- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

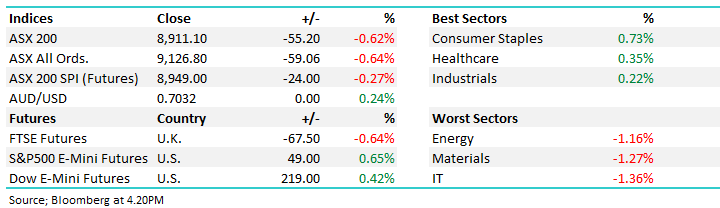

The ASX 200 fell away throughout the session as Federal Reserve policymakers under new chair Kevin Warsh signalled the chance of a rate hike later this year, hitting tech, financials and rate-sensitive growth names. Defensives held up best, with Consumer Staples and Healthcare the only sectors to post a meaningful gain, while Energy, Materials and IT led the market lower. Oil extended its slide as the US-Iran deal on reopening the Strait of Hormuz raised hopes for a quick return of Gulf supply, while gold and iron ore stayed under pressure from firmer US rate expectations underpinning a rise in the $US.

- ASX 200: 8,911.10 / -55.20pts / -0.62%

- AUD/USD: 0.7032 / +0.24%

- Best sectors: Consumer Staples +0.73%, Healthcare +0.35%, Industrials +0.22%

- Worst sectors: Energy -1.16%, Materials -1.27%, IT -1.36%

- Markets reacted to the Fed leaving rates unchanged but flagging higher borrowing costs later in 2026, with money markets now fully pricing a rate rise by October and two hikes broadly priced by March 2027.

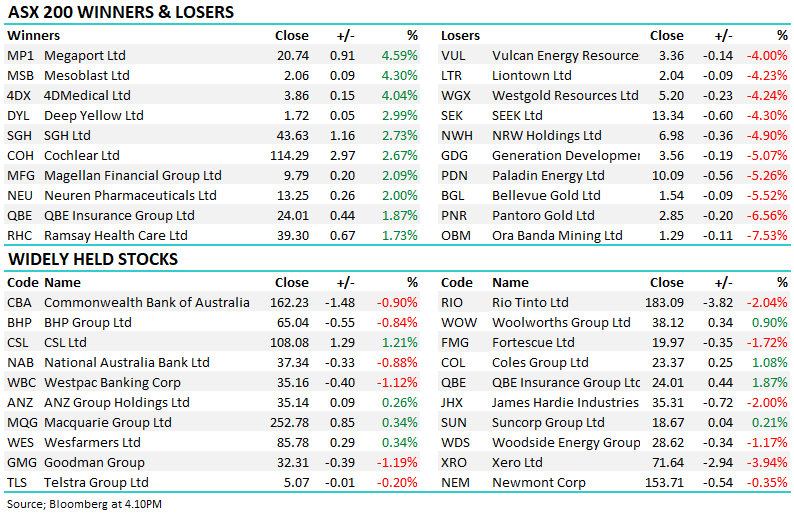

- Rate-sensitive tech names were sold off, with Xero (ASX: XRO) -3.94% to $71.64 and WiseTech Global (ASX: WTC) -3.39% among the session’s heaviest large-cap losers.

- The major banks were mixed: National Australia Bank (ASX: NAB) -0.88% to $37.34 and Westpac Banking Corp (ASX: WBC) -1.12% to $35.16 fell, Commonwealth Bank of Australia (ASX: CBA) -0.90% to $162.23 slipped, while ANZ Group Holdings (ASX: ANZ) +0.26% to $35.14 bucked the trend.

- Miners were broadly weaker as iron ore extended below $US100/t: Rio Tinto (ASX: RIO) -2.04% to $183.09 and Fortescue (ASX: FMG) -1.72% to $19.97 fell, while BHP (ASX: BHP) -0.84% to $65.04 eased back from its record high.

