- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

The ASX was on the back foot from the opening bell as investors digested overnight missile strikes between the US and Iran. Selling was significant but orderly, with the market moving gradually lower through the morning before popping and stabilising ~30pts above the lows for much of the afternoon. While geopolitical tensions dominated the headlines, weakness in iron ore provided an additional drag, with concerns around the rapid ramp-up of Guinea’s giant Simandou mine weighing on the local Miners.

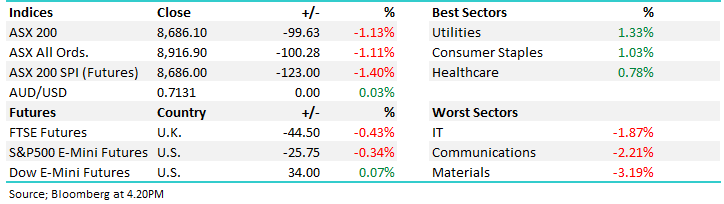

- ASX 200: 8,686.10 / −99.63pts / −1.13%

- ASX All Ords: 8,916.90 / −100.28pts / −1.11%

- AUD/USD: 0.7131 / +0.03%

- Best sectors: Utilities +1.33%, Consumer Staples +1.03%, Healthcare +0.78%

- Worst sectors: IT −1.87%, Communications −2.21%, Materials −3.19%

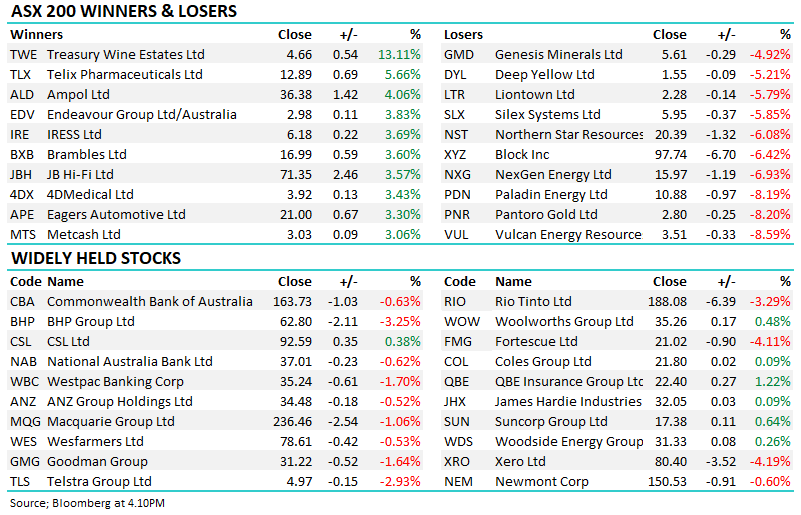

- BHP Group (ASX: BHP) −3.25% to $62.80, Rio Tinto (ASX: RIO) −3.29% to $188.08 and Fortescue (ASX: FMG) −4.11% to $21.02 led the market lower after Simandou exports accelerated and iron ore prices fell to their lowest level since April. Simandou shipments reached 2.2Mt in May compared to 1.1Mt in April, fuelling concerns around a supply glut and the potential displacement of Pilbara exports.

- The broader mining sector was also weak, with Lynas Rare Earths (ASX: LYC) −4.00% to $18.71, Iluka Resources (ASX: ILU) −2.23% to $7.90, Sandfire Resources (ASX: SFR) −3.75% to $19.51, South32 (ASX: S32) −3.26% to $4.75.

- Technology stocks gave back some of their recent gains after a softer result from Broadcom overnight, with weakness across Life360 (ASX: 360) −4.03% to $21.66, WiseTech Global (ASX: WTC) −2.93% to $40.14, Xero (ASX: XRO) −4.19% to $80.40.

- Treasury Wine Estates (ASX: TWE) +13.11% to $4.66 was the standout performer after delivering FY26 EBIT guidance ahead of consensus and outlining plans to simplify its brand portfolio and to accelerate the review of its struggling US operations.

- Endeavour Group (ASX: EDV) +3.83% to $2.98 rallied after Citi upgraded the stock to Buy, arguing the liquor retailer offers scope for market share gains despite near-term earnings uncertainty.

- Ampol (ASX: ALD) +4.06% to $36.38 extended recent gains after analysts responded positively to ACCC approval of the EG Group acquisition. Brokers viewed Ampol’s decision to cash-settle the scrip component as a sign of confidence in near-term earnings and refining margins.

- Megaport (ASX: MP1) remained in focus despite its trading halt, with Macquarie lifting its target price to $27.80 from $26.30. The broker described the company as a high-quality AI infrastructure play and highlighted upside from Contracted Compute.

- Pro Medicus (ASX: PME) −0.25% to $159.23 outperformed the broader tech sector after a five-year renewal with Ohio State University, with the total contract value ~80% higher than the existing arrangement demonstrating existing customers are expanding, rather than reducing contract commitments despite AI disruption concerns.

- ASX Ltd (ASX: ASX) +0.36% to $46.96 was resilient after UBS argued the recent selloff has left the exchange operator trading at its cheapest relative valuation in more than two decades.

- Oil (Brent): ~US$95.10/bbl / -0.9%

- Gold: ~US$4,467/oz / +0.8%

- Iron Ore: ~US$101.90/mt -1.6%

- Asian Markets: China –0.44%, Hong Kong –1.55%, Nikkei +1.7%

- Global Futures: FTSE Futures: −0.43% / S&P 500 E-Mini: −0.34% / Dow E-Mini: +0.07%