- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

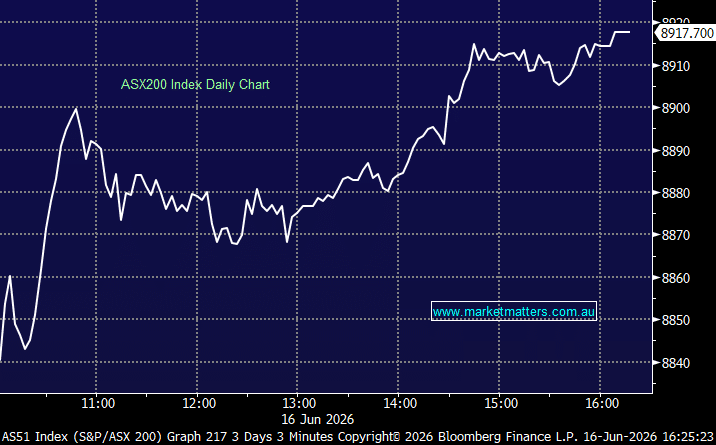

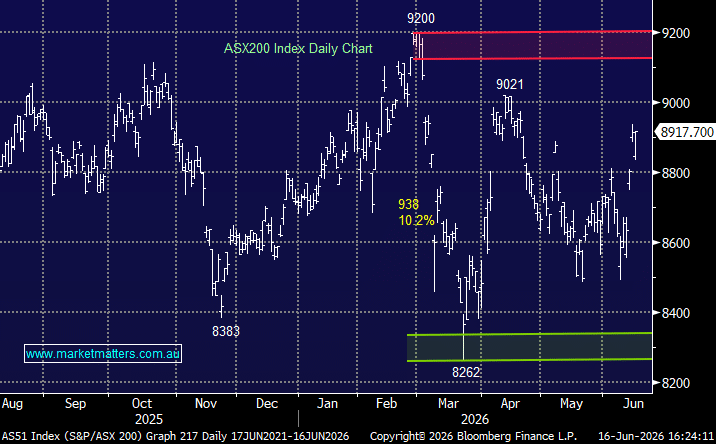

The ASX200 put on a fighting performance today, gapping down ~80pts on the open but recovering every last point of the deficit to finish mildly higher. The key news for the day was the Reserve Bank leaving the cash rate unchanged at 4.35%, pausing after three consecutive hikes this year.

Rate-sensitive sectors came under pressure early with Technology, Consumer Discretionary and Real Estate all taking a hit in the morning, though once the RBA delivered the widely expected hold, buyers gradually emerged. The Big Four banks provided most of the support and swung from negative to positive territory through the session helping to buoy the index. Resources also held up relatively well, helped by BHP trading at fresh record highs and continued momentum in the bounce in Gold stocks we’ve seen over the past few sessions.

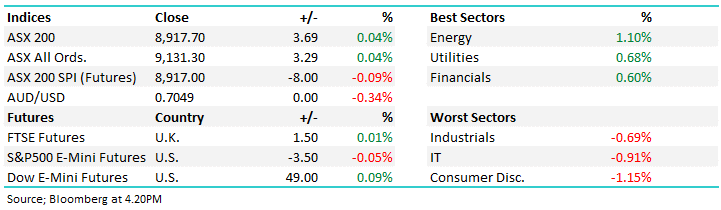

- ASX 200: 8,917.70 / +3.69pts / +0.04%

- AUD/USD: 0.7049 / −0.34%

- Best sectors: Energy +1.10%, Utilities +0.68%, Financials +0.60%

- Worst sectors: Industrials −0.69%, IT −0.91%, Consumer Disc. −1.15%

- The RBA left rates unchanged at 4.35%, though Governor Michele Bullock made it clear the inflation fight isn’t over. While the Board didn’t consider a hike this month, she refused to rule out further tightening should inflation fail to moderate as expected.

- Bullock also pushed back on recession concerns, reiterating the Bank is aiming to slow demand, not contract the economy. The RBA continues to forecast softer growth rather than an outright downturn.

