- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

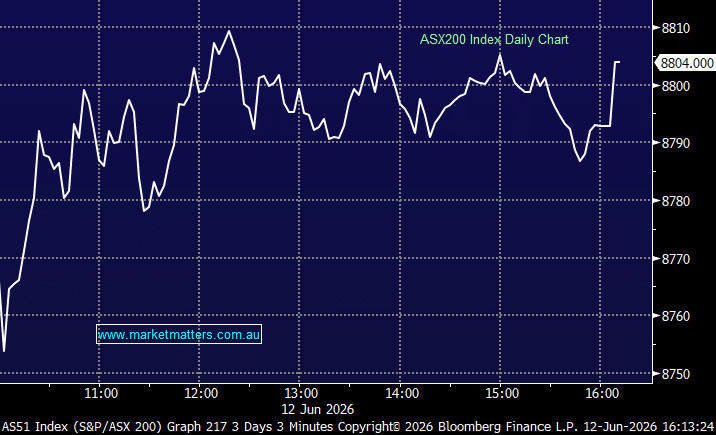

The ASX finished the week with its strongest session since April, surging almost 2% on the day after US President Donald Trump suggested a deal with Iran could be signed as soon as this weekend. The move wasn’t confined to a handful of stocks with around 85% of ASX 200 companies closing higher on the session. Materials led the charge after suffering heavily in recent weeks, banks bounced strongly following a difficult stretch, while consumer and rate-sensitive sectors continued an impressive recovery that has emerged as bond yields trend lower. The ASX 200 now sits at its highest level in around five weeks.

After spending much of the last few weeks worrying about what could go wrong, this week, and today’s session in particular was a reminder of how quickly markets can move when the news flow improves. This weekend has the potential to be more important than usual as markets watch for any concrete developments in US-Iran negotiations, not to mention tonight’s blockbuster SpaceX IPO as a major test of risk appetite.

- ASX 200: 8,804.00 / +170.75pts / +1.98%

- AUD/USD: 0.7038 / −0.17%

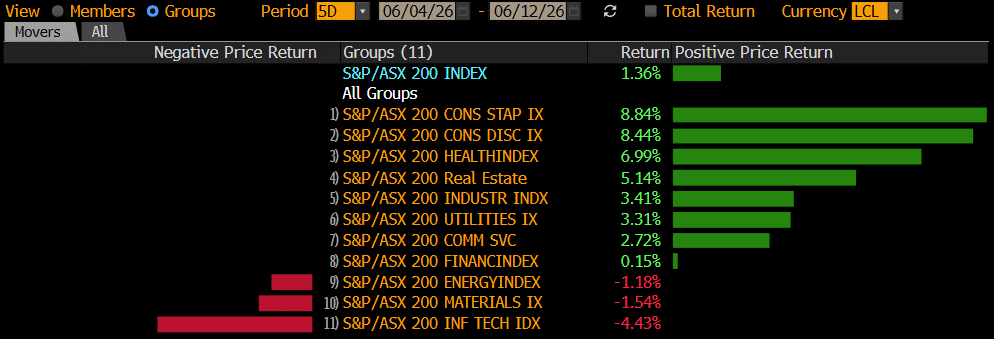

- Best sectors: Materials +4.06%, Consumer Disc. +2.05%, REITs +1.82%

- Worst sectors: Healthcare +0.08%, Communications −0.29%, Energy −0.46%

- Commonwealth Bank (ASX: CBA) +1.98% to $159.51, National Australia Bank (ASX: NAB) +2.30% to $36.50, Westpac (ASX: WBC) +1.45% to $35.00 and ANZ Group (ASX: ANZ) +1.01% to $34.17 all rebounded as investors rotated back into the banks after recent selling pressure.

- Notably this week, the Big Four have changed their tune around interest rate expectations — NAB has abandoned their call of a hike by the end of 2026, expecting a hold and rates to fall through 2027. ANZ and CBA also shifted from expectations of a hike to a hold through the end of the year.