- Gold miners gave back some recent gains as bullion came under pressure from rising rate expectations: Ora Banda Mining (ASX: OBM) -7.53% to $1.29, Pantoro Gold (ASX: PNR) -6.56% to $2.85, Bellevue Gold (ASX: BGL) -5.52% to $1.54 and Westgold Resources (ASX: WGX) -4.24% to $5.20 all fell heavily, with Ramelius Resources (ASX: RMS) -3.01% and Newmont (ASX: NEM) -0.35% to $153.71 also weaker.

- Battery metals and uranium names were mixed: Liontown Resources (ASX: LTR) -4.23% to $2.04 and Vulcan Energy Resources (ASX: VUL) -4.00% to $3.36 fell, while Paladin Energy (ASX: PDN) -5.26% to $10.09 dropped even as fellow uranium play Deep Yellow (ASX: DYL) +2.99% to $1.72 rose.

- SEEK (ASX: SEK) -4.30% to $13.34 was among the session’s worst performers after Citi flagged downside risk to job ad volumes, estimating ANZ listings fell 2.9 per cent year-on-year in May as automation-exposed roles such as call centre and advertising jobs dragged on demand.

- On the upside, Megaport (ASX: MP1) +4.59% to $20.74, Mesoblast (ASX: MSB) +4.30% to $2.06 and 4DMedical (ASX: 4DX) +4.04% to $3.86 led the gainers, with SGH Ltd (ASX: SGH) +2.73% to $43.63 and Magellan Financial Group (ASX: MFG) +2.09% to $9.79 also firmer.

- Healthcare was a bright spot: Cochlear (ASX: COH) +2.67% to $114.29, Neuren Pharmaceuticals (ASX: NEU) +2.00% to $13.25, Ramsay Health Care (ASX: RHC) +1.73% to $39.30 and CSL (ASX: CSL) +1.21% to $108.08 all rose, while QBE Insurance Group (ASX: QBE) +1.87% to $24.01 also added to gains.

- Energy stocks were weaker as oil extended its slide: Woodside Energy Group (ASX: WDS) -1.17% to $28.62 fell and Santos (ASX: STO) -0.41% also eased.

- Washington H. Soul Pattinson (ASX: SOL) +0.77% rose after agreeing to sell its stake in Brickworks’ industrial joint venture property trusts to Goodman Group (ASX: GMG) -1.19% to $32.31 for $1.89 billion, a deal Morgans called primarily a liquidity and portfolio-positioning move rather than a valuation event, while Citi framed it as Goodman securing a premium, power-intensive logistics land bank.

- Challenger (ASX: CGF) +1.03% edged higher after its Fidante funds management unit agreed to merge with Channel Capital to form a combined group with $150 billion of assets under management.

- Transurban (ASX: TCL) +0.20% added an $825 million tranche to its syndicated bank debt facility, lifting total funding capacity to $3.475 billion.

- Lifestyle Communities (ASX:LIC) +9.76% to $5.51 flagged an acceleration in June-quarter sales, with new home sales up to 56 from 43 in the prior period and net debt down $182.8 million over the year, even as margins are expected to moderate to 8.5-9.5 per cent from 11 per cent.

- Electro Optic Systems (ASX:EOS) remained in a trading halt ahead of disclosure on a Remote Weapon Systems contract and a planned joint venture, both expected to be announced by 22 June.

- Oil: Brent ~US$78/bbl, WTI ~US$76/bbl, easing further as the interim US-Iran deal on reopening the Strait of Hormuz raised hopes for a quicker return of Gulf supply.

- Gold: ~US$4,298/oz, off earlier highs as traders priced in firmer US rate expectations.

- Iron Ore: ~US$99/t, pressured by weak Chinese steel demand and rising supply from Guinea’s Simandou project.

- The Bank of England’s rate decision is due this evening (AEST), with economists expecting a hold at 3.75 per cent as easing energy costs reduce the urgency for a hike.

- Global Futures: FTSE -0.64%, S&P 500 E-Mini +0.65%, Dow E-Mini +0.42%.