -4.48% to $9.39 and Deep Yellow (ASX: DYL) -4.78% to $1.50 weaker as risk appetite deteriorated across the broader resources sector.

- Oil (WTI): ~US$72.90/bbl / -1.2%

- Gold: ~US$4,115/oz / -1.8%

- Iron Ore: ~US$98.00/mt / -0.2%

- Asian Markets: China -1.4%, Hong Kong -1.9%, Nikkei -3.5%

- Global Futures: FTSE -0.99%, S&P 500 E-Mini -0.95%, Dow E-Mini -0.32%, Nasdaq -2%