- BHP (ASX: BHP) +3.50% to $62.93 rallied alongside the broader materials as copper prices stabilised, helping drive the index higher.

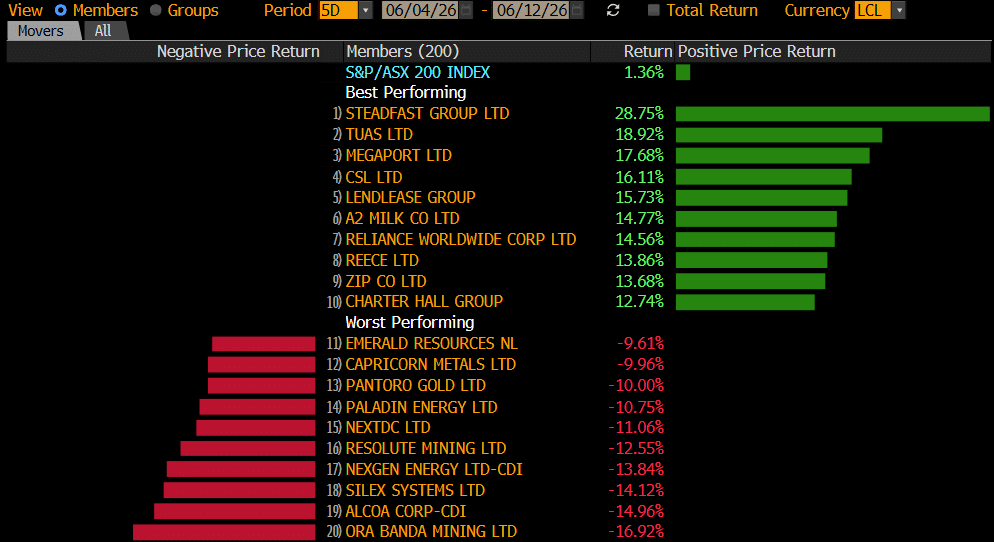

- Genesis Minerals (ASX: GMD) +10.83% to $5.32, Bellevue Gold (ASX: BGL) +9.35% to $1.35, Newmont (ASX: NEM) +3.95% to $137.79 and a host of gold names surged after bullion bounced 3.5% overnight following a brutal seven-session sell-off.

- Sandfire Resources (ASX: SFR) +8.07% to $19.83 and Develop Global (ASX: DVP) +8.9% were among the strongest performers as investors returned to copper exposure.

- Magellan Financial Group (ASX: MFG) +5.19% to $9.52 rallied after receiving ACCC clearance for its merger with Barrenjoey Capital Partners. The group intends to seek shareholder approval in October to rename the company Barrenjoey Group and adopt the ticker BJY.

- Monash IVF (ASX: MVF) +2.24% to 68.5c finished higher despite cutting FY26 profit guidance. Investors focused on the company’s improving market share and expectation that efficiency initiatives will contribute more meaningfully in FY27.

- REA Group (ASX: REA) −2.81% to $143.00 was one of the market’s notable laggards after Citi cut profit forecasts, citing risks from proposed changes to negative gearing and capital gains tax settings.

- The energy sector was the key laggard, with Woodside Energy (ASX: WDS) −0.92% to $31.23, Santos (ASX: STO) flat at $8.07 and Karoon Energy (ASX: KAR) −0.98% to $2.03 weaker as oil prices retreated sharply on hopes that disruptions to Middle Eastern supply routes may ease.

- Oil (WTI): ~US$86.10/bbl / -1.8%

- Gold: ~US$4,176/oz / -0.8%

- Iron Ore: ~US$101.40/mt / +0.2%

- Asian Markets: China +1.25%, Hong Kong +1.65%, Nikkei +2.67%

- Global Futures: FTSE +0.76%, S&P 500 E-Mini +0.06%, Dow E-Mini +0.11%