- Bond manager PIMCO said recent data suggests policy is now sufficiently restrictive to return inflation to the RBA’s 2-3% target band by 2027, although near-term inflation risks remain elevated.

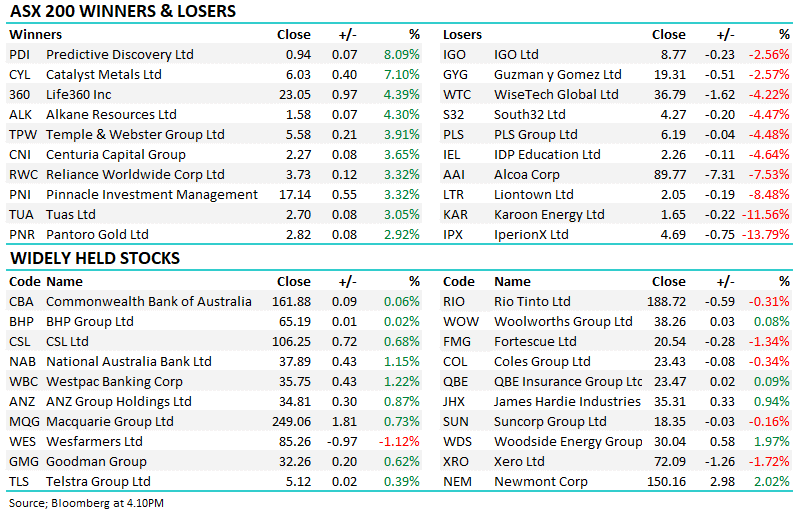

- Fresh from a $150m capital raising and out of a trading halt, Southern Cross Electrical Engineering (ASX: SXE) +19.9% to $4.82 surged after upgrading FY26 earnings guidance and unveiling maiden FY27 EBITDA guidance of at least $100m yesterday – the guidance underpinned by strong demand across data centres and infrastructure projects.

- Delays at the Who Dat E manifold weighed heavily on Karoon Energy (ASX: KAR) −11.56% to $1.65, with the key production restart now not expected until the second half of 2027, forcing a downgrade to medium-term production expectations.

- Shareholders overwhelmingly backed the $11.7bn takeover of Qube Holdings (ASX: QUB) +0.2% to $5.05 by a Macquarie-led consortium, clearing one of the final hurdles for the transaction.

- Atlas Arteria (ASX: ALX) ended flat after urging shareholders to reject a revised $5.10 per share offer, maintaining it materially undervalues the toll road operator as bidder IFM Investors lifted its stake to ~38%.

- HomeCo Daily Needs REIT (ASX: HDN) −1.15% to $1.29 slipped after reporting a $92m uplift in portfolio valuations during the half, taking total assets above $5.1bn.

- Transurban (ASX: TCL) −1.82% to $15.07 fell as analysts pointed to softer traffic growth, elevated valuation multiples and distribution yields that have fallen below long-term bond yields.

- A softer consumer backdrop saw UBS trim forecasts for Eagers Automotive (ASX: APE) −2.28% to $22.27, citing deteriorating conditions across its core dealership network.

- Alcoa (ASX: AAI) −7.53% to $89.77 was among the market’s weakest performers as aluminium stocks came under pressure following weaker commodity sentiment.

- Bucking broader weakness across parts of the technology sector, Life360 (ASX: 360) +4.39% to $23.05 continued its recent momentum, outperforming despite profit-taking elsewhere in growth names.

- Fresh record highs were again the story for BHP (ASX: BHP) +0.02% to $65.19, with the mining giant continuing to attract support despite softer Chinese economic data.

- The energy sector found some buyers, with Woodside Energy (ASX: WDS) +1.97% to $30.04 higher despite news the president of its Louisiana LNG project had departed after just over a year in the role.

- Oil (WTI): ~US$80.50/bbl / -0.2%

- Gold: ~US$4,320/oz / +0.1%

- Iron Ore: ~US$101.20/mt / −0.9%

- Asian Markets: China -0.1%, Hong Kong −1.7%, Nikkei +0.2%

- Global Futures: FTSE +0.01%, S&P 500 E-Mini −0.05%, Dow E-Mini +0.09%