- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

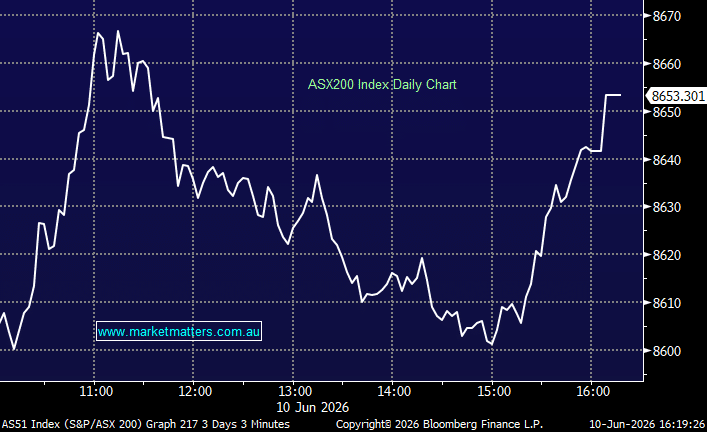

The ASX pushed higher today despite another round of US-Iran hostilities overnight, with investors continuing to look through the latest developments in the Middle East and instead focusing on the broader trajectory of negotiations. Oil prices initially jumped on the headlines though that had little bearing on the move for the local market, starting off strongly in a topsy turvy session – we saw a sharp +80pt rally in the morning before the index gave every single point of that back, before bouncing off the 8600 level and charging into the close to end the day firmly higher.

Consumer stocks were again the standout, extending a strong run over the past week while Gold miners remained under heavy pressure as bullion slid to its lowest level since November. The broader Materials space was weaker too, with the exception of the BHP which held firm, as copper prices stabilised.

- ASX 200: 8,653.30 / +49.13pts / +0.57%

- AUD/USD: 0.7021 / −0.13%

- Best sectors: Consumer Staples +3.87%, Consumer Disc. +3.58%, REITs +1.85%

- Worst sectors: Energy −0.87%, Materials −1.14%, IT −2.34%

- Reece (ASX: REH) +8.57% to $15.46 led the ASX 200 higher after Barrenjoey upgraded the plumbing supplier to Overweight and lifted its price target to $16.50, citing an improving earnings outlook.

- Consumer names continued their recent run, with Coles (ASX: COL) +4.95% to $23.73, Woolworths (ASX: WOW) +3.15% to $37.63 higher.

- Wesfarmers (ASX: WES) +4.25% to $83.39 hosted a strategy day outlining plans to drive growth through AI initiatives, data monetisation and an expanded addressable market at Bunnings.

- Steadfast Group (ASX: SDF) +36.20% to $5.38 surged after confirming a conditional $6.7bn takeover proposal from a consortium comprising Amwins and Dragoneer. The indicative $6.00 per share offer represents a +51% premium to last close.

- Sigma Healthcare (ASX: SIG) −5.48% to $2.76 slumped after confirming preliminary discussions regarding a potential acquisition of UK pharmacy giant Boots, a transaction reportedly valued at around $14bn. Investors appeared concerned about the scale and execution risk of the potential deal.

- Gold stocks remained under heavy pressure as bullion fell below US$4,200/oz, with Northern Star (ASX: NST) −3.54% to $18.54, Newmont (ASX: NEM) −3.09% to $137.30, Genesis Minerals (ASX: GMD) −6.33% to $4.88 and Ora Banda (ASX: OBM) −9.92% to $1.09 among the worst performers.

- IGO (ASX: IGO) −6.01% to $8.44 dropped after a fire at the Chemical Grade Plant 3 facility at Greenbushes. Fortunately, no injuries were reported, and the company maintained full-year guidance.

- Technology stocks lagged, with Xero (ASX: XRO) −2.04% to $76.82 and NextDC (ASX: NXT) −4.12% to $15.14 weaker.

- Defence name Boresight (ASX: BOS) rocketed on debut after listing following an $8m IPO, continuing the strong appetite for defence and security-related stocks.

- AGL Energy (ASX: AGL) +1.06% to $8.59 edged higher after breaking ground on a $490m gas-fired power station in Kwinana, Western Australia, aimed at strengthening grid reliability and supporting future energy demand.

- Helia Group (ASX: HLI) +1.83% to $5.00 gained after appointing Steadfast executive Mark Senkevics as chief executive, effective later this year.

- Oil (WTI): ~US$93.10/bbl / +0.06%

- Gold: ~US$4,207/oz / −1.2%

- Iron Ore: ~US$101.80/mt / +1%

- Asian Markets: China -0.53%, Hong Kong −0.84%, Nikkei −1.77%

- Global Futures: FTSE +0.13%, S&P 500 E-Mini −0.26%, Dow E-Mini −0.11%